Central Banks | 3 min read June 2026

Economics | 3 min read | February 2023

Economics | 3 min read | February 2023

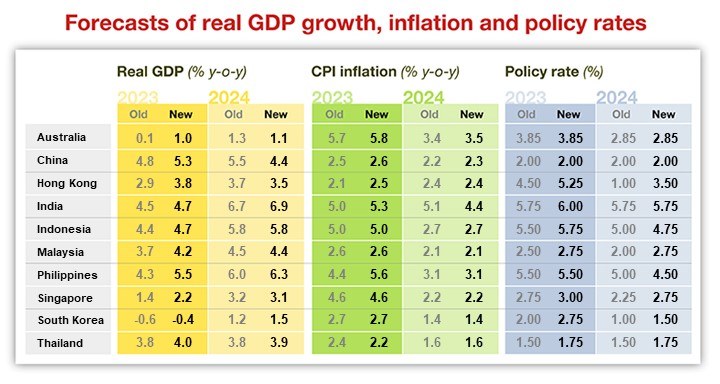

Over the last month, our global view has become more optimistic. We have raised our 2023 GDP growth forecasts for China, following its abrupt reopening in December, and the US, due to its stronger-than-expected labor market. As such, we have also raised our GDP growth forecasts for Asia to 3.6% in 2023 from 3.2% previously. However, good news for the US and China is not all good news for Asia, because a services-driven recovery in China and the US will not benefit Asia’s goods manufacturing hubs, while tighter financial conditions due to a hawkish Fed could weigh on Asia’s domestic demand. A growth slowdown and policy easing, even if delayed, remain our base case for Asia.

That service-related industries are proving more resilient to the global growth slowdown than goods-related industries is not a particularly favorable backdrop for Asia. The reason is that service industries are mostly domestically oriented, having only a small internationally tradable component, with tourism being an exception. The implication is that Asian exports are likely to remain in a slump in coming months.

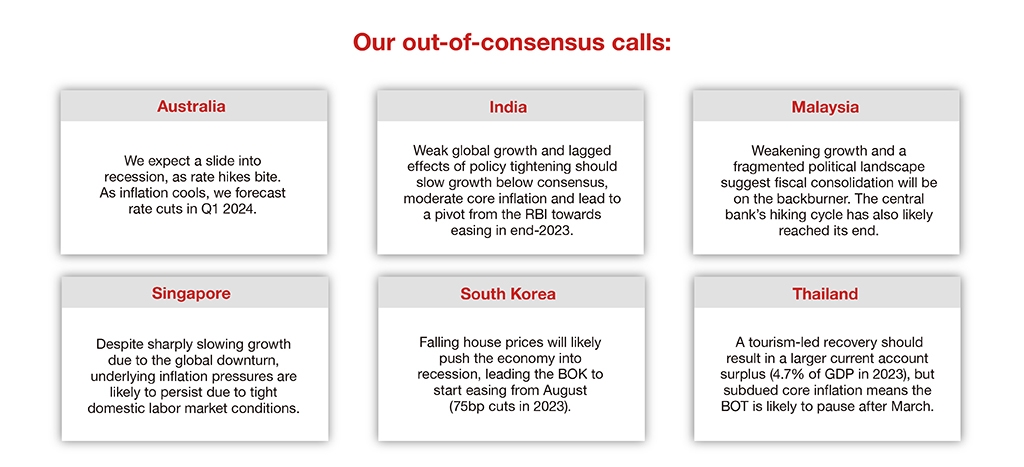

A big benefit to some Asian economies will come from China’s outbound tourism. The upward revision to our forecast for Hong Kong’s GDP growth reflects this anticipated benefit. Singapore’s services sector should also benefit from the border reopening which could partially offset the goods export downturn. However, we have only marginally increased our Thailand growth forecast as weak government spending could be an offset. India is unlikely to benefit from China’s reopening, but will be impacted by tighter financial conditions. A hawkish Fed could delay rate cuts in South Korea, thereby prolonging the housing downturn.

Even as we raise our projections, we believe Asia’s ongoing growth slowdown has further to run. Despite the euphoria around China’s growth rebound, what matters for Asia are its drivers. While China’s outbound tourism rebound will be positive for some economies, a moderation in China’s passenger car sales this year and a slower recovery in its property investments could be a drag. Already, the spillover effects from weak China demand last year and slowing final demand from the US and Europe have manifested in the form of an export downturn, and steep industrial production cuts across Asian economies.

We still expect weaker growth in the region in H1 2023, due to weaker exports and an inventory destocking cycle. The second half of the year should take a turn for the better, reflecting improved tech demand and some spillover effects from a recovering China. However, a higher-for-longer Fed, delayed policy easing in Asia and our view that China’s growth will slow again in 2024 increase the risk that this expected growth rebound may not sustain.

On inflation, there are no major changes to our forecasts since oil prices remain stable, global food prices continue to moderate, and slowing demand should ease core inflation from Q2 2023 onwards. Singapore is an exception, where inflation should increase due to the influx of Chinese tourists.

For more on our 2023 growth projections, read our full report.

Head of Global Macro Research

Chief Economist, India and Asia ex-Japan

Economist, Asia ex-Japan

This content has been prepared by Nomura solely for information purposes, and is not an offer to buy or sell or provide (as the case may be) or a solicitation of an offer to buy or sell or enter into any agreement with respect to any security, product, service (including but not limited to investment advisory services) or investment. The opinions expressed in the content do not constitute investment advice and independent advice should be sought where appropriate.The content contains general information only and does not take into account the individual objectives, financial situation or needs of a person. All information, opinions and estimates expressed in the content are current as of the date of publication, are subject to change without notice, and may become outdated over time. To the extent that any materials or investment services on or referred to in the content are construed to be regulated activities under the local laws of any jurisdiction and are made available to persons resident in such jurisdiction, they shall only be made available through appropriately licenced Nomura entities in that jurisdiction or otherwise through Nomura entities that are exempt from applicable licensing and regulatory requirements in that jurisdiction. For more information please go to https://www.nomuraholdings.com/policy/terms.html.

Jump to all insights on Economics

Central Banks | 3 min read June 2026

Economics | 15 min video February 2023

Economics | 3 min read February 2023