China's 14th Five-Year Plan ends this year, with the 15th set to commence in 2026. In our view, China’s five-year planning framework — a legacy from its central planning era — continues to be valuable, offering policymakers and markets an opportunity to review progress and challenges from the previous half-decade while charting a course for the medium to long term.

The two defining factors of China’s economy over the past five years

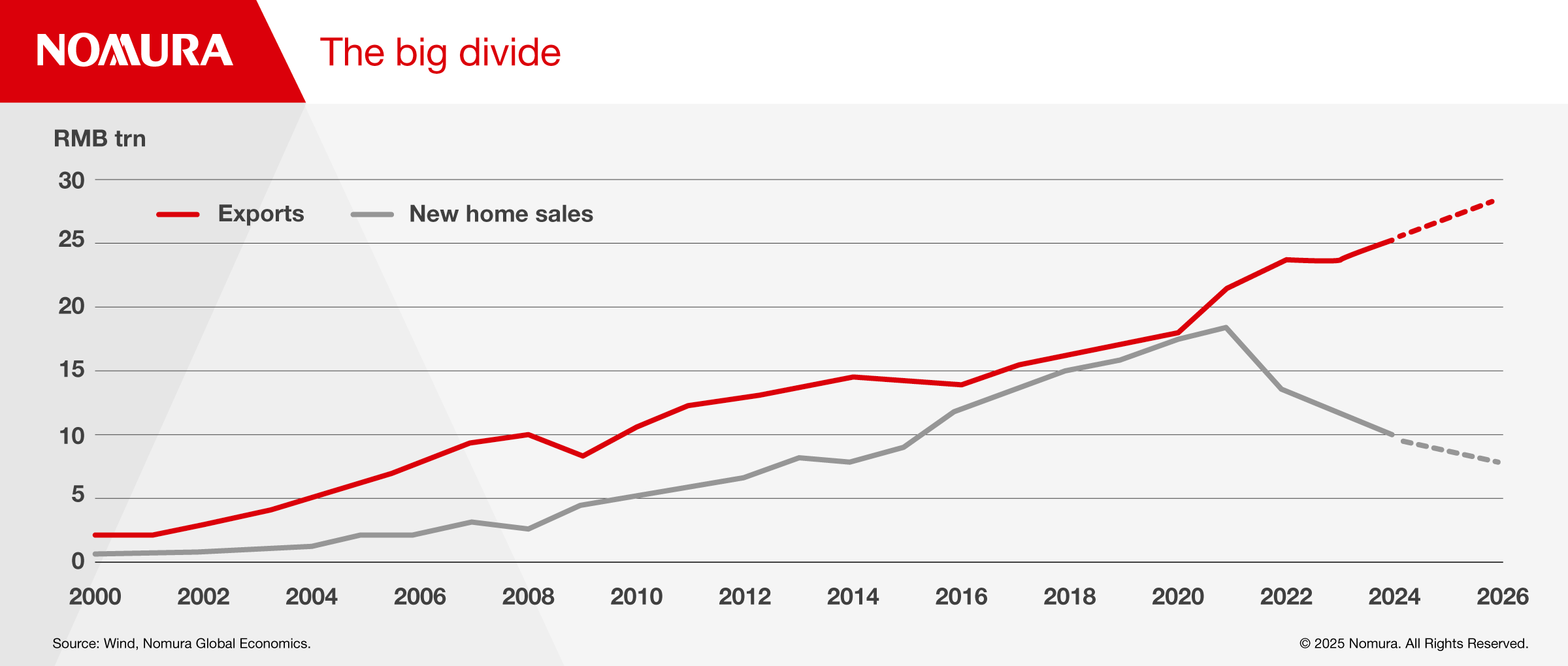

The Chinese economy over the past five years can be summarized in one chart (see below). For the first two decades of the century, the country’s exports and new home sales both trended upward. Those were the golden years. From 2021 onward, however, a stark divergence emerged, with the property sector beginning a steep decline.

According to official data, new home sales have plummeted by over 50% in the past five years, with private sector estimates suggesting an even steeper drop from peak levels. This collapse, compressed into just four and a half years, represents one of the fastest property bubble bursts in modern economic history. The ripple effects are profound: China has experienced deflation since 2022, with 10-year government bond yields falling below Japan's for the first time.

However, the property crisis represents only part of the picture. While domestic demand crumbled, Chinese exports grew at an average annual rate of 7.7% over the past five years, a remarkable acceleration from the approximately 2.2% annual growth in the five years preceding 2021. Without support from such strong export performance, China would likely have experienced deep deflation and recession.

This export boom reflects China's progress in climbing the value chain. Through massive investment in industrial parks, factories, and R&D, China has established dominance in sectors such as automobiles, shipbuilding, and robotics. Beyond high-end manufacturing, China has also become increasingly sophisticated in mining, separating, and processing critical materials, including rare earths, which has given the country bargaining power during trade negotiations with the US.

China has also made significant strides in the development of artificial intelligence. The success of China’s recent AI models serves as a reminder that China performs exceptionally well in this field, perhaps second only to the US.

Lasting recovery requires both domestic fixes and trade strategy

China is unlikely to sustain its exceptional export growth as global trade normalizes and protectionist pressures mount. With property investment continuing to decline at a 20% annual rate and manufacturing investment turning negative, Beijing will need to act decisively.

The government's response thus far — including a 10 trillion-yuan local government debt swap program and stock market interventions — represents important first steps but falls short of addressing the underlying structural issues. Policymakers are running out of easy policy tools. Over the past 18 months, they implemented relatively straightforward measures such as retail sales stimulus, property market support via eased restrictions and lower mortgage rates, and local government debt relief.

In our view, the 15th Five-Year Plan will need to address the more difficult policy issues, such as how to manage the cleanup of the property sector, maintain competitiveness in an increasingly challenging global trade environment, and boost consumption.

We expect annual GDP growth to slow in 2026 to around 4.3%. Also, if China’s export growth slows from about 8% to between 3% and 5%, that will not offset the sharp decline in the property sector. It will be essential for the government to become much more serious about dealing with property-sector problems. We believe there will be moderate deflation again next year, as well.

China will have to be more proactive in the coming months — such as by introducing a new round of support measures — otherwise it may risk deeper deflation, below-target growth, and potentially greater social instability.

The US–China rivalry will also be a central theme for the next five years. While China's improved performance across many sectors can sustain reasonable export growth, it will face increasing trade barriers — not only from the US but also from European countries and emerging markets — as China's manufacturing strength pressures domestic industries in those economies.

Social reform is imperative to boost consumption

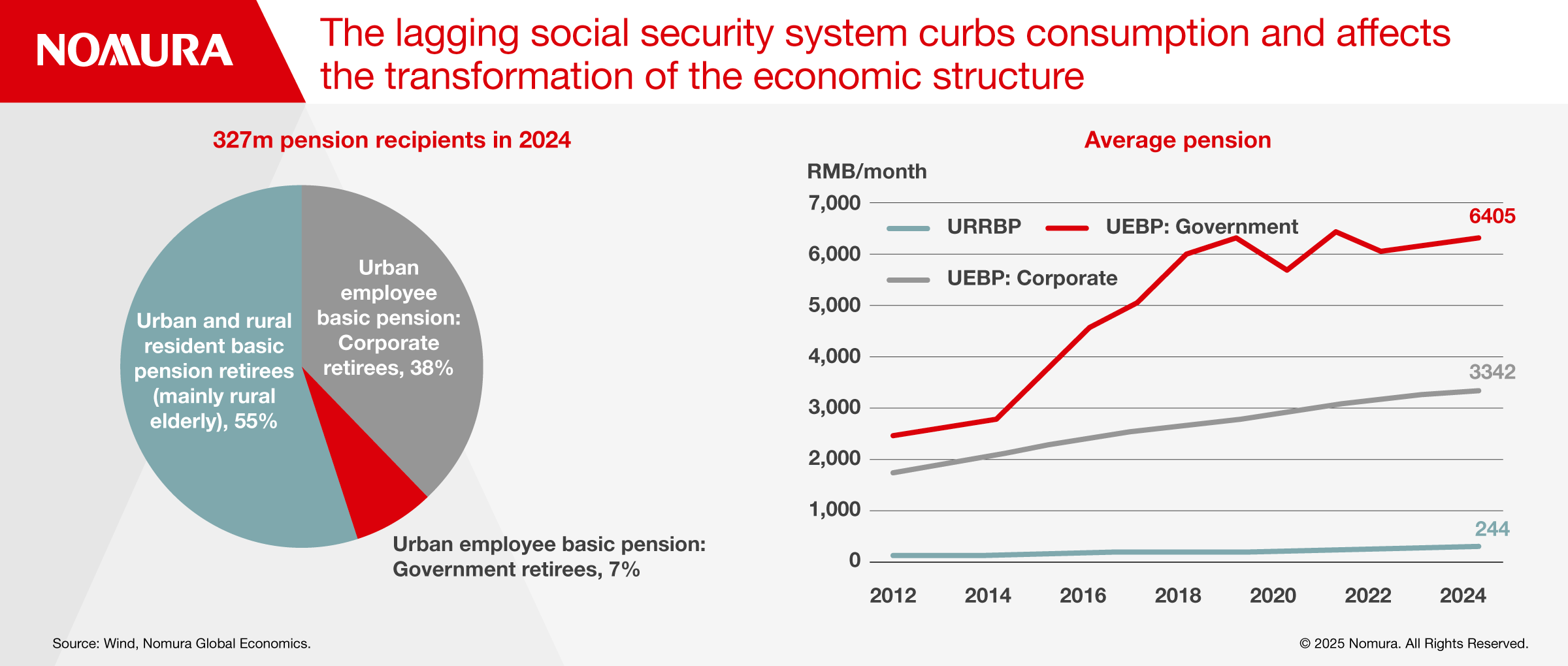

With slower export growth and limited prospects for recovery in the property sector, China will face pressure to boost consumption. To accomplish this, the government will need to significantly strengthen its social welfare system.

Over the next five years, China should act decisively to introduce policies to raise pension income for the significant proportion of pensioners who are currently receiving the equivalent of only one US dollar per day, which is below the poverty line. It is critical for the government to extend comprehensive pension programs to the broader population and address youth unemployment, which is at almost 20%.

The success of China's 15th Five-Year Plan will ultimately depend on Beijing's willingness to tackle these structural challenges head-on, balancing the need for economic stability with the imperative for meaningful reform.