The market for green structured notes continues to grow in depth and sophistication with new entrants and a broader variety of structures.

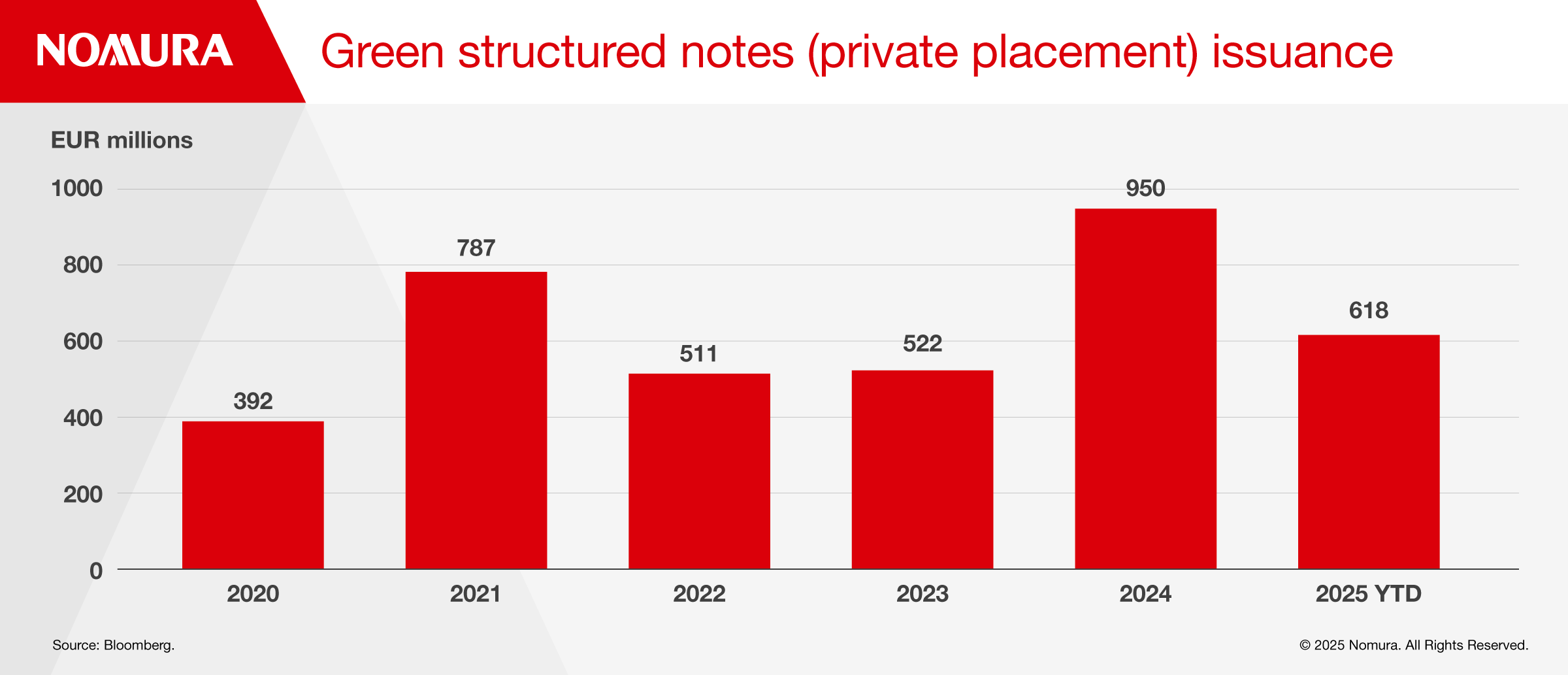

In 2024, green structured notes — defined as bespoke issuance with a green component* — saw record issuance of 950 million euros, almost doubling the amount from the previous year. This year, it is on track to hit a new high as issuance has already exceeded 600 million euros in the first six months, underscoring the growing demand for tailored offerings.

The first green bond was issued in 2007, but it was not until the 2010s before the inaugural green structured notes were issued. Since then, the market has seen more than a dozen banks offer various structures to a range of fixed income and equity investors looking for returns while fulfilling mandates to invest in green technologies.

Natalia Cermeno, Co-Head of Structuring EMEA at Nomura, says that the green structured note market saw a lull in 2022 and 2023 as fixed income rates were higher after global central banks lifted benchmark rates to fight inflation, driving down demand for yield enhancement. Additionally, markets were more volatile following Russia’s invasion of Ukraine, and this combined with unfavourable sentiment around ESG investing, which left some investors on the sidelines. However, the market has come back strongly since then.

“As investors have become accustomed to higher rates for longer, we have seen renewed demand for structured products to eke out more competitive returns, leading to a record year in 2024,” says Cermeno. “We could hit the one billion euro mark this year.”

Nomura issued its first green structured note at the end of April 2025 with a notional value of 20 million euros, and eight years’ maturity, sold to a Southern European bank to meet its asset and liability management (ALM) needs and its objective of financing green projects.

The note pays a fixed coupon for the first two years then a capped and floored floating coupon for the remainder. This approach enhanced the net interest margin over a two-year horizon while also providing long-term carry potential. The bespoke pay-off will channel investor proceeds into projects from Nomura’s Infrastructure and Project Finance business, which finances solar and other renewables ventures.

Nomura captured a so-called “greenium”, or green premium, where there is a cost saving by issuing a green bond instead of a conventional bond, reflecting the relative yield difference. This highlights strong investor demand.

“For investors, sourcing green structured notes can be a challenge, and that’s typically reflected in the pricing that the issuers can achieve. There’s more appetite for green assets than the market has projects to deploy,” says Cermeno.

The client was interested in a green investment but also needed a specific payoff to match its ALM profile, so Nomura used the building blocks of a derivative to match the exact maturity and coupons it required.

According to Cermeno, about a dozen banks have issued bespoke green structured notes. Many are not always active, so issuance typically depends on having capacity, being able to price the structure competitively, and having a green framework.

Issuing any type of green instrument requires governance to avoid misclassifying assets. To that end, Nomura published a Green Issuance Framework, defining projects eligible as green, based on international standards and validated by a second party opinion.

“We have been very careful to avoid greenwashing”, says Ella Chalfon, Sustainability Management Officer at Nomura. “We have a rigorous process of selecting and approving projects, and then later on calculating and reporting the impact created by them.”

Cermeno says that Nomura has capacity to increase issuance and sees appetite from French and Italian insurers for inflation-linked notes, equity-linked notes, and inverse floaters.

She also expects that the broader market will soon evolve to offer further depth of liquidity across a variety of payoffs in green format. This includes green loan repacks and green synthetic risk transfer deals, which are likely to become more attractive as rates remain higher for longer, prompting firms to focus on optimizing capital.

While there are ongoing challenges to ESG in the US, Cermeno says that European investors in particular are likely to support healthy issuance of green structured notes as they have seen how they can achieve “two goals with one product.”

For more information on this topic, please contact Natalia Cermeno or Ella Chalfon.

* “Bespoke issuance with a green component” reflects any green issuance below 200mn with a minimum denomination of 100k printed since 2021 and minimum issuance size of EUR 8mm. While there is a wide range of currencies issued, this analysis focuses on EUR and USD where the majority of green issuance has been issued. For the scope of this analysis, we have only considered bonds issued by the following global investment banks: HSBC, Citibank Group, Goldman Sachs, Morgan Stanley, JPMorgan, Bank of America – Merrill Lynch, NatWest Markets, Deutsche Bank, Barclays, BNP Paribas, Natixis, Credit Agricole, Standard Chartered Bank, and Nomura.

Disclaimer

This content has been prepared by Nomura solely for information purposes, and is not an offer to buy or sell or provide (as the case may be) or a solicitation of an offer to buy or sell or enter into any agreement with respect to any security, product, service (including but not limited to investment advisory services) or investment. The opinions expressed in the content do not constitute investment advice and independent advice should be sought where appropriate.The content contains general information only and does not take into account the individual objectives, financial situation or needs of a person. All information, opinions and estimates expressed in the content are current as of the date of publication, are subject to change without notice, and may become outdated over time. To the extent that any materials or investment services on or referred to in the content are construed to be regulated activities under the local laws of any jurisdiction and are made available to persons resident in such jurisdiction, they shall only be made available through appropriately licenced Nomura entities in that jurisdiction or otherwise through Nomura entities that are exempt from applicable licensing and regulatory requirements in that jurisdiction.

To read the full disclaimer, please click here.

For more information please go to https://www.nomuraholdings.com/policy/terms.html