Europe 2024 Outlook – Will Inflation Get Back To Target?

We forecast a very benign recession in the Euro Area, lasting three quarters from Q3 2023, and lopping only 0.5% off GDP. In the UK, economic growth has slowed but remains resilient. We forecast only mild, and short, near-term recessions, with risks in both directions.

Euro Area inflation is declining more sharply than we had expected, though the evolution of services inflation will be greatly dependent on wage pressures.

We believe the ECB is done with its hiking cycle. In our view, the ECB is likely to begin its cutting cycle only in June 2024.

Fiscal policy looks to be less accommodative in 2024 than it has been in the years since the pandemic.

Euro Area

The Growth Outlook – Weak, But Not Collapsing

Surveys may have overstated the expected economic downturn during 2022 and 2023, but nonetheless, official activity data appear to be finally turning too. We expect a mild three-quarter recession spanning late 2023 and early 2024.

Economic growth has already been marginally weak in Q3 2023 (-0.1% q-o-q), and we forecast it to also print negative in Q4 2023 (-0.3%) and Q1 2024 (-0.1%). After this we see a very gradual ascent back to trend growth, which we estimate to be around 0.3% q-o-q, and which we think will only be achieved by the start of 2025.

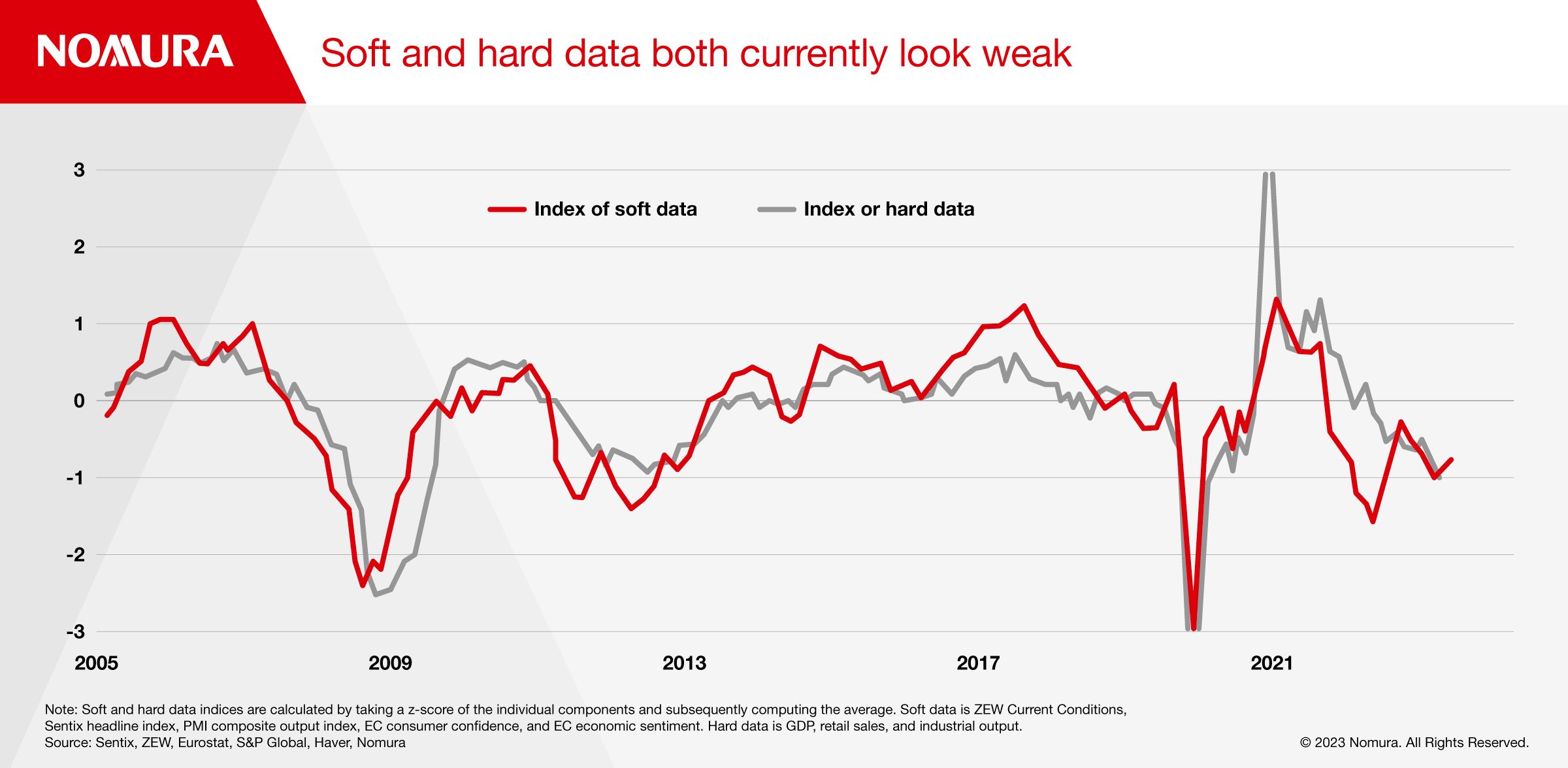

Surveys gave a confusing signal at the end of 2022, falling sharply, while hard data proved to be more resilient than these surveys implied. Some official data have begun to turn negative, notably industrial output, construction, and retail sales, and so there appears to have been some convergence between hard and soft data.

Soft and hard data both currently look weak

That said, we remain cautious about reading too much into the relationship between survey data and official data; notably, the PMI data suggest output should be rather weaker than it is. Taking stock of both survey and official data, these broadly support our mild recession view.

The Return of Real Wage Growth

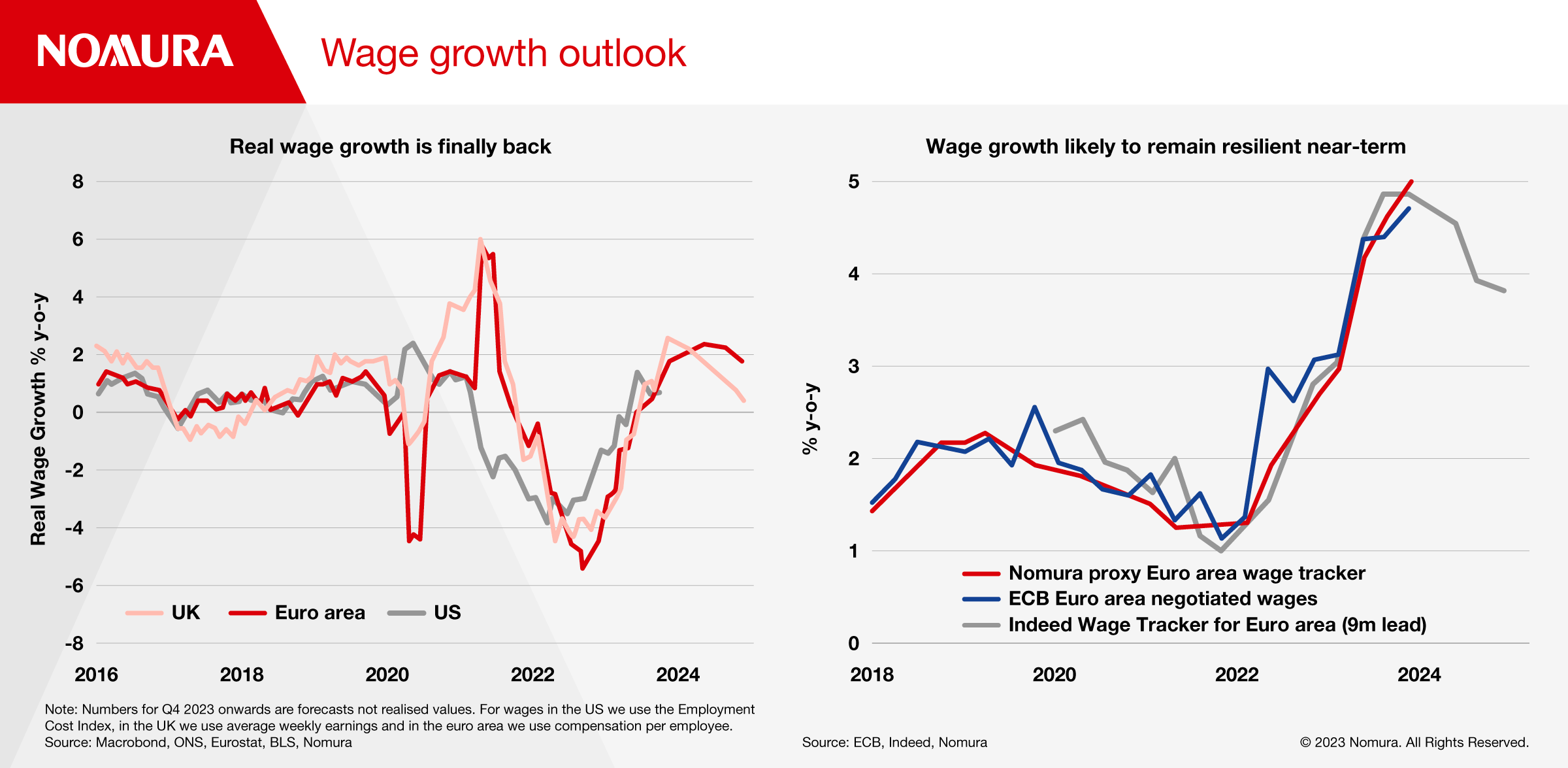

For the first time since 2021, the Euro Area should see positive real wage growth. According to our forecasts, it should peak at 2.4% y-o-y in Q2 2024, mostly due to falling inflation, with compensation per employee growth slowing only marginally. This should provide some support to embattled consumers that have been suffering from a cost-of-living squeeze.

Wage growth outlook

The Euro Area’s labour market continues to be resilient. As of October 2023, the unemployment rate remains at its historical low of 6.5%.

We expect the unemployment rate to rise, but only by 0.5pp from its current level, to 7.0% in Q4. This relatively benign rise stems from the structure of the Euro Area’s labour markets; by and large, they are quite inflexible due to the large-scale existence of job retention schemes. These job retention schemes mean that unemployment in the Euro Area is more inelastic to changes in activity or in response to economic downturns versus in the US or UK.

Inflation – Getting Back to Target

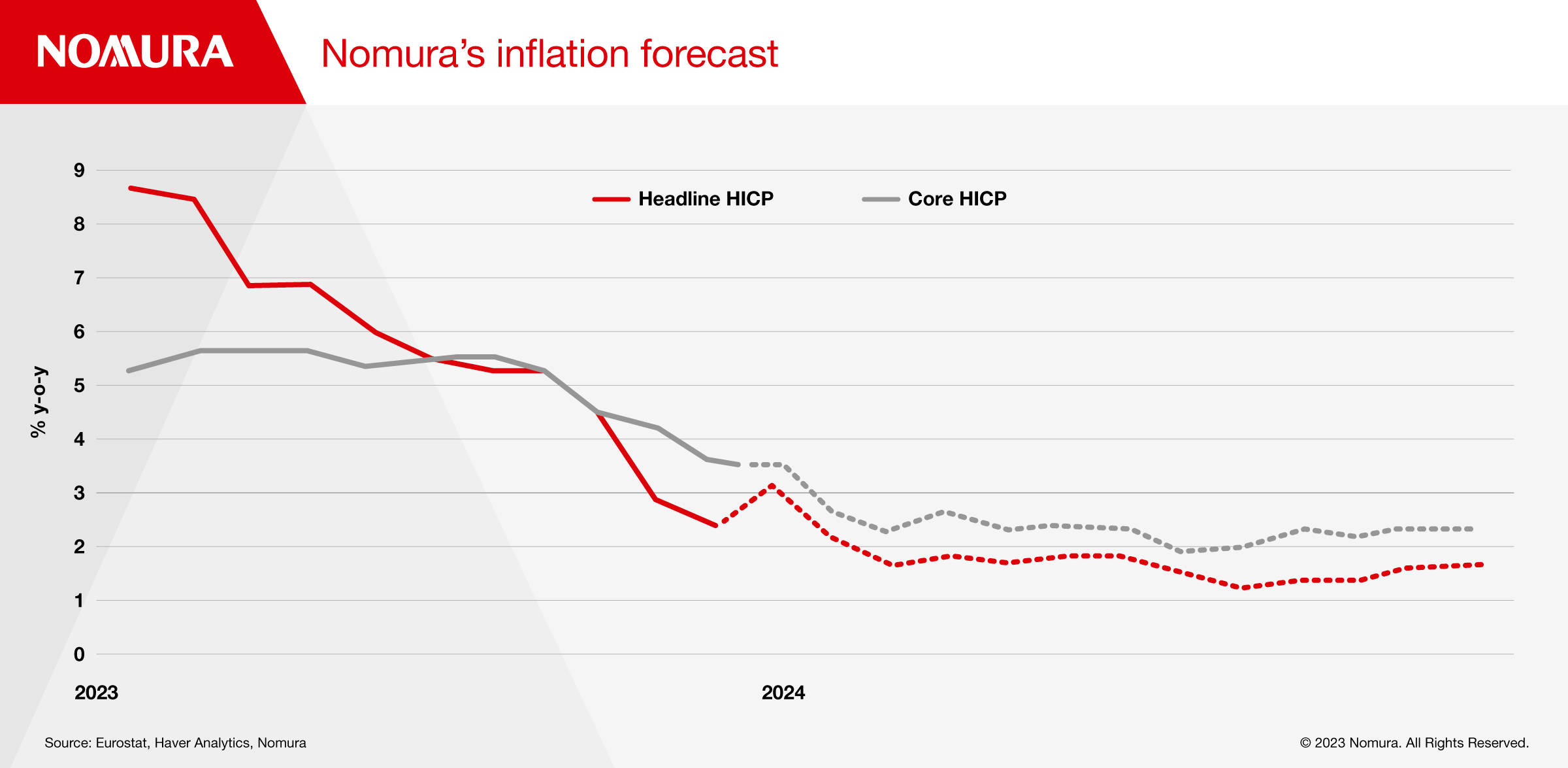

We expect Euro Area headline Harmonized Index of Consumer Prices (HICP) inflation to reach 2.1% by January 2024 and fall meaningfully over 2024, finally printing at 1.5% in December 2024. Meanwhile, we believe Euro Area core HICP inflation is set to continue its descent and reach 2.6% by January 2024, dip below 2% briefly during July and August, before rebounding and hovering around 2.3% until end-2024.

We expect core HICP inflation to continue to slow thereafter, albeit much more slowly, and reach the ECB’s 2% inflation target in a consistent manner by September 2025.

Nomura's inflation forecast

Monetary Policy – Shifting The Narrative From Hikes To Cuts

The ECB began raising rates at the most aggressive pace in its history in July 2022. Now, however, we think the ECB is done and dusted on rates as:

activity data are softening, indicating just a slowing or potential rolling sectoral recessions;

both headline and core inflation have fallen markedly since their respective peaks, and underlying momentum in core inflation, which is at present the ECB’s main focus, is slowing; and

guidance from the ECB suggests no more hikes are forthcoming and ultimately the Governing Council, on the whole, appears comfortable with rates at current levels.

Nomura's ECB view

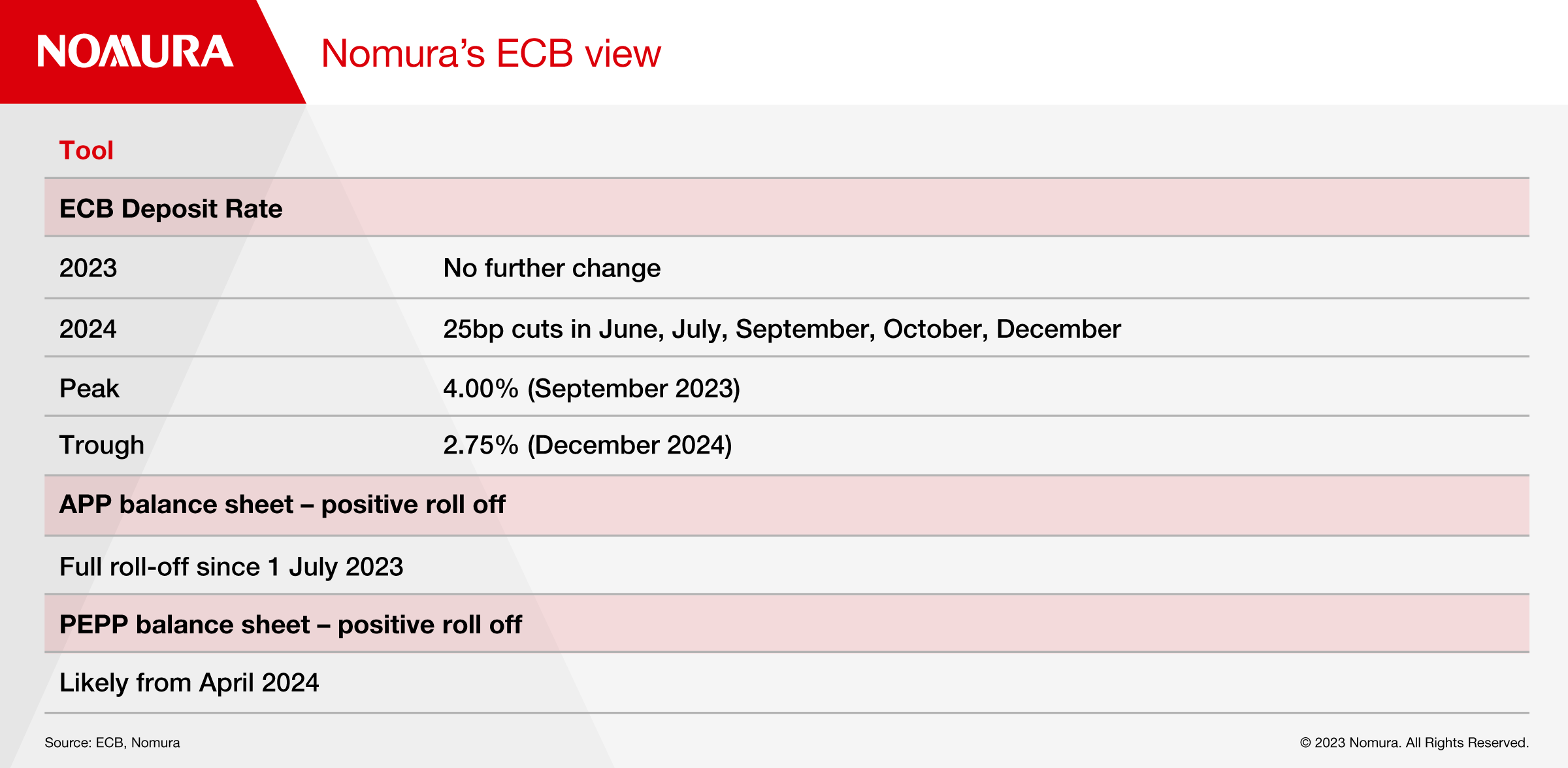

In our view, the ECB is likely to begin its cutting cycle only in June 2024. The rationale for cutting rates is that the ECB will eventually want to bring rates down from restrictive to neutral.

As a result, we see the ECB cutting by 25bp at each meeting from June 2024 until the depo rate reaches 2.75% (at that pace, it would get there by the end of 2024). We estimate that neutral by then will be in the range of 2.25 – 2.75%, and we believe the ECB will likely want to keep rates at the higher end of this range as structural factors may see inflationary pressures more pronounced versus pre-pandemic.

The risks to this view are likely skewed towards earlier cuts. Moreover, market pricing for cuts may even intensify in the near-term.

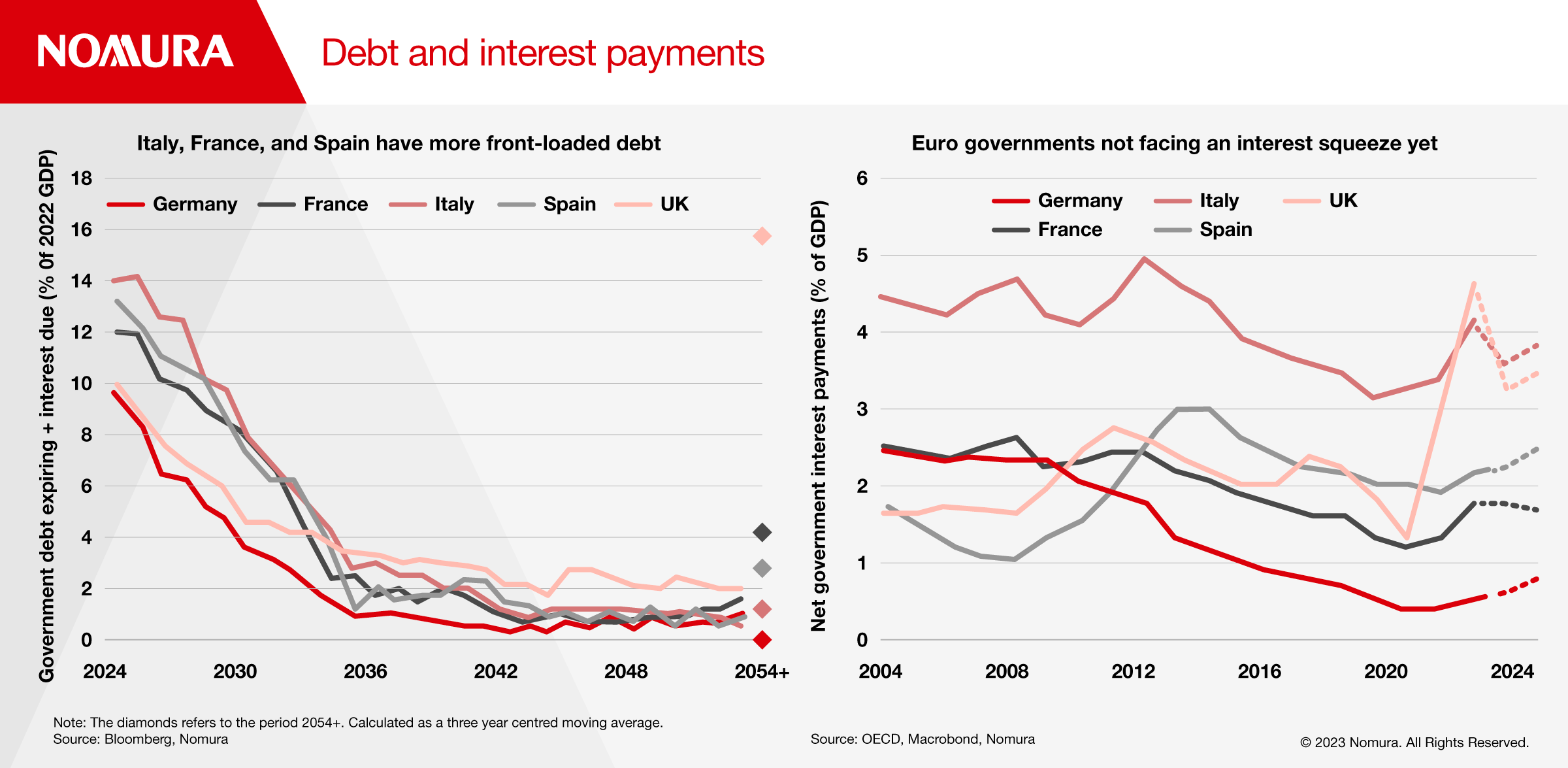

Fiscal Policy – Less Accommodative Than Before

The European Commission forecasts that most major Euro Area economies will shrink their fiscal deficits, although in general not enough to make much progress on the road to fiscal balance.

This will likely attract scrutiny from the European Commission, which is planning to re-implement fiscal rules. For certain countries, this will act as a constraint on their spending capabilities.

The European Commission has identified eight countries that are at risk of having excessive deficit procedures brought against them: Belgium, Spain, France, Italy, Latvia, Malta, Slovenia and Slovakia. New fiscal rules probably won’t affect the current draft 2024 budgets, but are likely to affect the planning for the 2025 budgets.

Regardless, generally there is increasing pressure from institutions like the ECB and national politicians to see more fiscal discipline.

Debt and interest payments

The 2024 European Parliamentary Election

To be held on 6 to 9 June, there are concerns about the lurch to the right and increasing popularity of right-wing eurosceptic political parties.

What are the implications of such a “lurch to the right”? Much of the legislation in the European Union, proposed by the European Commission, requires the active participation of the European Parliament. In essence, further integration could prove more challenging. This also likely makes the agreement and adoption of new EU fiscal rules, which have been suspended in response to the pandemic, more challenging.

United Kingdom

Stagnation and Sticky Inflation

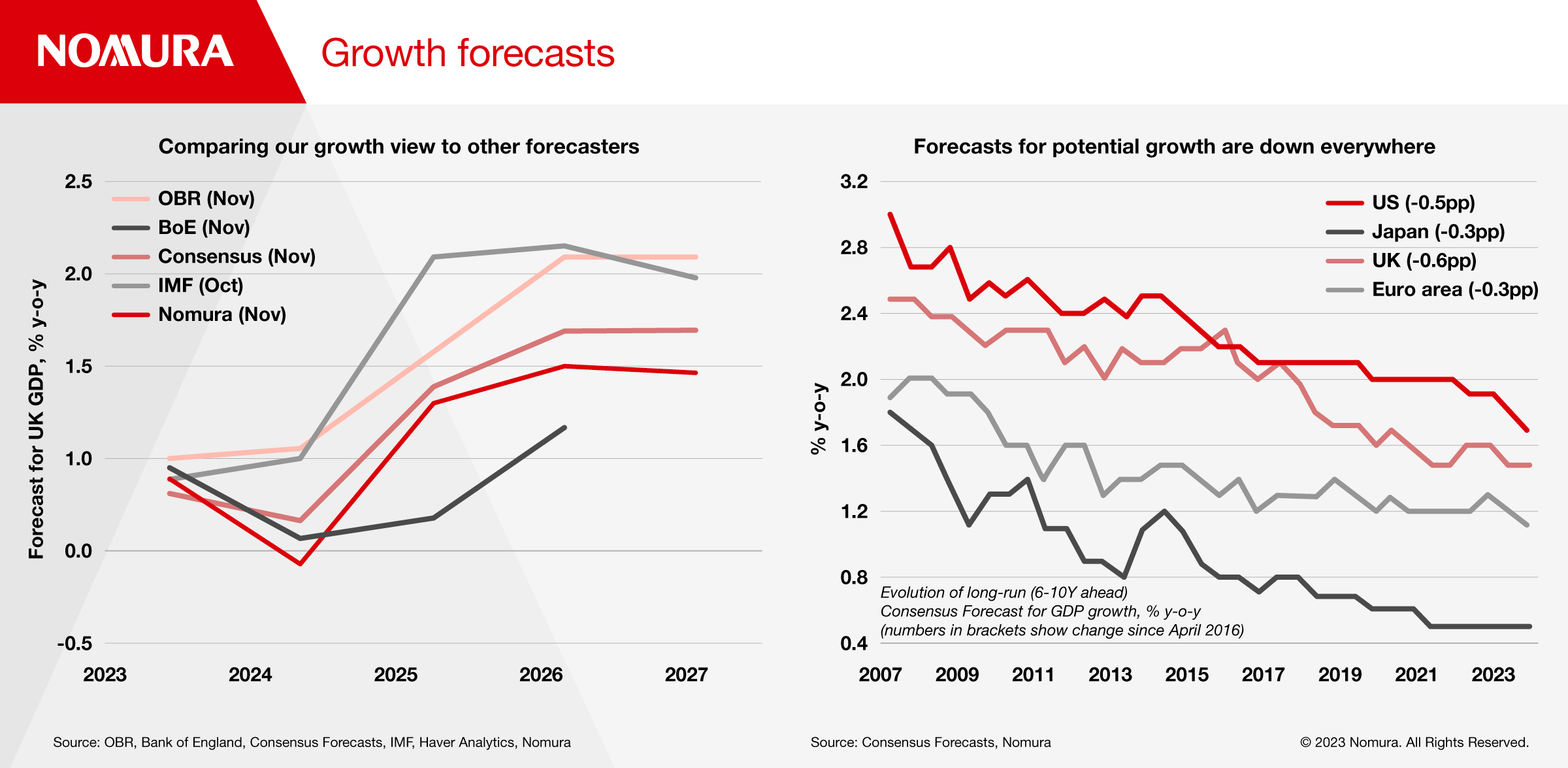

Economic growth has slowed but remains more resilient than we’d originally envisaged. With business surveys having generally held up, we forecast only a mild, and short, near-term recession, with risks in both directions.

UK growth forecasts

The news on UK inflation in recent months has been encouraging. The October CPI print revealed a notable decline in headline inflation, from 6.7% to 4.6%, lower than we, the consensus and the Bank of England were expecting.

However, we think it will take longer to get back to target than it took to reach its peak. Upstream services inflation in particular is proving more stubborn, according to recent survey evidence. And a tight – but easing – labour market should mean wage growth takes time to normalise.

The Monetary Policy Outlook

While markets are pricing in the possibility of earlier monetary policy loosening, especially from the ECB and the Fed, stickier UK inflation, alongside additional fiscal support ahead of the impending general election point to the BoE waiting for longer before cutting rates than the market expects about other central banks. In our view, it will be August 2024 before the first cut. We expect the Bank to cut rates back down to 4% by early 2025.

The UK General Election

The next general election must be held by January 2025, and is likely either in late spring or the autumn of 2024. It is unlikely to be earlier than the spring as the Conservatives will want any Budget loosening measures (typically announced in March) to have their desired effect, and probably no later than October as cold weather may lower turnout among older voters, who may be more likely to vote Conservative.

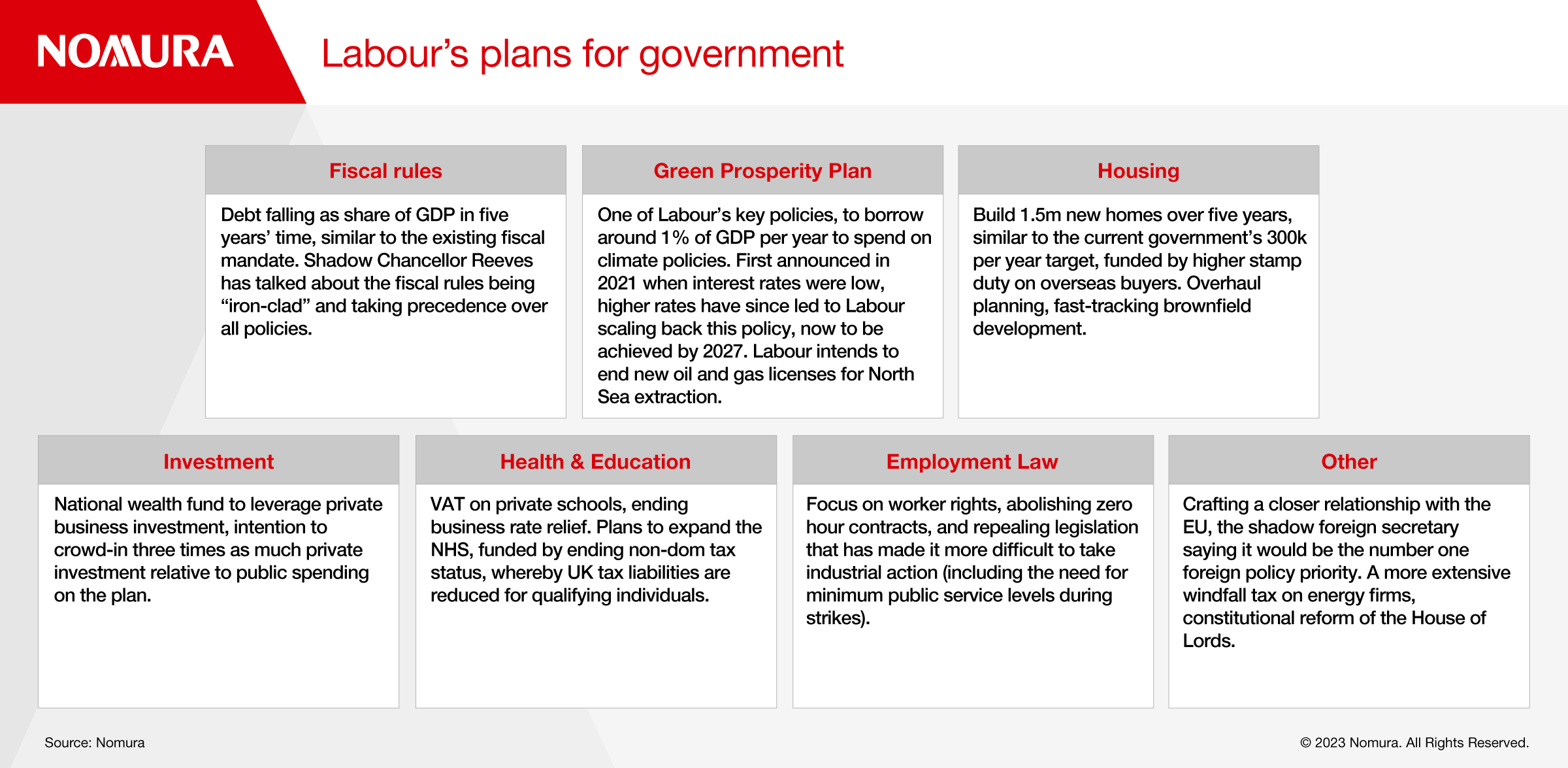

Should Labour win the election with a majority, and return to power after a 14-year period of Conservative rule, what is the party’s plan for government?

This content has been prepared by Nomura solely for information purposes, and is not an offer to buy or sell or provide (as the case may be) or a solicitation of an offer to buy or sell or enter into any agreement with respect to any security, product, service (including but not limited to investment advisory services) or investment. The opinions expressed in the content do not constitute investment advice and independent advice should be sought where appropriate.The content contains general information only and does not take into account the individual objectives, financial situation or needs of a person. All information, opinions and estimates expressed in the content are current as of the date of publication, are subject to change without notice, and may become outdated over time. To the extent that any materials or investment services on or referred to in the content are construed to be regulated activities under the local laws of any jurisdiction and are made available to persons resident in such jurisdiction, they shall only be made available through appropriately licenced Nomura entities in that jurisdiction or otherwise through Nomura entities that are exempt from applicable licensing and regulatory requirements in that jurisdiction. For more information please go to https://www.nomuraholdings.com/policy/terms.html.