General Partners (GPs) of private equity funds are increasingly adopting net asset value (NAV) financing as a dedicated strategy from the outset of a fund’s life amid ongoing challenging market conditions for exits and new capital raises.

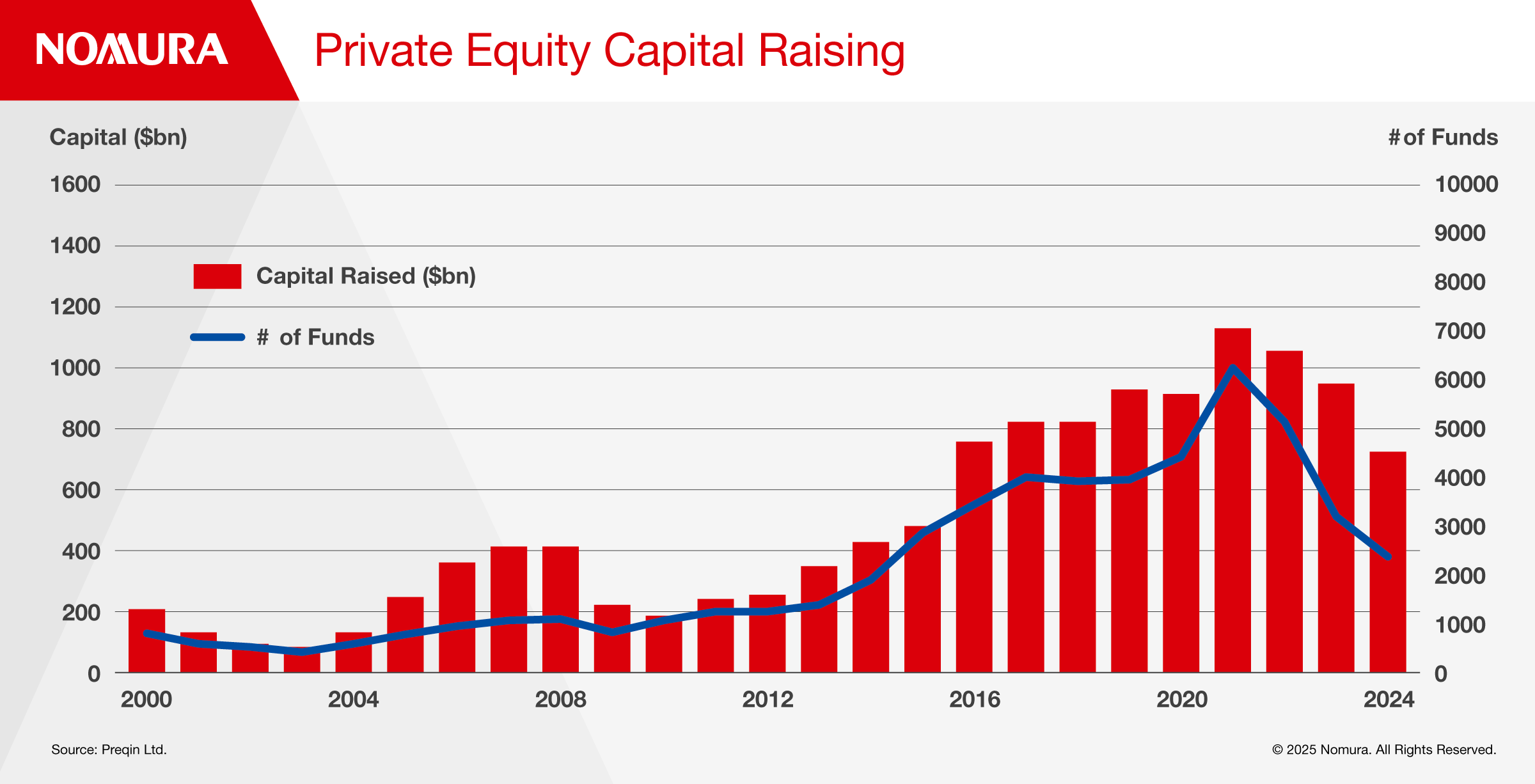

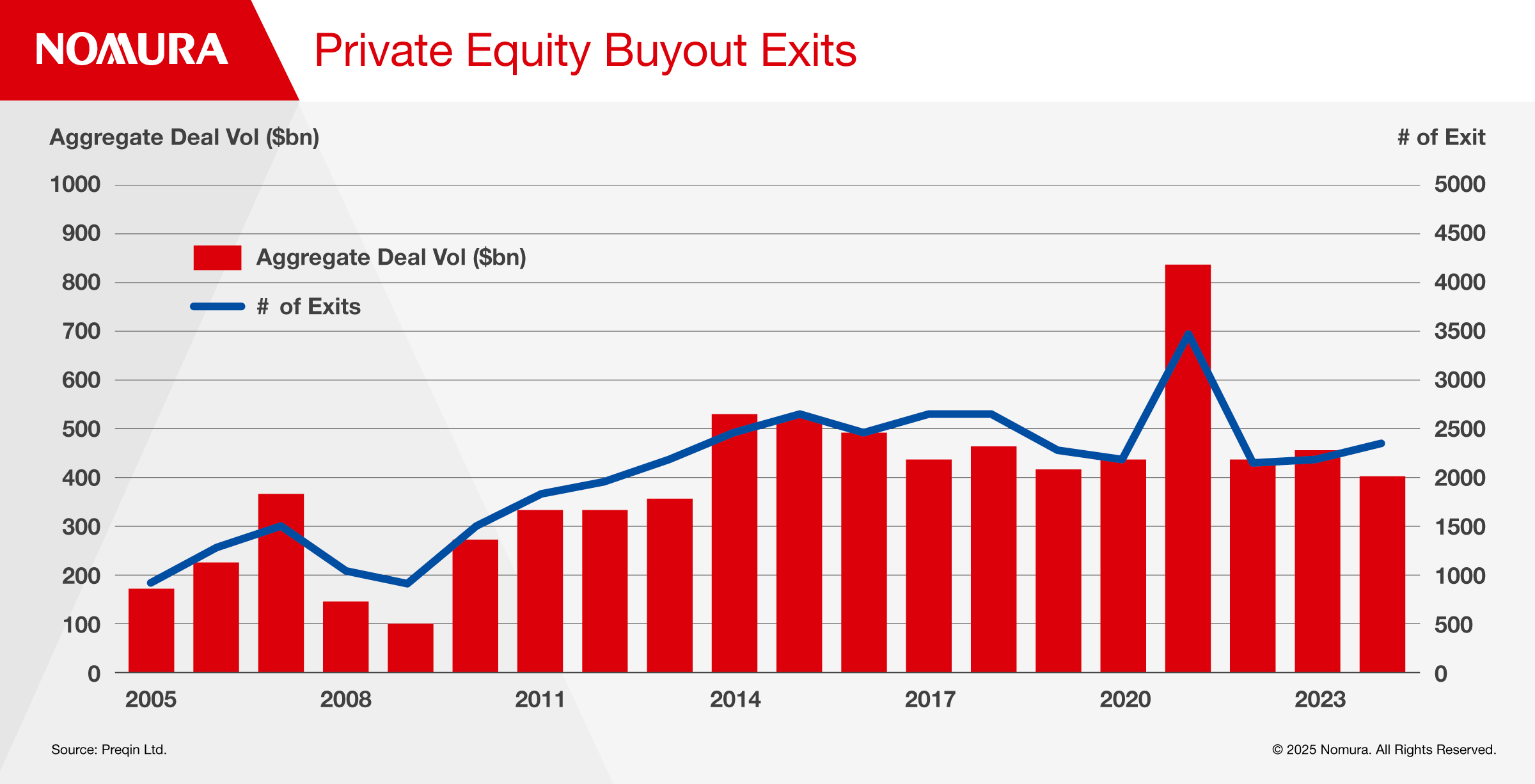

The NAV financing market grew to $44bn in 2023 and is predicted to reach $145bn by 2030, according to Oaktree Capital Management while buyout portfolios currently hold 28,000 unsold companies with an estimated value of $3.2 trillion, according to Bain’s global private equity report.

NAV financing allows funds to tap into the value of their existing holdings, unlocking capital for strategic investments and portfolio management initiatives without having to sell these holdings prematurely. NAV financing is a loan provided by a lender to a private equity fund that owns a diversified portfolio of companies. This loan is secured by the net asset value of the fund’s holdings and the fund’s NAV acts as collateral or security for the loan.

Nomura has a long track record of providing NAV based financing and liquidity solutions to private equity investors having operated in the space for more than a decade and continues to deploy capital to meet client needs.

Slower recycling of cash, higher interest rates and market volatility are key drivers behind a rise in primary NAV financing, says Max Forton, Head of Americas Fund Financing Solutions at Nomura. He adds that the difficult fundraising environment has made NAV financing an attractive proposition as sponsors have 15% to 25% target internal rates of return (IRRs) and the cost of NAV debt is comfortably lower than those figures.

“Taking on leverage if you are planning to hit those returns should naturally be accretive,” he says. “It’s an active way for sponsors to bet on themselves in a challenging fund-raising environment.”

Gaurav Khare Head of EMEA Fund Financing Solutions at Nomura says that in a competitive environment for primary sponsors looking to raise capital, using leverage via NAV financing allows them to offer higher returns to investors, which in turn allows them to raise more capital.

He says that a more difficult market for exits means that portfolio companies are being held for longer and may therefore require more investment to grow but their access to capital over a longer period becomes reduced as Limited Partner (LP) investors have offered a fixed amount of capital to these sponsors at the fund’s inception.

“These companies are in growth mode and so NAV facilities can be an interesting way to raise additional capital to keep these companies growing, injecting additional funds or acquiring related targets.”

Khare notes that the other form of cheaper capital accessible to primary sponsors is capital call facilities, which tend to be available during the initial investment period of a fund. NAV financing offers loans at a cost that’s closer to capital call facilities but not as expensive as LP capital and it allows GPs to deploy it more flexibly beyond just the initial investment period of the fund as with capital call facilities.

The technology is clearly here to stay but sponsors should also be aware of the costs including signing up to covenants and restrictions. Most bank NAV lending facilities require security over assets. Loan to value (LTV) covenants typically require borrowers to divert cash towards lenders or conduct an accelerated sale of assets in certain scenarios.

He says that if the macro and tariffs backdrop in the US makes exits more difficult, then NAV financing will rise up the agenda for sponsors as it offers versatility over a longer time horizon. But sponsors evaluating NAV facilities will need to have confidence that their assets are holding value when taking on leverage so they will need to trade off LTVs with diversification and cyclicality in their portfolios.

Forton says he is paying closer attention to the ‘value’ part of the LTV calculation as the nature of private markets means an inevitable delay in valuation and reporting making it even more important to understand where the actual value lies. He gives the example of a 10% LTV loan against a 31 December record date NAV which may have shifted significantly when it comes to underwriting the asset several months later and taking a view of the collateral.

Khare says that as the market has matured, NAV financing has bifurcated into bank lenders that typically focus on the lower LTV structures, and private credit funds that service the higher LTV deals. Lower LTV structures in the range of 10-20% are most common as they add a lower risk IRR pickup.

He also sees banks with big balance sheet that specialise in subline lending becoming more active in NAV financing which has led to spread compression but he says it’s in line with comparable markets for a similar risk profile.

He adds that it’s become a very competitive space because of the dearth of opportunity as an originator of private credit over the past three years. Leveraged Finance had a record year in 2024 exceeding $1trillion globally but the majority was refinancing as opposed to new transactions. As a consequence, NAV deals have been subject to spread compression but in general, they are in line with comparable public markets for a similar risk profile.

While NAV financing isn’t a nascent market it still has scope to develop further, and Forton expects to see a continued period of muted liquidity within private markets driving growth of the sector.

“So many assets held by private equity sponsors have exit ramps that are getting pushed further down the road due to macro volatility which should present a lot of opportunity for this space,” he says.

Over the longer term, he expects the market to become more sophisticated and well-defined with capital being better matched to the risk of the assets rather than the patchwork of deals that characterise today’s market.

“Currently, it’s a bit of an egg hunt where if you find the egg you just take it regardless of your capital profile versus their capital needs but as the market develops and more lenders can show track records, and as coverage improves, assets will find a more optimized home.”

Khare adds that in terms of innovation, a new wave of money coming into the private markets space from retail funds, will bring different leverage structures into play which means the NAV financing technology can be deployed to different sources of capital.