Electric vehicle adoption is outpacing charging infrastructure build-out creating a sub-optimal experience for both customers and fleets. But massive ongoing investment in the sector combined with rapidly evolving technologies, promises to accelerate the required infrastructure to support continued growth, according to an EV expert at Nomura Greentech’s Sustainable Leaders Summit.

Sales of electric vehicles in the U.S reached 5.7% in 2022 and are expected to grow to 66mn in 2040 to exceed 50% market share, according to Clean Technica data, yet a typical person in the U.S. lives about 31 minutes away from a high speed charger.

While the charging infrastructure requires more investment, as - it is very far from the internal combustion engine equivalent where you’re 7 minutes away from a gas station, there is no alignment to provide a compelling user experience the expert said at the summit, held under the Chatham House Rule.

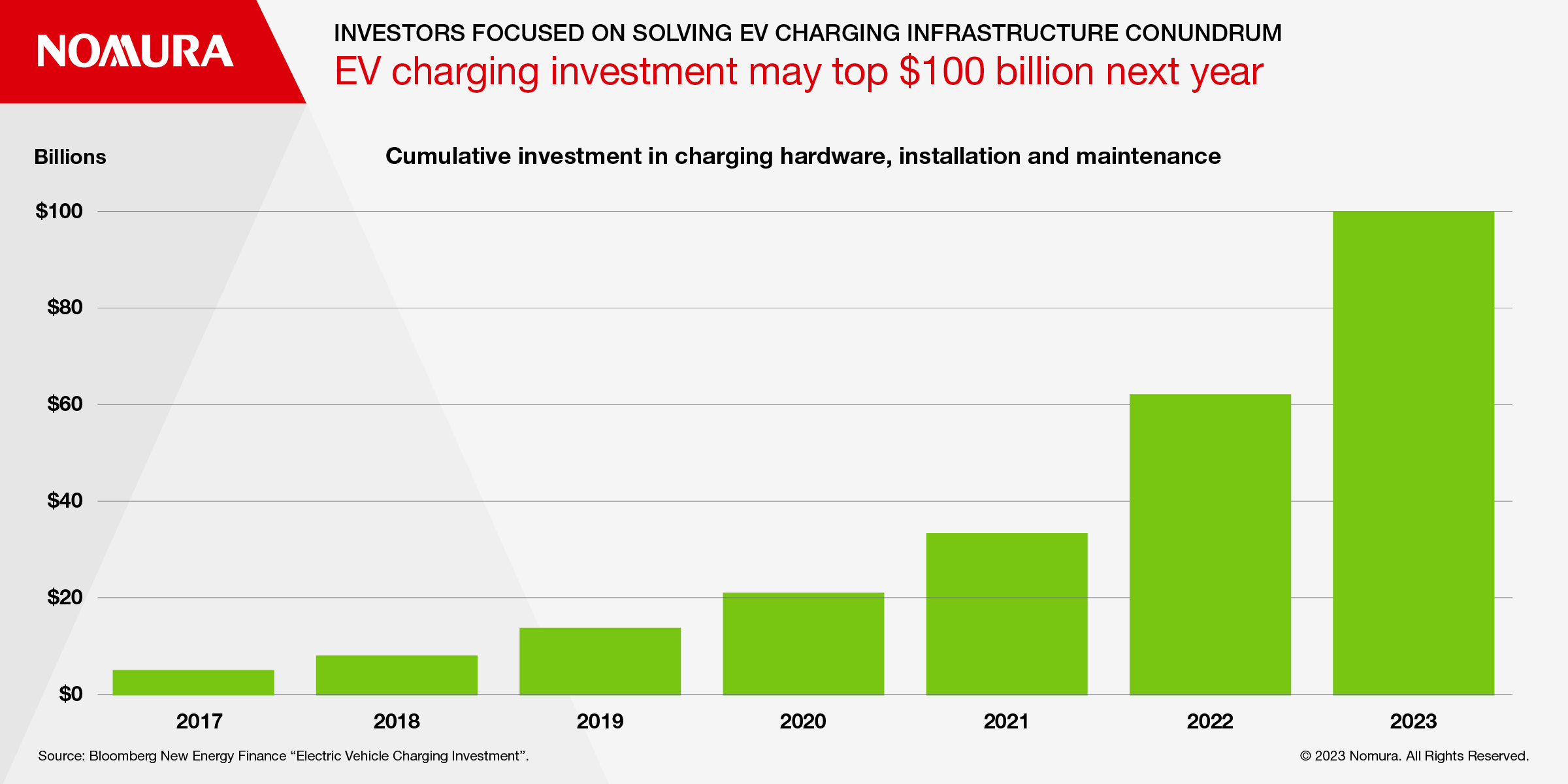

But capital is pouring into the sector and in 2022 alone, $28.6bn was invested in charging, up 228% from the prior year, 61% of which is attributed to the more than 600,000 public chargers built in China. Cumulative investment globally will probably surpass the $100bn mark in 2023 if China keeps up its relentless pace, according to Bloomberg New Energy Finance data.

Fueled by strong EV adoption, increased network utilization and a deeper understanding of the monopolistic nature of the industry, a large number of infrastructure investors, oil majors, utilities, charging companies, and incumbents are committing to install millions of chargers, according to the expert.

Unit economics should start to improve as factories scale, such as Wallbox’s plant in Texas, which will have the ability to produce 1mn chargers annually by 2030.

The current patchwork of charging connectors and networks in the U.S. makes for a poor consumer experience compared to gas stations, a prime example being the lack of standardized connectors but the announcement from GM and Ford to use Tesla’s ‘North American Charging Standard’ should offset some of those frictions.

In the U.S., fast charger companies claim that they have over 95% uptime; however, studies show that the number is closer to 77%. Tesla’s supercharger network is an exception providing fast charging with 99.95% uptime reliability.

It is not just a lack of infrastructure but also the fact that large investments are not in line with consumers’ expectations. Fast deployment of capital as in the case of Electrify America can lead to bad outcomes with many of the stations deployed in suboptimal locations.

While battery technology continues to improve significantly, it still has limitations. Batteries are heavy and take up a lot of space, which can limit the design and functionality of EVs, and they also have limited lifespans with their performance affected by temperature and other factors, the expert said.

BATTERY SWAPPING

An alternative option that has gained traction in China involves running dedicated stations that can automatically swap out depleted battery packs for fully charged ones in minutes, which brings the refueling experience on par with ICE models, according to the expert.

This could help enable longer trips without long charging stops but U.S. and European car companies are less open to the swap system as it moves them towards an asset-heavy business model without the freedom to use the battery as an integral part of the vehicle.

In China, NIO and Geely are betting heavily on these solutions for both personal vehicles and commercial fleets, leveraging the government to front the high cost; the companies expect to operate 5,000 swap stations by 2025.

However, swappable battery packs require standardization across vehicles, which presents obstacles in such a fragmented field.

GRID IMPACTS

As EVs scale up, managing when they charge will be critical to avoid overloading the grid especially considering the challenges of renewable energy intermittency.

An executive involved in the battery space noted that there will be more energy capacity in EVs by 2030 than the entire electricity grid, which provides a good opportunity for EVs to help make the grid more resilient.

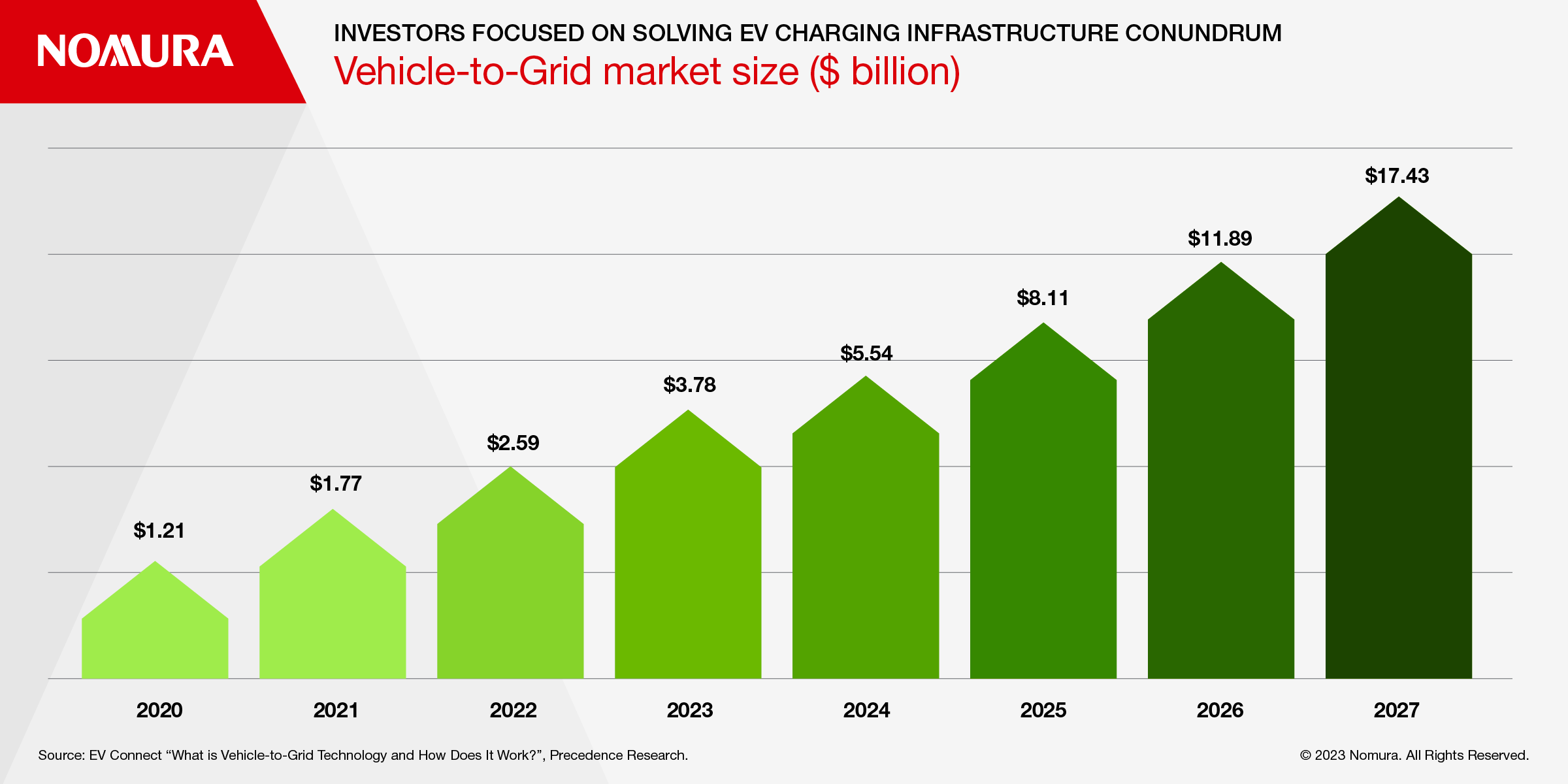

Bidirectional charging is one solution, which allows EVs to provide power back to the grid and vice versa at optimized times of the day but it faces policy and technical barriers. While utilities are starting to manage EV charging to help the grid, wide scale vehicle-to-grid flow is further away.

However, regulation will play a critical role in adoption of a full lifecycle system of utilizing batteries from EVs to support the grid, noted another executive.

The EV expert went further, saying that rather than incentivizing overnight charging at home, creative solutions like vehicle-to-everything (V2X) will be needed to coordinate smart charging of vehicles wherever renewable supply is abundant in order to procure the greatest efficiencies. Nearer opportunities are fleets providing grid services through centralized storage and managed charging.

The future could see self-driving EVs tapping renewables when available and providing power back to buildings or the grid when useful.