Investor interest in the Japanese economy is increasing globally, due to expectations of an end to deflation. Here we summarize the major events that led to a decades-long deflationary spiral.

The Japanese economy has picked up at times over the 30 years since its economic bubble burst

Japan has been attracting global attention amid prolonged tension between the US and China due to its position as the only Asian member of the G7

Large spring wage hikes may finally trigger a move out of deflation

Investor interest in Japan’s economy is increasing globally, due to expectations of an end to deflation, symbolized by the largest wage hikes for around 30 years and improvement in Japan’s relative position amid US-China tensions.

To understand Japan’s next phase, we take a look back at how the only Asian country in the G-7 lost its position as the leading global economy.

Post-Plaza Accord Yen Appreciation - One Factor Behind Formation of Bubble Economy

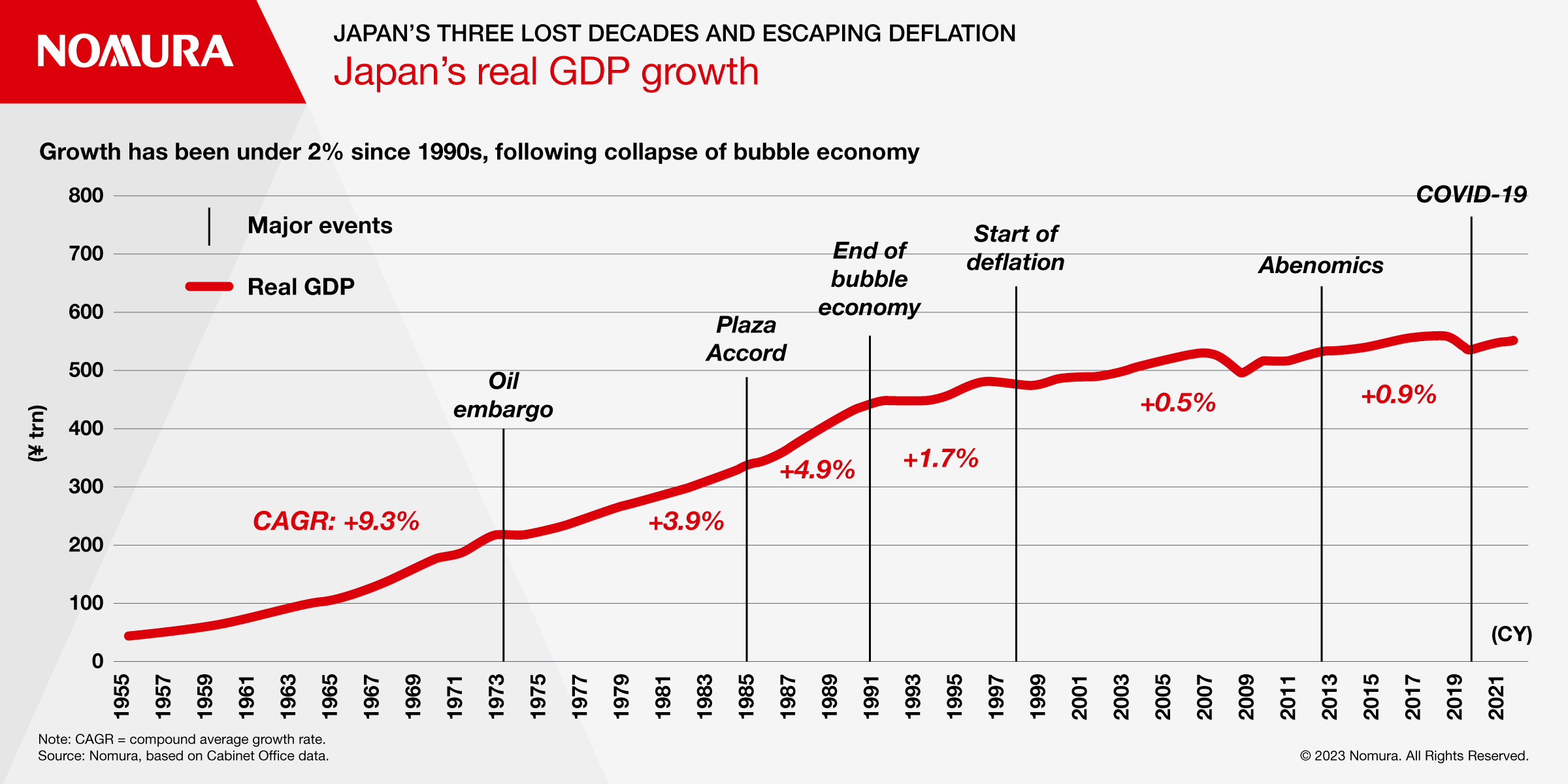

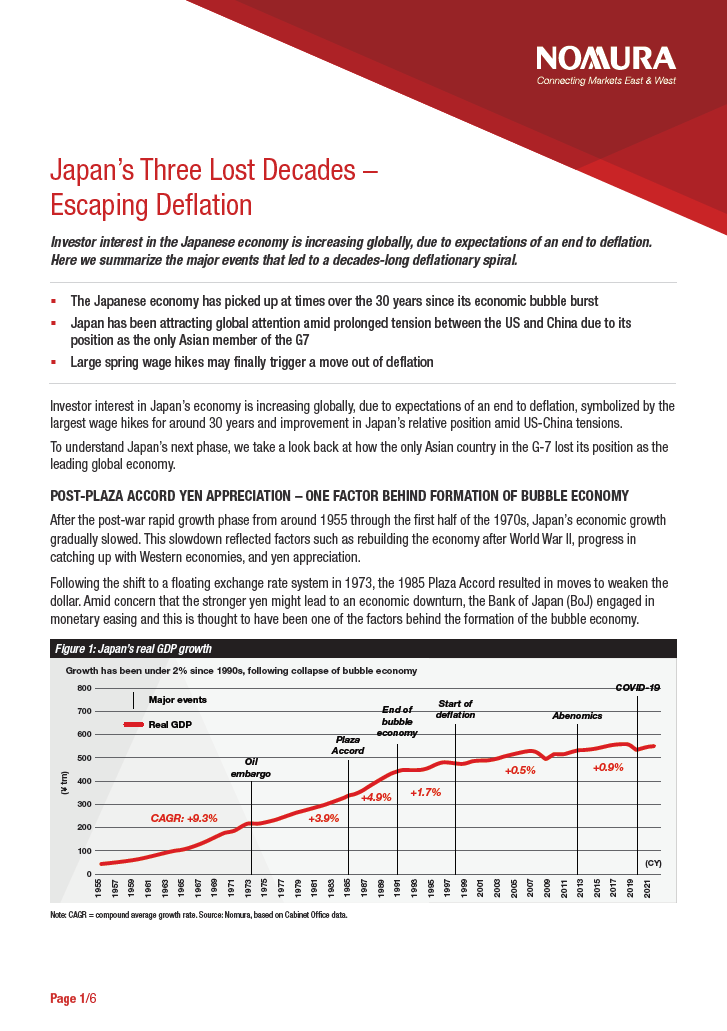

After the post-war rapid growth phase from around 1955 through the first half of the 1970s, Japan’s economic growth gradually slowed. This slowdown reflected factors such as rebuilding the economy after World War II, progress in catching up with Western economies, and yen appreciation.

Following the shift to a floating exchange rate system in 1973, the 1985 Plaza Accord resulted in moves to weaken the dollar. Amid concern that the stronger yen might lead to an economic downturn, the Bank of Japan (BoJ) engaged in monetary easing and this is thought to have been one of the factors behind the formation of the bubble economy.

Figure 1: Japan’s real GDP growth

During this period, the Japanese economy benefited from low inflation despite the sharp rise in asset prices, partly because of the fall in crude oil prices.

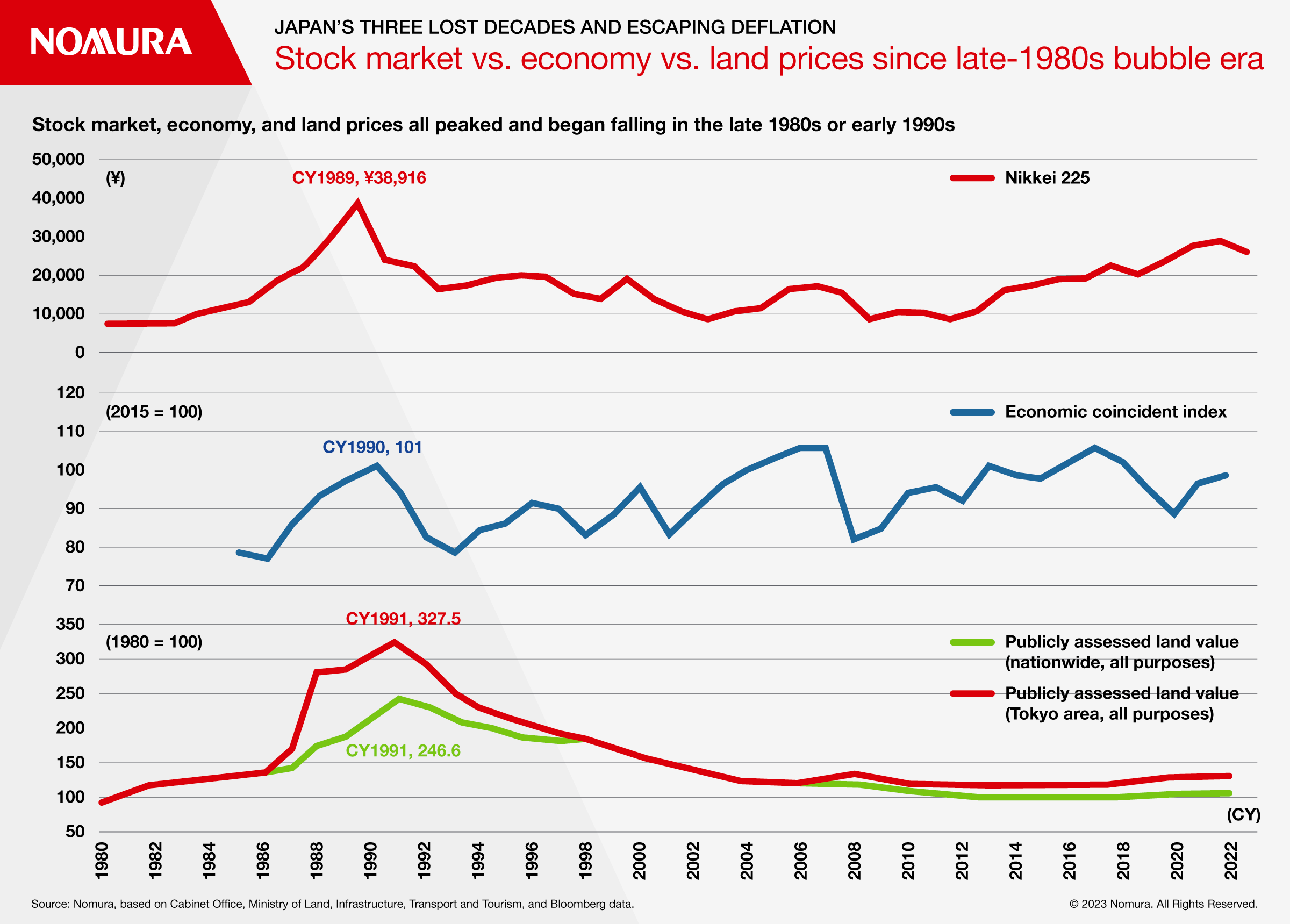

However, share prices, the economy, and land prices started to fall after peaking at end 1989, end-1990 and end-1991, respectively. This marked the collapse of the bubble and the period from then up to the present is called the “lost three decades”.

Japan Enters Deflation in 1998 Following NPL Problem

From the end of the bubble through to around 1997, there were some periods of economic recovery. However, economic growth remained weak compared to the 1980s. As land prices continued to fall, the problem of nonperforming loans (NPLs) at financial institutions increased, resulting in a series of bankruptcies at major financial institutions.

The consumption tax rate was increased from 3% to 5% in 1997, and the summer of that year also saw the Asian currency crisis, putting downward pressure on the Japanese economy from several directions. The period of “Japan as No. 1” was in the distant past as it entered a period of deflation in 1998, with negative GDP deflator growth.

Figure 2: Stock market vs. economy vs. land prices since late-1980s bubble era

Unconventional Monetary Policy

The BoJ embarked on a new phase in 1998 as it implemented independent and transparent policies under the new Bank of Japan Act. The BoJ gradually lowered its policy rate throughout the 1990s, introducing a zero interest rate policy in 1999. This marked the start of its unconventional monetary policy. Although the BOJ ended its zero-interest rate policy in 2000, it introduced quantitative easing in 2001 in the wake of the bursting of the IT bubble in the US.

In short, while AI-based ESG ratings are unlikely to completely replace analysts in the near future, they are a useful tool to complement traditional assessments and help to address biases while improving understanding of evaluation results.

Japan's Unemployment Rate Reached Its Highest Post-War Level

During this period, there was strong downward pressure on wages, with macro-level per-capita average wages falling year-on-year. This partly reflected a change in workforce composition, with a rise in the ratio of part-time workers, and base pay being frozen in around 2002.

However, China becoming part of the global economy might have put deflationary pressure on the Japanese economy by supplying cheap labor. The freeze in base pay was to some extent due to awareness of Japan’s international competitiveness being threatened by wages in Japan being too high. There was a clear change in the Japanese-style employment approach that considers it right that employment is long-term and stable.

External Demand-Driven Economic Recovery in 2000s

The financial crisis of the second half of the 1990s ended in 2003 with the injection of public funds into Resona Holdings. The economy entered the Izanami Boom, the longest period of economic expansion in Japan’s postwar history (at that time). However, partly because of wages being curbed, there was only a muted recovery in private consumption, which accounts for around 60% of Japan’s GDP. Exports gained an increasing presence during this time. China’s position as the “factory of the world” had strengthened after it joined the World Trade Organization in 2001 and Japanese exports to China rose sharply, making Japan known as an economy driven by external demand. At the same time, China becoming part of the global economy put deflationary pressure on Japan by supplying cheap labor.

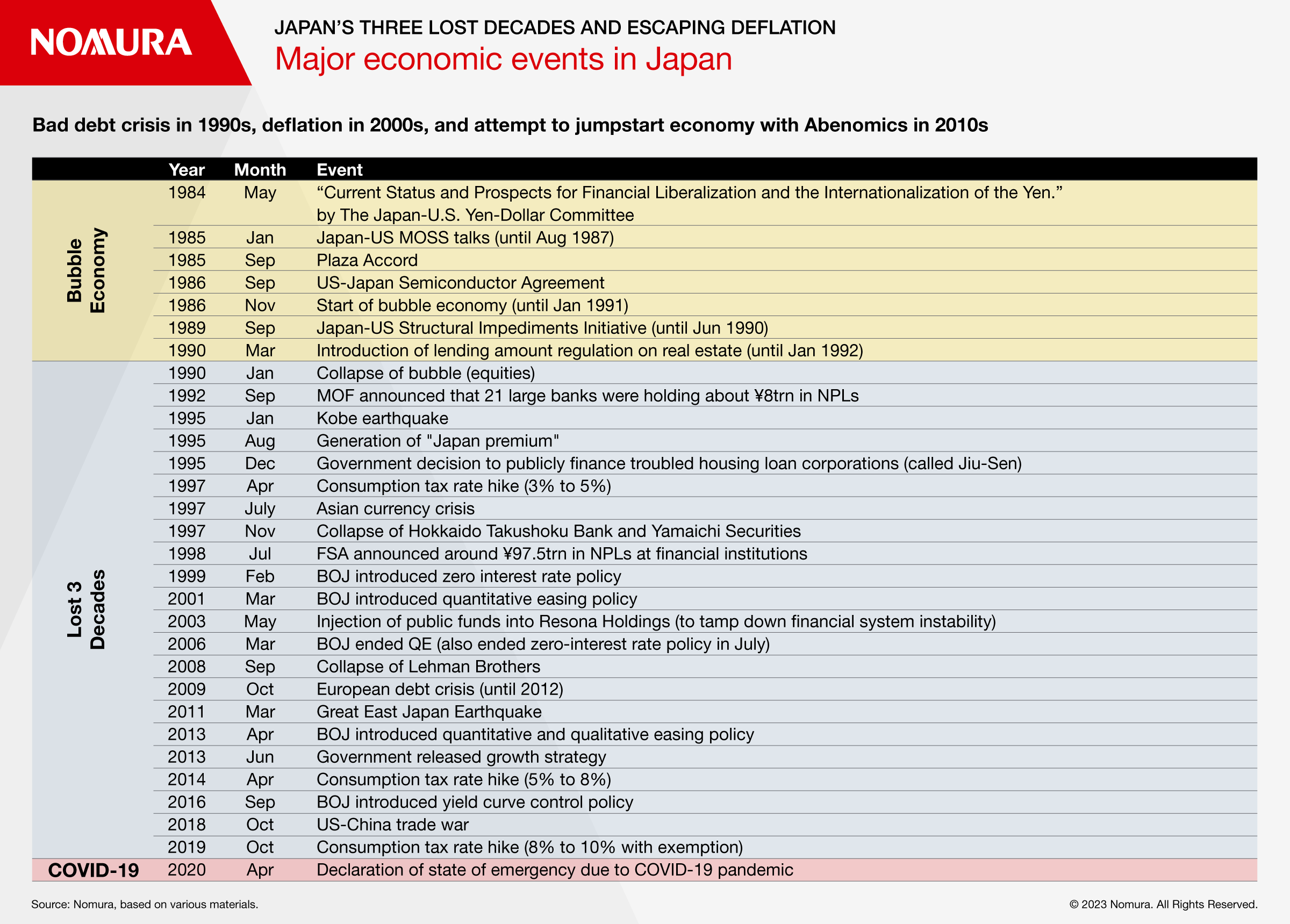

Figure 3: Major economic events in Japan

Facing Deflation Again As A Result of Global Financial Crisis

The 2008 global financial crisis occurred as Japan’s economic recovery remained weak.

The relatively low exposure of Japan’s financial sector to subprime-related products meant that there were no major bankruptcies. However, as economic growth in the 2000s was reliant on exports, there was still a downturn in Japan’s economy on the same scale as that seen in western countries. The Japanese economy once again faced deflation as the 2000s came to a close.

The excessively strong yen/weak dollar, with USD/JPY falling below 76 level, played a large role in the deflation seen at the time, along with the slide in demand accompanying the global recession.

The already appreciating yen, relative to the US dollar, came under further appreciation pressure following the Fukushima Daiichi nuclear power plant accident. In autumn 2011, USD/JPY fell to an all-time low of 75.32.

BOJ Purchases Assets

In response to this situation, the BOJ came up with its comprehensive monetary easing framework, under which it started purchasing long-term JGBs, corporate bonds, commercial paper, ETFs, and REITs. But the yen continued to strengthen against the dollar and core CPI inflation continued to trend in the vicinity of 0%.

Launch of Abenomics With Change In Administration At End-2012

Change came in the latter half of 2012 with the economic policies of Prime Minister Abe (Abenomics). They consisted of a bold monetary policy – in the form of quantitative and qualitative easing - a flexible fiscal policy, and a growth strategy to stimulate private investment

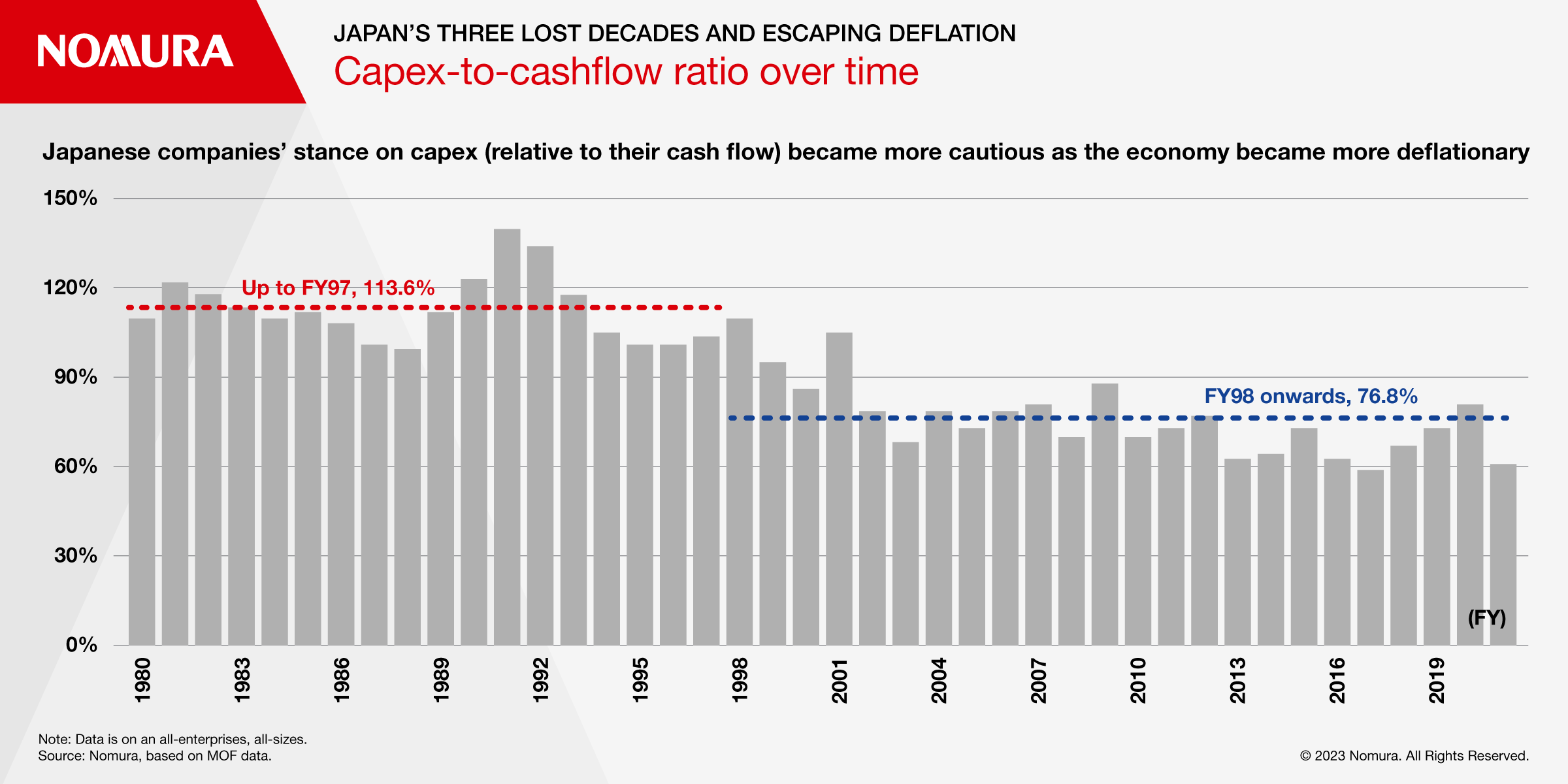

Figure 4: Capex-to-cashflow ratio over time

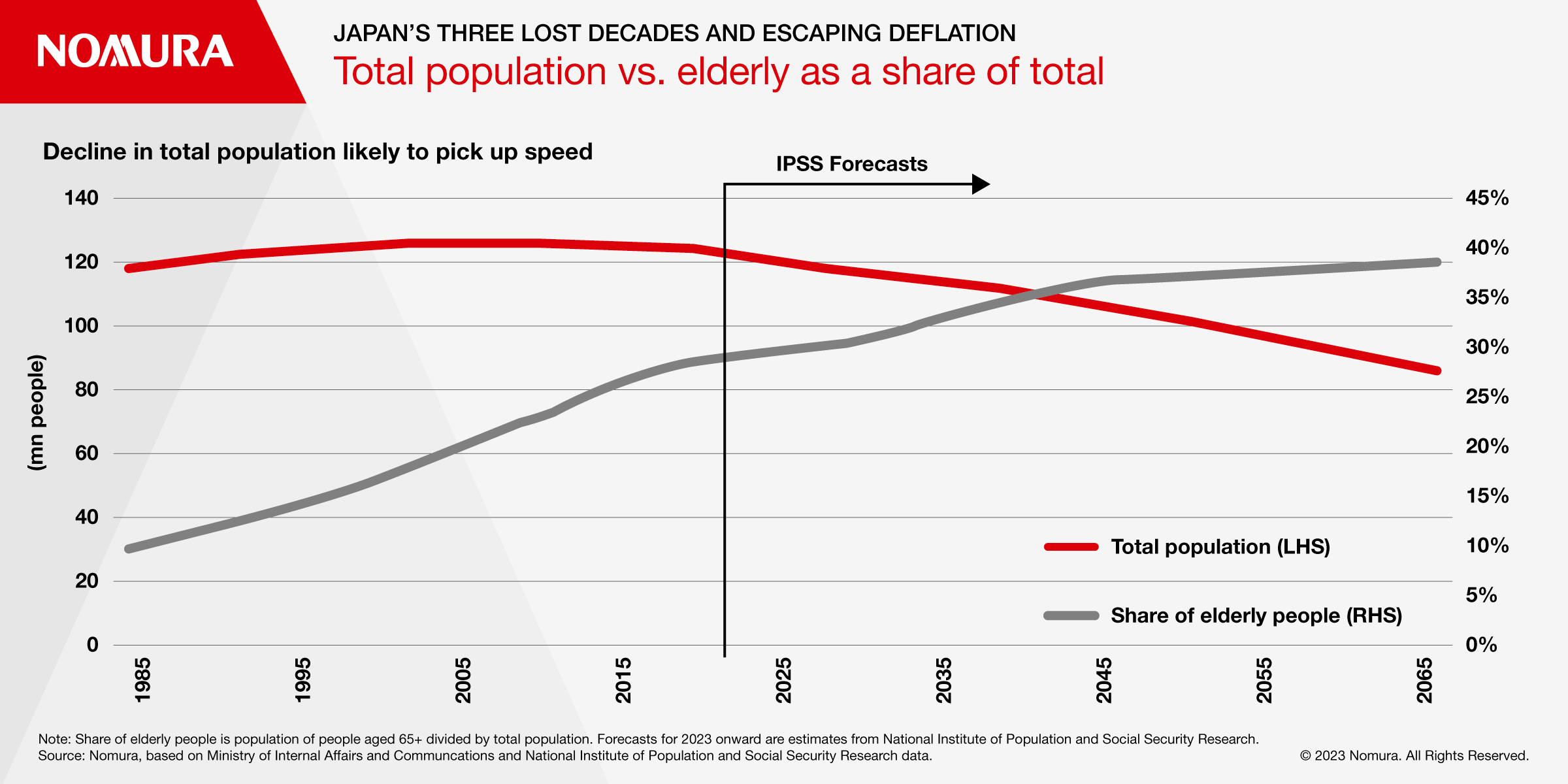

In response to the quantitative and qualitative easing, land and real estate prices rose moderately. Expectations of a rise in consumer prices also grew as population decline led to labor shortages.

Figure 5: Total population vs. elderly as a share of total

The Japanese economy thus looked as though it had taken a firm step toward ending deflation. However, the economic recovery abruptly lost speed when the government hiked the consumption tax rate from 5% to 8% in April 2014. Then BOJ Governor Haruhiko Kuroda committed the BOJ to achieving 2% inflation, but the target of stable inflation was gradually pushed further into the future.

Recognizing this as a problem, the BOJ sprang the huge surprise of negative interest rates in January 2016, leading to widespread disruption; JGB yields fell sharply and the yield curve flattened.

This substantially damaged investment opportunities for ultra-long investors such as pension funds and life insurers. Banks and other financial institutions also had to modify their systems in order to deal with negative interest rates. In response, the BOJ introduced its yield curve control policy in September 2016, which is still in place today.

Highest Inflation Since The 1980s, Largest Wage Hikes Since First Half of The 1990s

Energy, food, and forex dealt a triple whammy of inflationary pressures to Japan’s economy. Core CPI inflation came in at +4.2% y-y in January 2023, its highest level since September 1981.

Meanwhile, the sixth set of data compiled by the Japanese Trade Union Confederation (Rengo) on spring wage negotiations showed base pay growth accelerating sharply to 2.14%, its highest level since the first half of the 1990s.

While much of the spring wage hike in 2023 was to offset inflation, it cannot be explained by faster inflation alone, suggesting that upward pressures on wages as a result of accelerating population decline have finally started to make themselves felt more strongly.

This content has been prepared by Nomura solely for information purposes, and is not an offer to buy or sell or provide (as the case may be) or a solicitation of an offer to buy or sell or enter into any agreement with respect to any security, product, service (including but not limited to investment advisory services) or investment. The opinions expressed in the content do not constitute investment advice and independent advice should be sought where appropriate.The content contains general information only and does not take into account the individual objectives, financial situation or needs of a person. All information, opinions and estimates expressed in the content are current as of the date of publication, are subject to change without notice, and may become outdated over time. To the extent that any materials or investment services on or referred to in the content are construed to be regulated activities under the local laws of any jurisdiction and are made available to persons resident in such jurisdiction, they shall only be made available through appropriately licenced Nomura entities in that jurisdiction or otherwise through Nomura entities that are exempt from applicable licensing and regulatory requirements in that jurisdiction. For more information please go to https://www.nomuraholdings.com/policy/terms.html.