Japan in focus | 3 min read May 2025

Japan in focus | 3 min read | October 2025

The Takaichi Surprise

How the woman chosen to lead Japan’s incumbent political party could affect markets and the economy.

Japan in focus | 3 min read | October 2025

How the woman chosen to lead Japan’s incumbent political party could affect markets and the economy.

On Saturday, October 4, Sanae Takaichi, the former economic security minister, was elected leader of Japan’s Liberal Democratic Party (LDP). It surprised many who had expected the Minister of Agriculture, Shinjiro Koizumi, to be voted in.

Takaichi is likely to be nominated as the new prime minister — and become Japan’s first female prime minister — at an extraordinary Diet session, possibly on October 17. She is then expected to take part in a number of important diplomatic events, starting at the end of the month with the ASEAN leaders’ summit in Malaysia, then host US President Donald Trump in Tokyo for a Japan–US summit.

Takaichi’s economic policies — already being referred to as Sanaenomics, and which resemble the Abenomics of former Prime Minister Shinzo Abe — have the following three pillars:

National crisis management and economic growth: Takaichi says she will try to strengthen and enrich Japan through investment for the purpose of national crisis management and economic growth

Expansionary fiscal policy: This includes increases in tax revenues and better use of existing funds within the government as financial sources while trying to avoid increases in Japanese government bond (JGB) issuance. Takaichi attaches importance to measures to combat inflation, including an increase in subsidies for local governments, an increase in deductible individual income, the abolition of temporary taxes on gasoline and light oil, and the introduction of refundable tax credits, which could give a boost to consumer spending among middle- and lower-income consumers.

The government should be responsible for monetary policy while the BOJ has autonomy to choose the best policy tools: Takaichi has explicitly said that the government should be responsible for monetary policy. She believes that cost–push inflation is not enough to confirm that Japan is getting out of deflation. She would like demand–pull inflation to be the major driver of inflation and that the BOJ should help make this happen.

While Abenomics prioritized monetary easing, Sanaenomics seems more focused on expansionary fiscal policy.

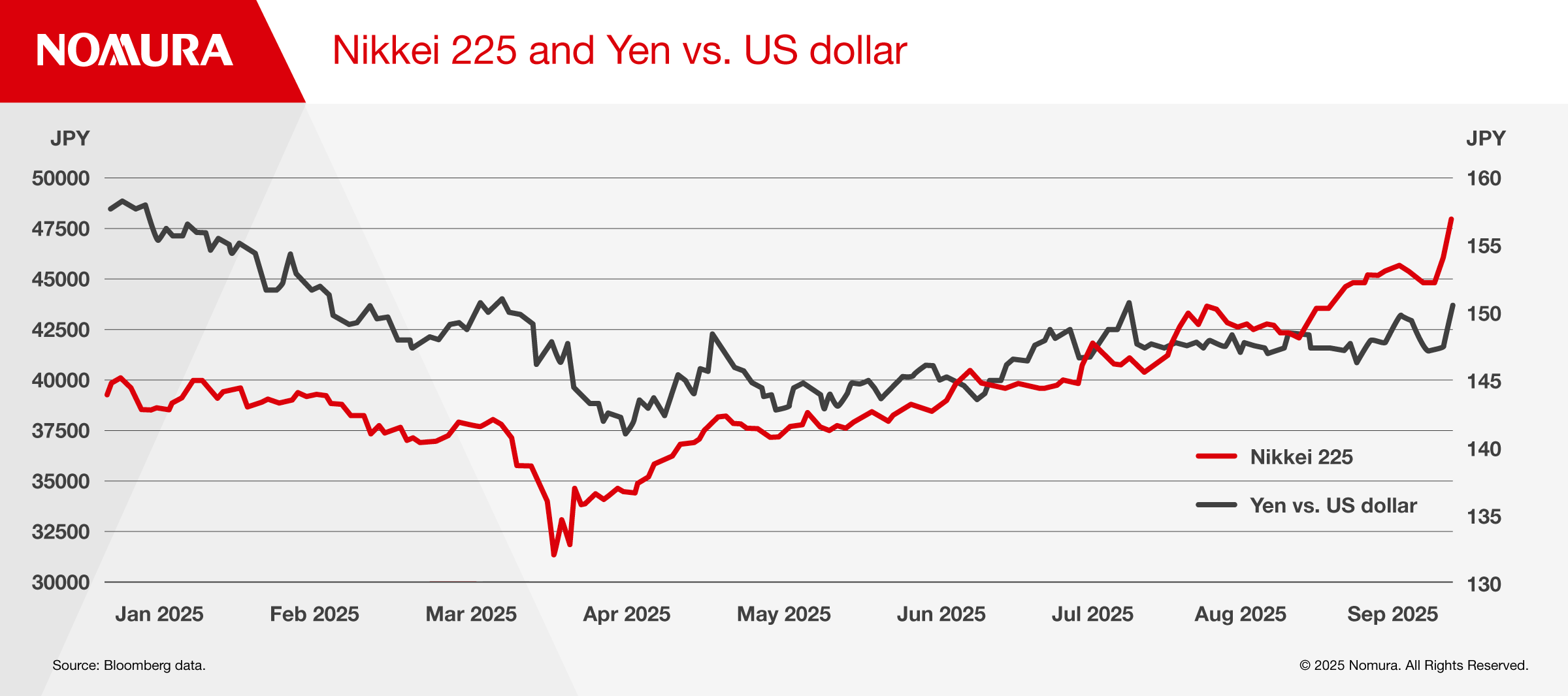

When the markets opened on Monday, October 6, they reacted much as one might have expected to the “Takaichi surprise.” The Nikkei 225 posted a large gain, briefly topping 48,000, and the yen weakened against the dollar to the 150 handle (Figure 1).

Fiscal policy worries caused the yen yield curve to steepen. Although short-term JGB yields fell on expectations that the BOJ would maintain a loose monetary policy, super long yields rose: the 20 year yield climbed to around 2.7% and the 30 year yield to nearly 3.3%. Expectations for a BOJ rate hike in October receded sharply, with the implied probability falling from over 60% before the election to less than 30%.

However, further yen depreciation would feed inflationary pressure, so the BOJ — as the guardian of price stability — will likely need to act, and Takaichi has not ruled out rate hikes. Markets will presumably look for a new equilibrium while assessing how Takaichi handles policy.

After the initial stock market rally, the market will most likely begin to scrutinize the feasibility of Takaichi’s policies, as well as her Cabinet picks, coalition negotiations, and growth strategy. We think expectations for new policies following the regime change could prompt a longer market rally and sustained buying by nonresident investors. This was seen with the post office reforms after the September 2005 general election and with the launch of Abenomics after the December 2012 election.

In contrast, the share price rally could quickly lose steam if Takaichi’s policies prompt a sharp rise in interest rates or start to sound similar to those of previous administrations. The TOPIX rallied for a week following the surprise victory of Junichiro Koizumi in April 2001, but the gains were eroded when his Cabinet picks were not well received.

The Hudson Institute posted an essay by Takaichi on its website on 1 October, in which she provided a list of areas where growth is expected, including AI, semiconductors, quantum, nuclear fusion, perovskite, materials, biotechnology, aerospace, shipbuilding, drug discovery, disaster prevention, and defense. This broadly overlaps with areas of strength for Japan that she talked about when running for the LDP leadership in 2021.

Economic security

Takaichi has spoken a great deal about economic security, which we think covers areas such as pharmaceuticals, semiconductors, cybersecurity, AI, cloud computing, defense, bunkers, and space. She has long been in favor of boosting cybersecurity, having served as the first chair of the LDP’s Cybersecurity Strategy Headquarters and having worked to get the Active Cyber Defense Act passed in May 2025.

She has also associated herself with AI for some time, speaking about it in 2016 when she was minister for internal affairs and communications. During the 2025 LDP leadership race, she launched an AI version of herself: AI Sanae.

On the defense front, she has shown support for exceeding the government’s target of defense spending at 2% of GDP in FY2027, partly related to purchases of cutting-edge equipment. She has also spoken about enacting legislation to require the installation of bunkers at major train stations and when constructing large buildings.

Energy

With regard to energy, Takaichi has spoken about restarting nuclear reactors in the near term while also ensuring that Japan retains its technological lead over other countries over the longer term by stepping up R&D into next-generation small modular reactors (SMRs) and nuclear fusion. She has also posted many videos about nuclear fusion and SMRs.

Moreover, she has voiced strong opposition to solar panels made overseas and is keen to promote the development and uptake of perovskite solar panels as a Japanese invention. During the 2025 leadership race, she also advocated for resource development in Japan and joint international resource development.

Given Takaichi’s macroeconomic views, there are rising expectations that nominal economic growth will keep higher than nominal interest rates. This is fundamentally a positive for equity markets.

While Takaichi is advocating a wide range of policies, the real question is how likely they are to be implemented. So, we should pay close attention to appointments within the LDP — in terms of policy, the policy research council chair, and in terms of the tax system, the chairperson of the Tax Commission. Next, attention should also be given to the appointment of the ministers and heads of the various economic agencies.

Many economic policies of Sanaenomics appear likely to work in the direction of accelerating inflation. At the same time, we expect core CPI inflation in Japan to fall through the first half of 2026. We think this disinflationary trend is likely to increase the feasibility of many of Takaichi’s policies.

Chief Economist, Japan

Head of FX Strategy, Japan

FX Strategist, Economist

Executive Rates Strategist, Japan

Chief Equity Strategist, Japan

Equity Strategist, Japan

Chief Market Economist, Japan

This content has been prepared by Nomura solely for information purposes, and is not an offer to buy or sell or provide (as the case may be) or a solicitation of an offer to buy or sell or enter into any agreement with respect to any security, product, service (including but not limited to investment advisory services) or investment. The opinions expressed in the content do not constitute investment advice and independent advice should be sought where appropriate.The content contains general information only and does not take into account the individual objectives, financial situation or needs of a person. All information, opinions and estimates expressed in the content are current as of the date of publication, are subject to change without notice, and may become outdated over time. To the extent that any materials or investment services on or referred to in the content are construed to be regulated activities under the local laws of any jurisdiction and are made available to persons resident in such jurisdiction, they shall only be made available through appropriately licenced Nomura entities in that jurisdiction or otherwise through Nomura entities that are exempt from applicable licensing and regulatory requirements in that jurisdiction. For more information please go to https://www.nomuraholdings.com/policy/terms.html.

Japan in focus | 3 min read May 2025

Japan in focus | 4 min read July 2023

Japan in focus | 3 min read July 2025