Carbon pricing's importance to economic decisions

The ever deepening focus on sustainable finance is most certainly based in an environmental crisis-led trend, with growing recognition of the criticality of decarbonising the world’s economy. China (by 2060), Japan, South Korea, UK and EU (by 2050) have all recently committed to Carbon Neutrality, and US President Elect Joe Biden also talks in these terms.

Emissions of carbon into the atmosphere must be limited, and foundational economic analysis tells us that carbon emissions should be treated as a scarce resource, and need to be managed by supply and demand dynamics. To achieve this, emissions need to be restrained and priced.

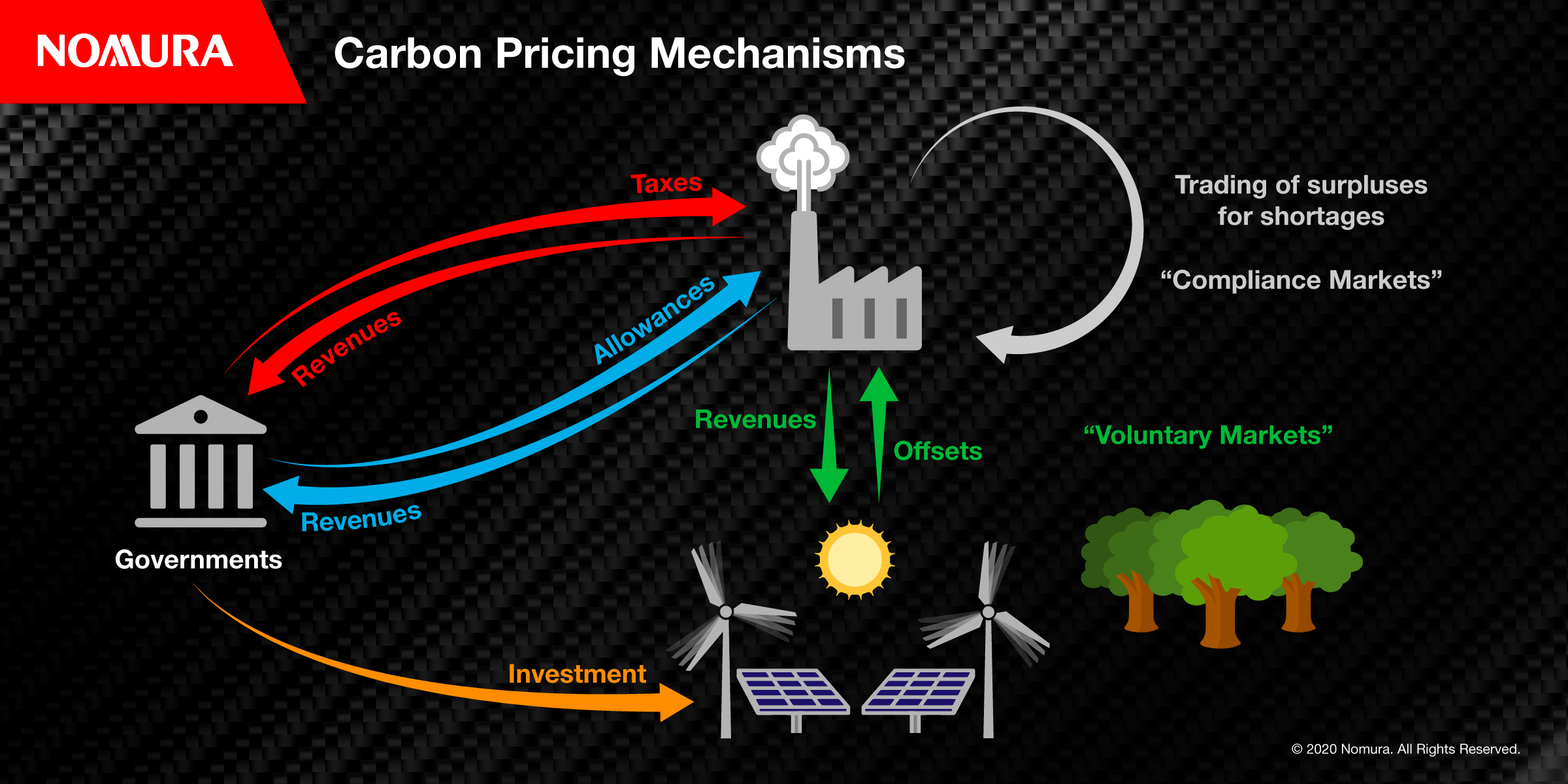

Enter Carbon pricing, it is an approach to reducing carbon emissions that uses multiple instruments to pass on the cost of emitting carbon emissions to the emitters, aka the ‘polluter pays’. In 2020 however, the world economies to a significant extent operate without this price being in place.

The result today is that most businesses operate without adequate consideration of this missing cost. Commercial decisions are made without the full consideration of this externality, and we cannot therefore expect the right decisions.

Tools in the bag to help implement carbon pricing

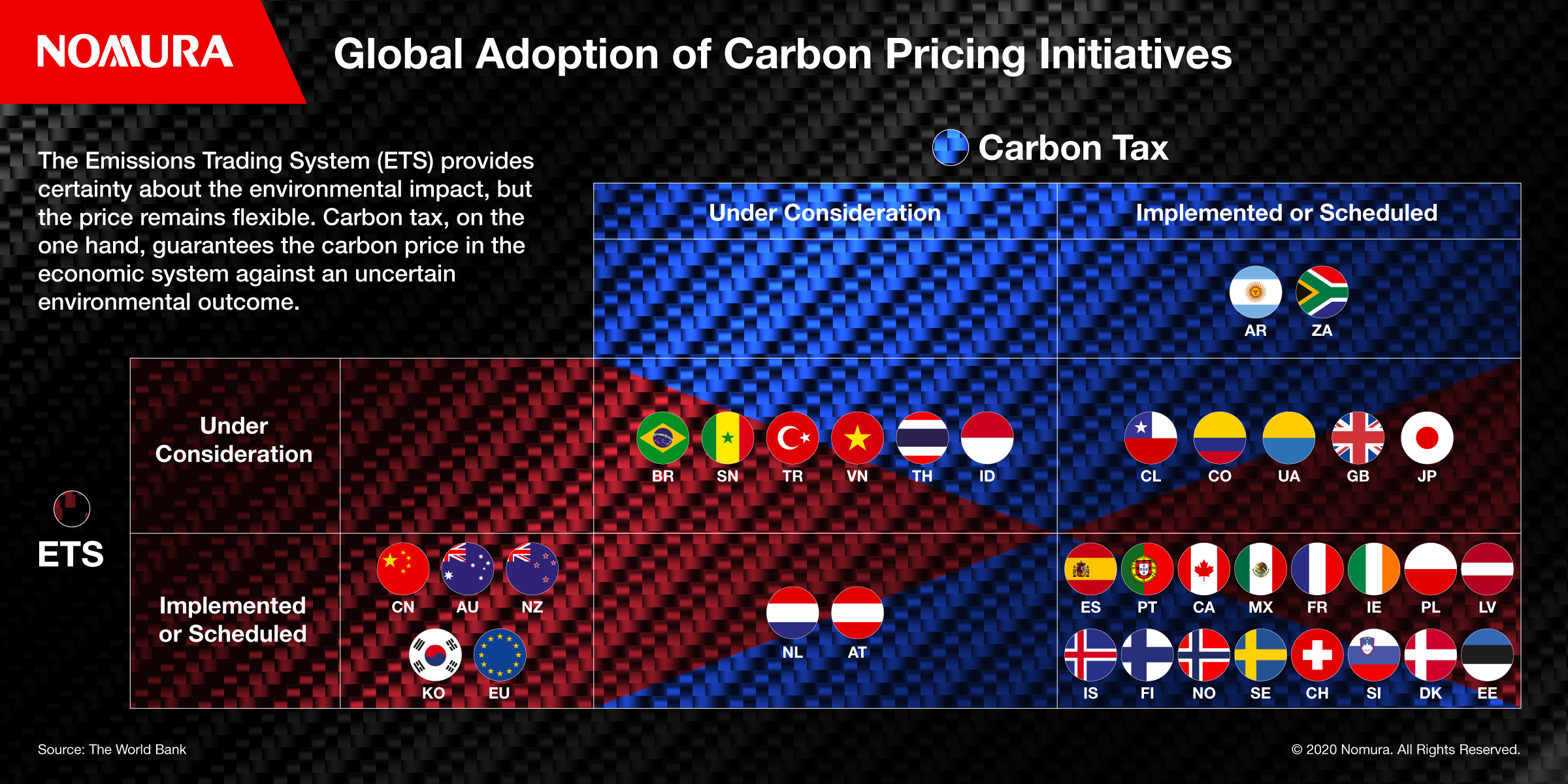

One of the main weapons of choice in the fight against carbon emissions is Emission Trading Schemes (ETS), The Economist has estimated that around 20% of the world’s emissions are today covered by such schemes.

The EU is the largest adopter of ETS, with the EU Green Deal pledging to increase the EU ETS coverage from 45% to 55% of emissions by adding further sectors, and reducing pricing allowances by 2.2% per annum to force change.

China is following suite and is close to implementing its own planned scheme, additionally there are state schemes in the US, and these are likely to get more backing as the US president elect Biden re-joins the ‘Paris Agreement’.

Outside of ETS, governments have taxation as a carbon reduction instrument. Most notably carbon border taxes, which have the aim of not only penalising carbon intensity of imports, or carbon intensive transport costs of those imports, but also protecting the domestic corporates from the arbitrage of operation overseas to avoid other carbon measures.

Economic viability and Financial Services role in helping

Ultimately the need is for sufficiently high carbon pricing that firstly makes legacy carbon intensive activities unviable, and consequently makes low carbon activity, and decarbonisation, economically viable initiatives.

Banks and fund managers should be looking to track the CO2 emission levels of the firms they invest in, and directly seek to lower these through engagement or divestment. More structurally, banking prudential management is increasingly focussed on carbon as a risk factor, where aggressive policy change could have significant impact on high carbon businesses that are unprepared.

Carbon pricing, at meaningful price levels, is a key factor for decarbonisation. Such schemes are also a way for governments to raise finance for other green initiatives, so have a valuable secondary effect.

Governments will, however, need to consider the implications and social policy dynamics of such schemes. Charges on domestic heating and personal transportation has a detrimental immediate effect on society and needs to be considered with balanced social policies.

Read more insights from Nomura Institute of Capital Markets Research (NICMR) here.