BOJ Monetary Policy Meeting: Bank adopts a more flexible approach to YCC, in effect altering the policy

The BOJ wrapped up its latest Monetary Policy Meeting (MPM) on 28 July.

The big news is that the Bank has decided to exercise more flexibility in conducting yield curve control (YCC). In practical terms, this represents a substantive adjustment to the YCC policy. However, it should be noted that the policy has been changed in one respect but left unchanged in another. On the one hand, the Bank intends to continue guiding the 10yr JGB yield so that it mainly stays within 0.5ppt to either side of 0%. On the other hand, it has significantly raised the hard limit at which fixed-rate purchase operations kick in to cap the 10yr yield, from 0.5% to 1.0%.

In describing its reasons for deciding to conduct YCC with more flexibility, the Bank argued first of all that it needs to “patiently continue with monetary easing”, stating that there is no clear path yet to sustainable and stable achievement of the 2% price stability target. It then added that in light of the considerable uncertainty surrounding economic activity and prices, its program of monetary easing can actually be made more sustainable through the exercise of greater flexibility in the conduct of YCC.

Expanding on this point about the elevated uncertainty surrounding economic activity and prices and the need for more flexibility in the management of YCC, the Bank’s argument is twofold: (1) in the event that upside risks to the economy and prices materialize, monetary policy can be kept accommodative through a decline in real interest rates and the mitigation of effects on the functioning of bond markets; (2) in the event that downside risks materialize, monetary policy can be kept accommodative in that long-term rates will have room in which to come down.

The decision on “conducting yield curve control (YCC) with greater flexibility” (in the BOJ’s own words) was made by an 8-1 majority vote. The sole dissenter was Toyoaki Nakamura, a former executive vice president at Hitachi, Ltd. While Mr Nakamura agreed in principle with the idea of allowing greater flexibility, he argued that it would be better to wait until it is clearer that companies have shored up their earning power. This in effect means that all nine members of the policy board approve of the idea of conducting the policy more flexibly.

Outlook report: Policy still accommodative, as the median view on inflation is largely unchanged, but the uncertainty around inflation prompted what is in effect an adjustment to the YCC policy

Following the MPM, the BOJ also released its latest Outlook for Economic Activity and Prices (Outlook Report). Normally, BOJ watchers look to this report for the policy board members’ median inflation forecasts. However, the decision to loosen up the YCC policy in a way that amounts to a change to the policy itself was made not because of the outlook for inflation as such, but because of the heightened uncertainty surrounding the inflation outlook.

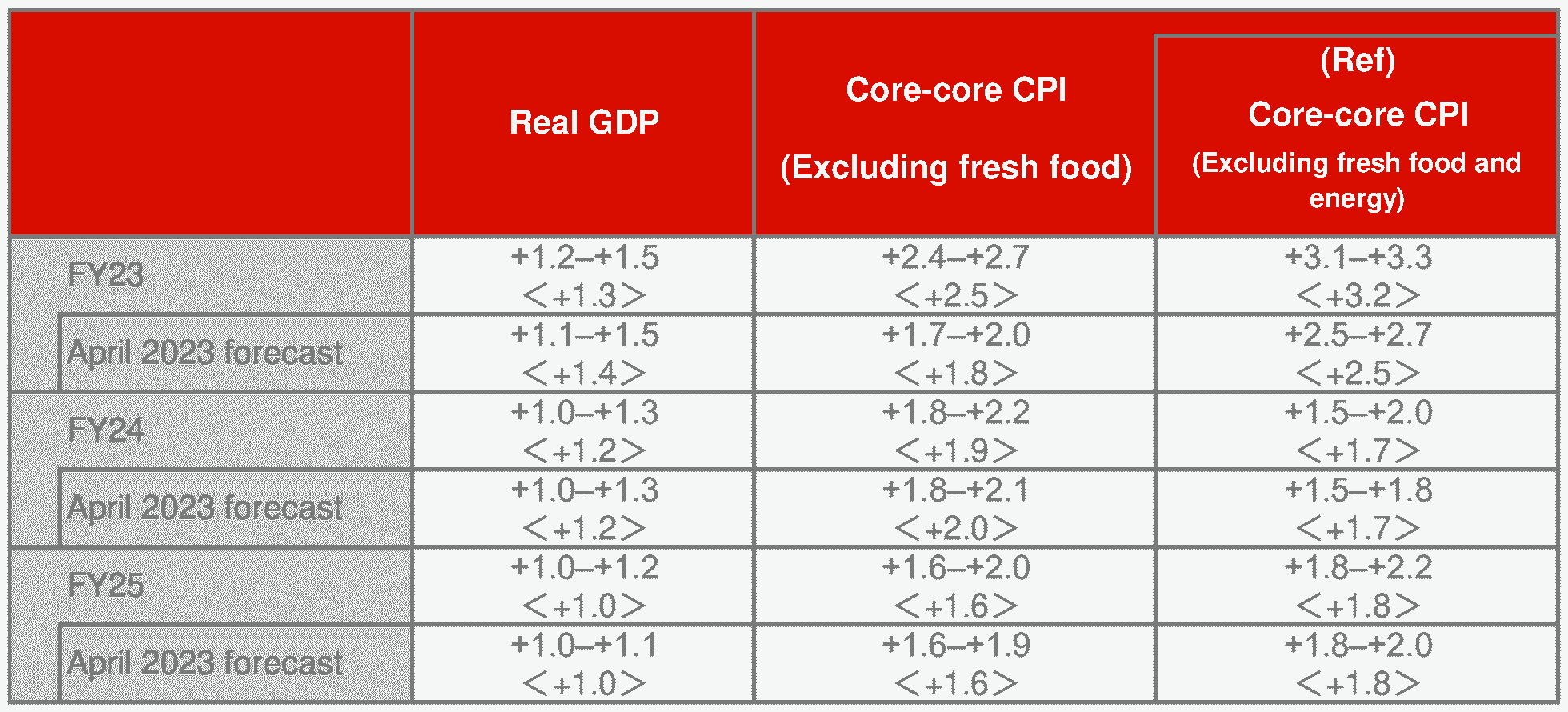

In the newly released Outlook Report, the board members’ median forecasts look for core CPI inflation (all items less fresh food) of +2.5% in FY23, +1.9% in FY24, and +1.6% in FY25 (Figure 1). In the previous report, issued in April, the numbers were +1.8%, +2.0%, and +1.6%. So while the median forecast for inflation in FY23 was revised up considerably, the outlook for FY24 and FY25 was not changed all that much. The BOJ does not think it has gotten closer to achieving its 2% inflation target in a sustainable and stable way, and its perception of the need to keep monetary policy accommodative is what led it to decide to handle its YCC policy more flexibly.

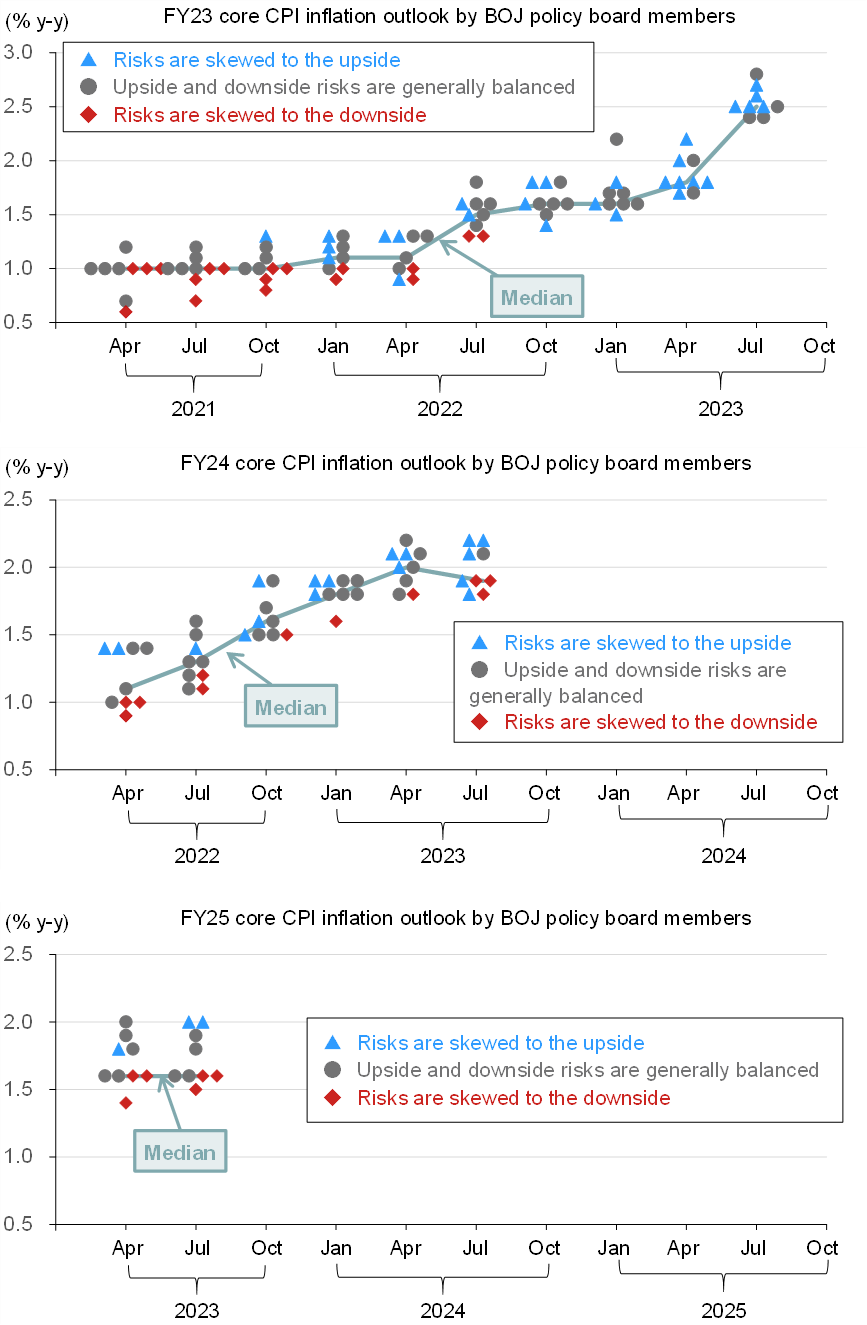

The Outlook Report also makes it clear that there is quite a bit of uncertainty surrounding even the policy board members’ median inflation forecasts. For example, while the board raised its median forecast for core CPI inflation in FY23 from +1.8% (in the April report) to +2.5% (in the July report), five of the policy board’s members (a majority) indicated that they think the risks are skewed to the upside (Figure 2, top).

In the forecasts for inflation in FY24, some members indicated that they think the risks are skewed to the downside. However, we have yet to see any indication that the members wary of the downside risks have actually lowered their inflation forecasts for FY24 (Figure 2, middle).

In the board’s inflation forecasts for FY25, members with higher inflation forecasts think the risks are skewed to the upside, while members with lower inflation forecasts think the risks are skewed to the downside (Figure 2, bottom).

This distribution of the perceived risks makes it plain that the BOJ sees a great deal of uncertainty in the outlook for prices. And as discussed above, it is this that prompted the decision to conduct YCC with greater flexibility.

We remove the prospect of a formal adjustment to YCC from our main scenario, and picture YCC and NIRP being dropped as early as 2024 H1 (probably in Apr–Jun); still see little likelihood of QT or positive interest rates at any time in 2024

In Figure 3 below, we lay out three scenarios for the forward conduct of the BOJ’s monetary policy, taking on board the content of today’s announcements.

In our main scenario (to which we assign a probability of 60%), we remove the expectation of a formal change to the YCC policy now that the BOJ has announced what amounts to a change in the policy. Building on our assumption that wage hikes in the spring of 2024 will be comparable to those worked out in 2023, we picture YCC and the negative interest rate policy (NIRP) being dropped completely as early as 2024 H1 (with Apr–Jun 2024 as the most likely timing). That said, we do not expect to see either quantitative tightening (QT) or a return to a positive interest rate policy at any time in 2024.

In risk scenario A (to which we assign a 30% probability), we picture the BOJ being quicker than we expect to make a judgment that the Japanese economy is on its way to sustainable and stable inflation of 2%. Should that happen, YCC could be abandoned at one of the MPMs between September and December 2023, before the results of the broad-perspective monetary policy review being conducted are even announced. Even in this scenario, we would expect the end of NIRP to come in 2024 H1 at the earliest (probably in Jan–Mar).

In risk scenario B (to which we assign a 10% probability), we picture the BOJ taking an increasingly cautious stance on the outlook for economic growth and inflation in the latter half of 2023 in response to economic deterioration overseas and other developments. In that event, we think the withdrawal from YCC and NIRP would have to wait until 2024 H2 or perhaps even later.

(Research Report published July 28, 2023)