A fragile economic recovery

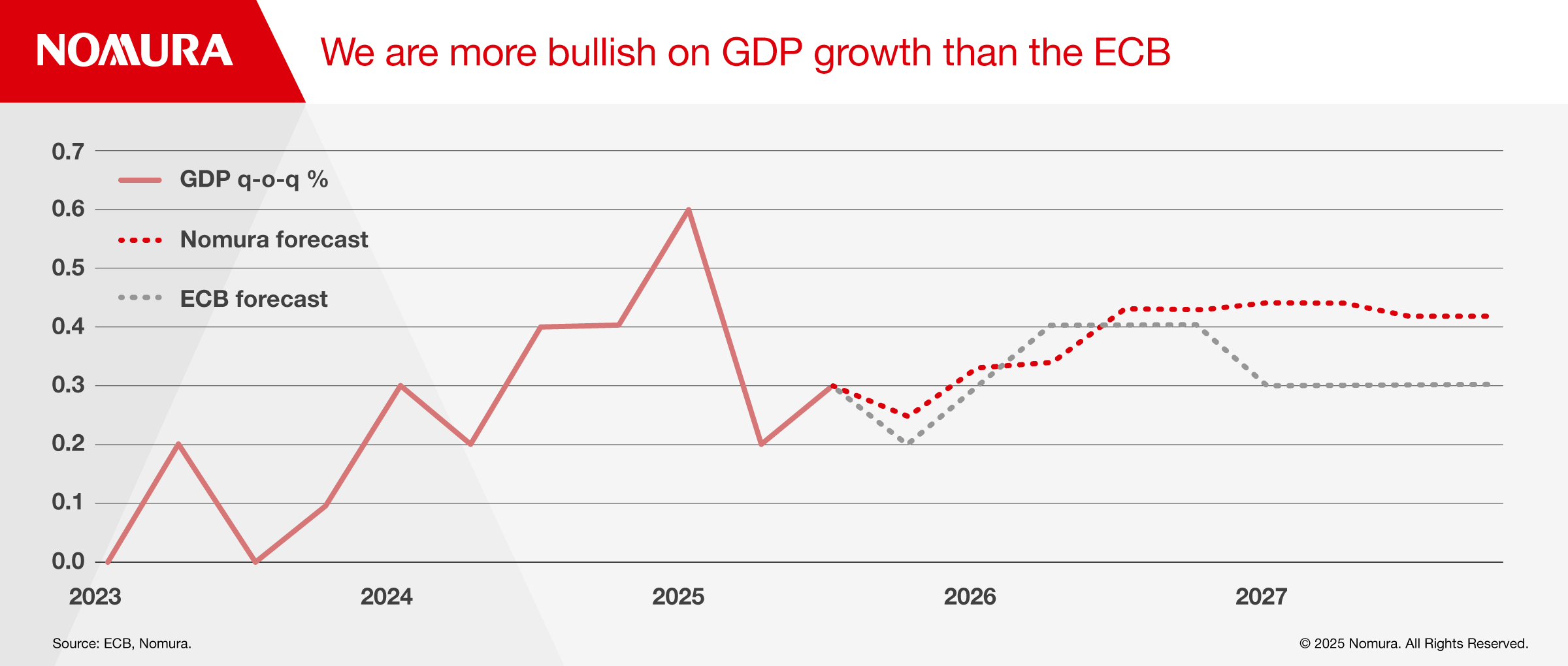

We forecast GDP growth in the euro area to accelerate gradually over the next year, expecting 0.2% q-o-q growth in Q4 2025 to double to 0.4% q-o-q by H2 2026 (Figure 1).

We believe the key drivers of economic activity in 2026 include German infrastructure and euro area defence spending, a gradual recovery in household consumption growth and lower interest rates than persisted from H1 2023 to H1 2025.

Low inflation, a falling unemployment rate, rising disposable income and a gradual moderation of household savings should support a recovery in household spending. However, the consumer recovery remains fragile, and wage growth is likely to slow in 2026, so we do not expect a full recovery in household consumption to pre-pandemic growth rates in 2026.

Downside risks to GDP growth in 2026 include fiscal spending taking longer to materialise, and fiscal tightening in some countries, including France and Spain, limiting the impact of German loosening.

Furthermore, while German fiscal spending should boost infrastructure investment, underlying structural issues, such as increased competition from China and a shift to electric vehicles will continue to weigh on the economy. US tariffs may also hit euro area exports in 2026 by more than we have factored into our forecasts.

Undershooting the target

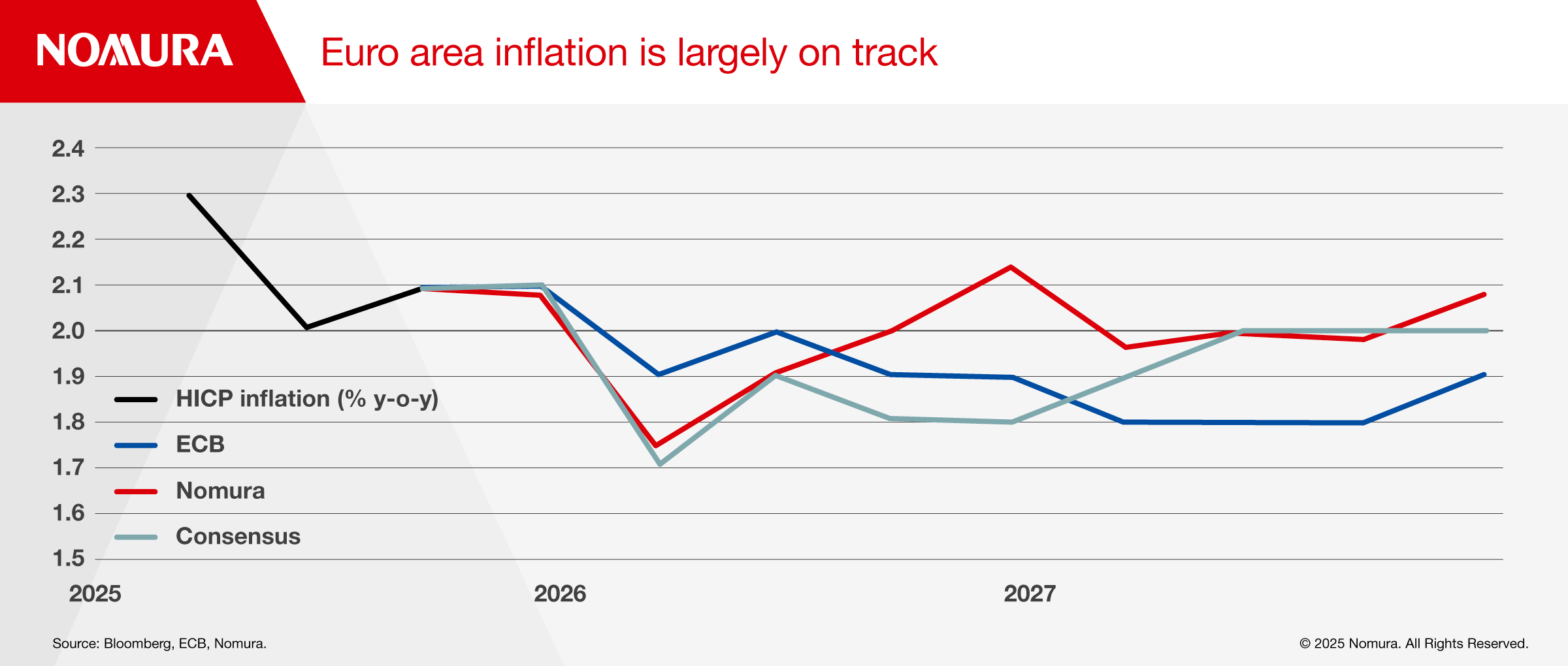

In our view, inflation is no longer a concern in the euro area, and the ECB has largely done its job of returning it to target. We forecast HICP inflation will remain around the ECB’s 2.0% target for most of our forecast horizon (through end-2027; Figure 2) and will average 1.9% in 2026 and 2.0% in 2027.

Risks to the ECB’s 2.0% target for most of the forecast horizon are skewed to the downside as follows:

- Wage growth risks settling at a level below that which is consistent with 2.0% HICP inflation.

- Crude oil is 17% cheaper as of end-November than at the start of 2025, and natural gas is 41% cheaper. We believe there could be further pass-through from lower energy prices to headline HICP inflation.

- EUR/USD has risen by around 12% since the beginning of 2025 and not all of the euro’s appreciation has passed through into HICP inflation.

- There is a strong risk that China will dump cheap goods in Europe due to US tariffs. European Commission and Bank of England analysis suggests this is already occurring in some items, albeit with the risk that it becomes more pronounced and meaningfully weighs on core goods prices.

Upside inflation risks are more limited. We are sceptical that Germany’s fiscal bazooka (€1trn over 10 years) will lead to meaningful inflationary pressures due to ample spare capacity in Germany and a high level of underemployment in the manufacturing and infrastructure sectors.

Fiscal’s time to shine

With the ECB's policy rate at neutral, fiscal policy has quickly taken over as Europe’s most pressing matter. For some countries with fiscal room (Germany, for example), the focus is on how increased spending would support growth. Others, such as France, are fiscally and politically challenged.

Across all of Europe, Germany stands out as being the only major country that can afford to support the recovery process with grand-scale fiscal loosening. An end to the war in Ukraine would likely contribute to an even speedier economic recovery on account of Germany’s greater reliance on the manufacturing, construction and export sectors. We believe Europe would likely fund an important element of Ukraine’s reconstruction and European firms, notably German firms, would likely reap the benefits of going in to rebuild Ukraine.

United Kingdom: A normalising economy

Growth uninspiring, but recovering

While surveys point to an ongoing expansion, they suggest subdued near-term growth. We expect a return to trend growth (around 1.5% annualised), but only by H2 2026.

Our GDP growth forecasts are similar to those of the Bank of England (BoE) and consensus – a recovery from Q3’s slow 0.1% q-o-q pace to 0.3% q-o-q in H1 2026 and 0.4% q-o-q from H2 2026. The outlook for global growth will be an important determinant of UK growth, being a highly open economy, while a better tariff outcome than its peer group could limit the fallout on UK growth.

Fiscal policy is being tightened, but as recently announced tax hikes are back-loaded, this could dent the Labour government’s chances at the next election (no later than August 2029). As official interest rates remain above neutral, we expect a further 25bp of easing, with the final rate cut this cycle expected in April 2026 (3.50% terminal).

Labour market slowdown accelerating

Labour market activity has been slowing more aggressively in recent months with an increased focus on the unemployment rate, having risen more markedly than in other major developed markets over the past year.

In addition, payrolls are falling at around a 0.5% y-o-y pace, while the annual growth in workforce jobs is at a four-year low.

As a result of these loosening trends, wage growth has also slowed.

Leaving sticky inflation behind?

Headline annual rates of CPI inflation should fall especially sharply as rises in administered prices, which took effect in 2025, drop out of the annual comparison. Notably, VAT on school fees will drop out from January 2026, while water/sewerage, vehicle taxes and energy prices will drop out from April 2026. More importantly, we think the momentum in underlying prices will slow as wage growth continues to moderate.

Closing in on neutral rates

As surveys are pointing to slow economic growth, the labour market is weakening and inflation is easing, the BoE has space to ease monetary policy modestly further. But a combination of still-elevated services inflation and delayed fiscal tightening in the latest budget suggests the Bank will proceed in cutting rates with caution.

Türkiye Deep-Dive: Carry on

Political support for the new economic programme continues. We expect the disinflationary policies to remain intact over the next year. We expect the CBRT to continue with its cutting cycle as inflation slows. Our forecast for inflation at end-2026 is 21.1%, down from 31.0% at end-2025. We see room for 1000bp in cuts and forecast the policy rate at 28% by end-2026, down from 38% in December 2025. Several factors support our view:

- Budget performance is better than expected;

- Monetary stance is unlikely to ease despite cuts;

- GDP growth will likely remain below potential;

- Current account balance is likely to widen, but only slightly;

- Risk scenario.

Overall, we remain bullish on Türkiye, while cautiously monitoring political developments. An earlier-than-expected election or a referendum for constitutional change could shift our views, but we believe the probability of such events is low. Geopolitical developments are also important. A Russia-Ukraine peace deal would be positive for Türkiye, as it has strong economic relations with both countries. Oil prices that are below market expectations would also be positive, as Türkiye is a major energy importer. Every USD10 change in the oil price impacts the current account balance by USD4-6bn and inflation by 1.2%.

Read the full report here: Global Macro Outlook 2026