Japan: Side effects of support measures for corporations

Companies overcoming cash flow issues caused by the pandemic may have to curb capex due to rising debt

- Japanese government and BOJ’s various financial support measures during the pandemic have shown some success

- However, increased borrowings could potentially result in reined in capex and other investment, particularly affecting SMEs

- We envision government policy measures to come into play if the way liabilities are holding back capex starts to become recognized issue

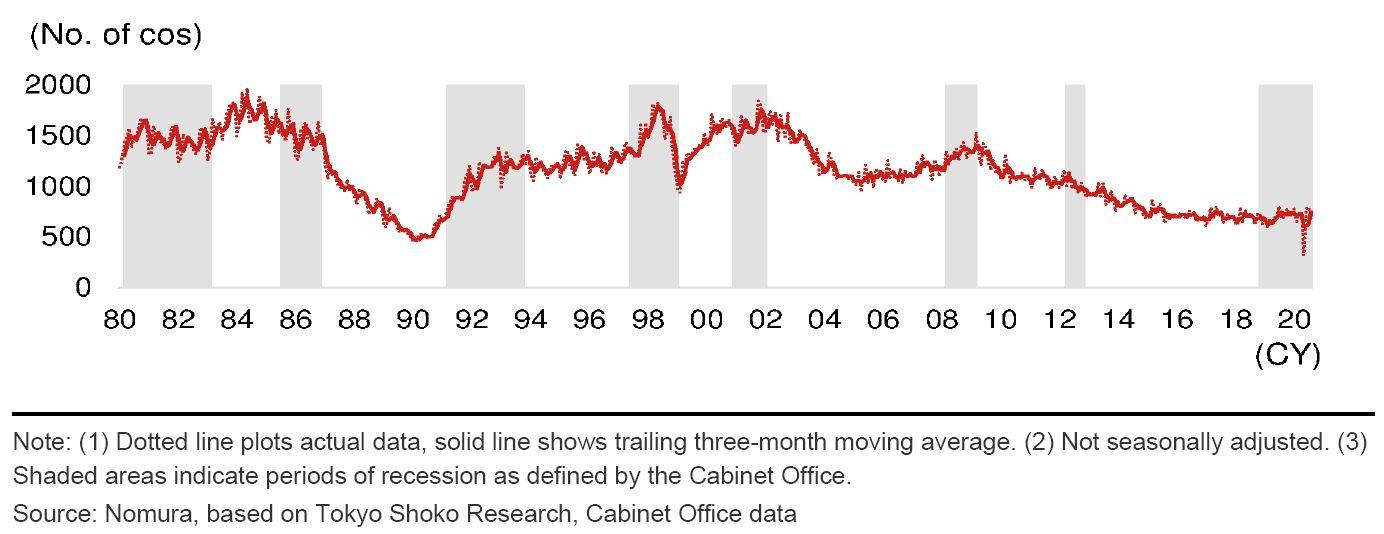

Cash flow support for corporations of unprecedented scale during pandemic

The Japanese government and BOJ have drawn up various financial support measures for corporations in response to the sharp downturn in the economy due to the COVID-19 pandemic. Companies have also been able to access essentially interest-free loans and there has been a resultant sharp increase in lending by financial institutions since May. While corporate sentiment has deteriorated sharply, companies have largely avoided a serious cash crunch and corporate bankruptcies remain low. We think these wide-ranging support measures during the pandemic have had some success.

Potential side effects from unprecedented support package

We expect measures to help companies with cash flow to continue for now and think we need to watch out for potential side effects. If the economic recovery proves sluggish, companies saddled with large amounts of debts will need to allocate their operating surplus to repayments, which could see them rein in capital expenditures (capex) and other investment.

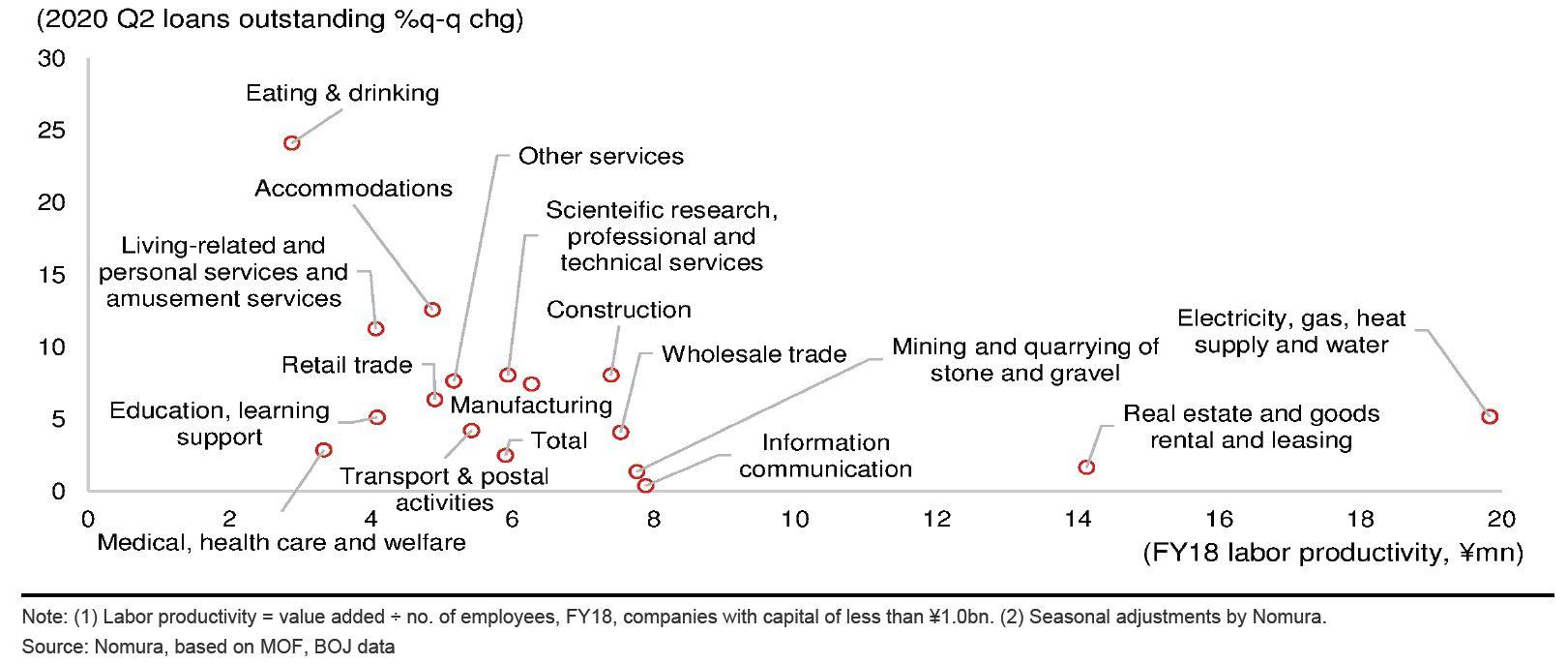

We estimated capex function with the debt-to-total assets ratio, expected growth rate, and real interest rate as explanatory variables, indicating that the more the debt-to-total assets ratio increases for small and medium-sized enterprises (SMEs), the more they have to rein in capex compared to large corporations.

Productivity improvement efforts may be hindered at SMEs and face-to-face service businesses

We also consider the impact on productivity. Observers have for a long time identified a need to improve productivity at SMEs, but after going through the pandemic SMEs may think twice about carrying out the investment needed to improve productivity, in our view. We can moreover see that, companies in face-to-face industries sharply increased their borrowing just to get through the pandemic. As a result we think they may continue to rein in capex.

How to resolve the debt problem and improve productivity after the pandemic

Given that the increase in debt is prompting companies to rein in capex and hampering efforts to improve productivity, it is, as BOJ Governor Haruhiko Kuroda indicated, likely to be some time before financial support measures for companies are scaled back. Scaling back the support measures too quickly could cause the economy to stumble, resulting in a prolonged downturn.

If the way corporate debt is stifling capex becomes a recognized problem, we can envision the following kinds of policy measures coming into play: (1) bolstering companies' cash flow while making repayment terms easier; (2) maintaining low or zero interest rate policy for a protracted period and adopting a gradual repayment regime as the economy returns to normal; (3) using tax breaks to bolster capex; (4) using public funds to reduce corporate debt; and (5) encouraging corporate consolidation.

Read our full report here.

Contributor

Kengo Tanahashi

Economist, Japan

Masaki Kuwahara

Senior Economist, Japan

Takashi Miwa

Chief Japan Economist

Disclaimer

This content has been prepared by Nomura solely for information purposes, and is not an offer to buy or sell or provide (as the case may be) or a solicitation of an offer to buy or sell or enter into any agreement with respect to any security, product, service (including but not limited to investment advisory services) or investment. The opinions expressed in the content do not constitute investment advice and independent advice should be sought where appropriate.The content contains general information only and does not take into account the individual objectives, financial situation or needs of a person. All information, opinions and estimates expressed in the content are current as of the date of publication, are subject to change without notice, and may become outdated over time. To the extent that any materials or investment services on or referred to in the content are construed to be regulated activities under the local laws of any jurisdiction and are made available to persons resident in such jurisdiction, they shall only be made available through appropriately licenced Nomura entities in that jurisdiction or otherwise through Nomura entities that are exempt from applicable licensing and regulatory requirements in that jurisdiction. For more information please go to https://www.nomuraholdings.com/policy/terms.html.