Inflation Outlook and ECB Position:

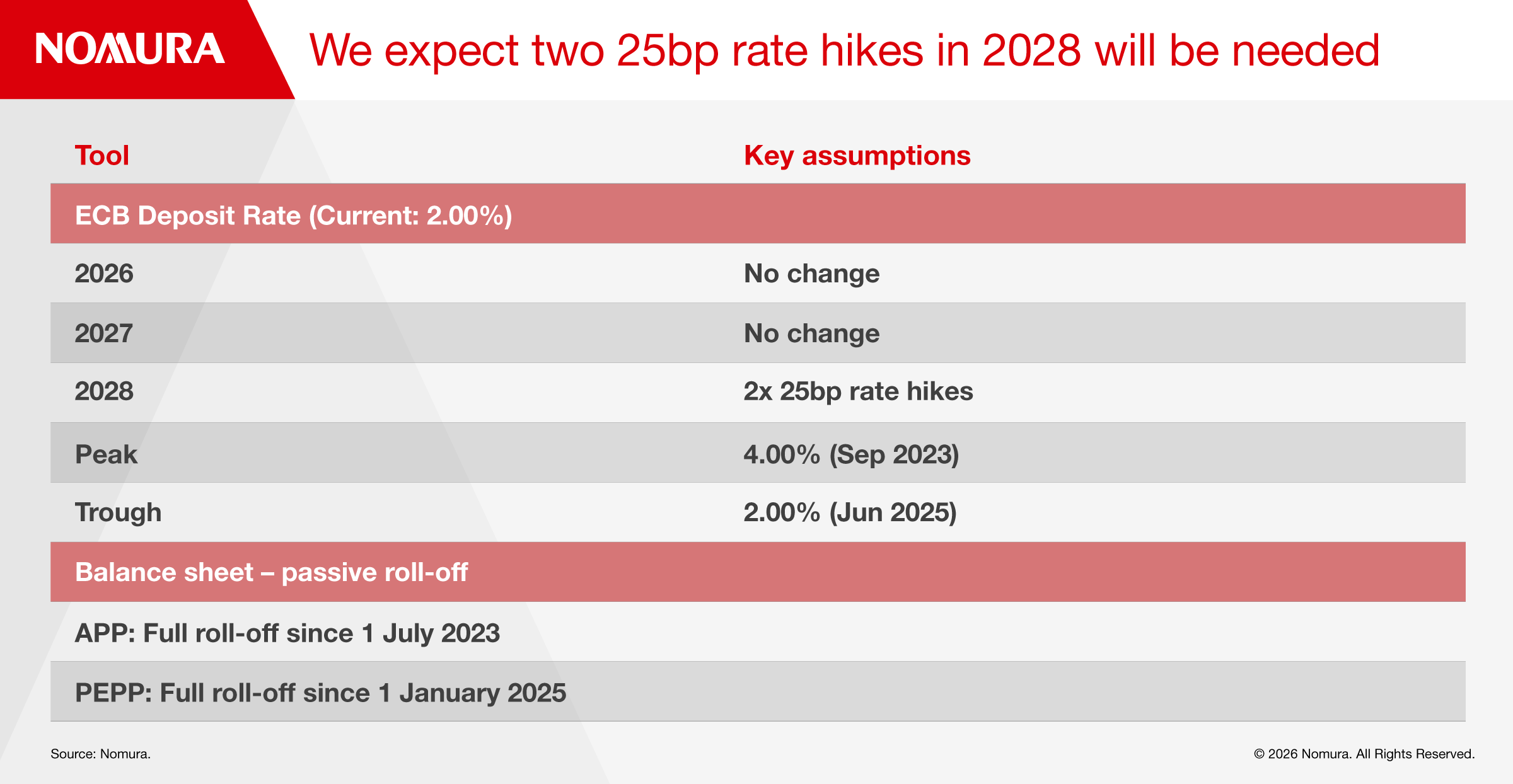

We forecast euro area inflation to average 1.8% this year and 2.0% next year. While inflation risks are skewed to the downside this year, they are skewed squarely to the upside in 2027 and, in particular, in 2028. We believe the ECB will remain on hold for the foreseeable future, but we believe the next move will be a hike rather than a cut. We believe the ECB will need to raise rates at least 50bp in 2028 (two 25bp hikes) to ensure inflation remains around target in 2028.

Euro area HICP inflation declined by 0.3pp to 1.7% y-o-y in January 2026, and we expect it to print modestly below the ECB's 2.0% target in H1 2026 owing to energy base effects, before rising to around target through the end of 2027. ECBspeak on the whole, has been clear that the ECB is in a good place, as ECB staff forecast HICP inflation to be around the 2.0% target in 2028. Some ECB Governing Council members, like Schnabel, have argued that the next move is more likely to be a hike than a rate cut.

Downside Risks for 2026:

While we forecast euro area inflation will hover around the ECB’s 2.0% target for most of 2026 and 2027, inflation risks for 2026 are skewed squarely to the downside, owing to the following reasons:

- Crude oil prices fell by 20% in 2025, and natural gas prices contracted by 42%. We believe there could be further pass-through from lower energy prices to headline HICP inflation.

- EUR/USD rose by around 13% in 2025, and the ECB estimates a 10% appreciation in the euro lowers headline HICP by around 0.4% within a year.

- There is an elevated risk that China will dump cheap goods in Europe due to US tariffs.

Despite the potential for near-term inflationary undershoots, we do not expect the ECB to react to any below-target inflation prints this year. The ECB is now squarely focused on its end-of-horizon forecast, which is currently 2028, rather than near-term deviations.

Upside Risks for 2027-2028:

Importantly for the ECB, inflation risks in 2027 and, in particular, in 2028, are skewed squarely to the upside.

The euro area unemployment rate was 6.2% in December 2025, its lowest on record. The European Commission estimated the equilibrium unemployment rate was 6.6% in 2025, meaning the unemployment rate is 0.3pp below its equilibrium. We expect the unemployment rate to continue falling in 2026, 2027 and 2028 and for the wedge with the equilibrium rate to remain important by end-2028. Services and manufacturing firms continue to cite acute labour shortages, further underscoring the euro area's tight labour market. This tightness in the labour market is likely to add wage growth pressures over the forecast horizon.

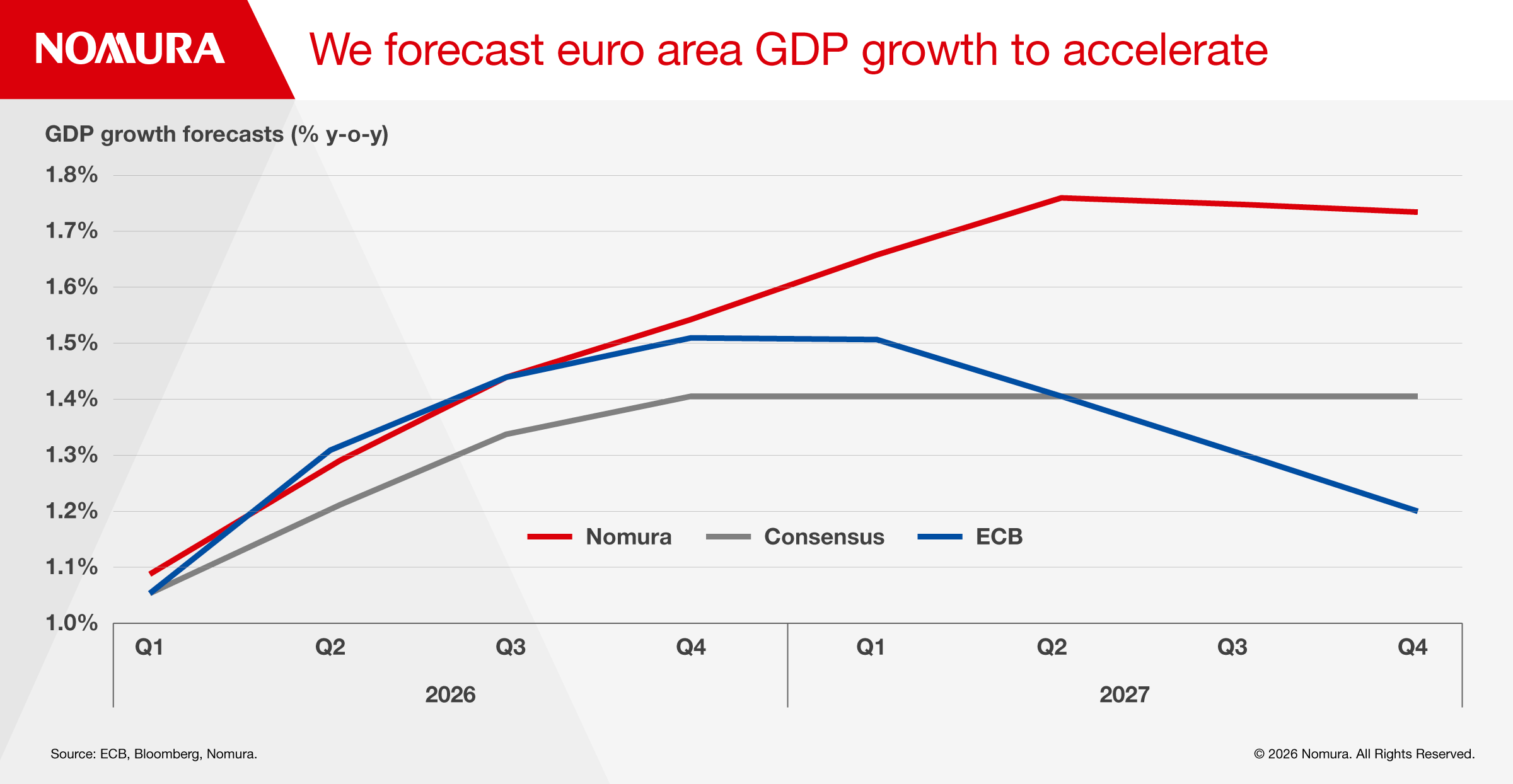

We forecast euro area GDP growth to accelerate in 2026 and 2027, before settling between 1.7 and 1.8% y-o-y from Q2 to Q4 2027. The consensus appears to believe that potential growth in the euro area stands at 1.1%, and we pencil euro area potential growth at around 1¼%. If potential growth is indeed 1.1-1.2% y-o-y and our GDP growth forecasts of 1.7-1.8% materialise, this could result in meaningful inflationary pressures.

We believe that the near-term impact from US tariffs is disinflationary, as US tariffs will lower euro area GDP growth and there is a risk of China dumping cheap goods in Europe. However, in the medium term, tariffs tend to be stagflationary as they upend value chains and result in trade disruptions and distortions.

The Bottom Line:

In our view, it appears we are moving into a pre-financial crisis world where the labour market is tight, the unemployment rate is below the equilibrium unemployment rate, and GDP growth is above potential. We forecast euro area GDP growth markedly above the forecasts of the ECB and consensus in 2027, which are likely to add meaningfully to domestic inflationary pressures towards the end of 2027 and, in particular, in 2028.

Hence, we believe the ECB's next move will be to raise rates rather than to cut rates, and we expect the ECB will need to raise rates twice by 25bp in 2028 to ensure inflation remains around target. The risk is that the hikes eventually occur earlier, in 2027, should inflationary pressures prove stronger than we have penciled in.