The UK is a stalwart of green bond issuance and has been at the forefront of climate measures. It broke new ground when it launched the world’s first green government bond for retail investors, dubbed Green Savings Bonds and other countries are already rolling out similar programmes to support and grow the market.

While governments around the world have long issued green bonds as part of their efforts to finance projects aimed at environmental improvement, expanding the programme to retail investors is a novel move.

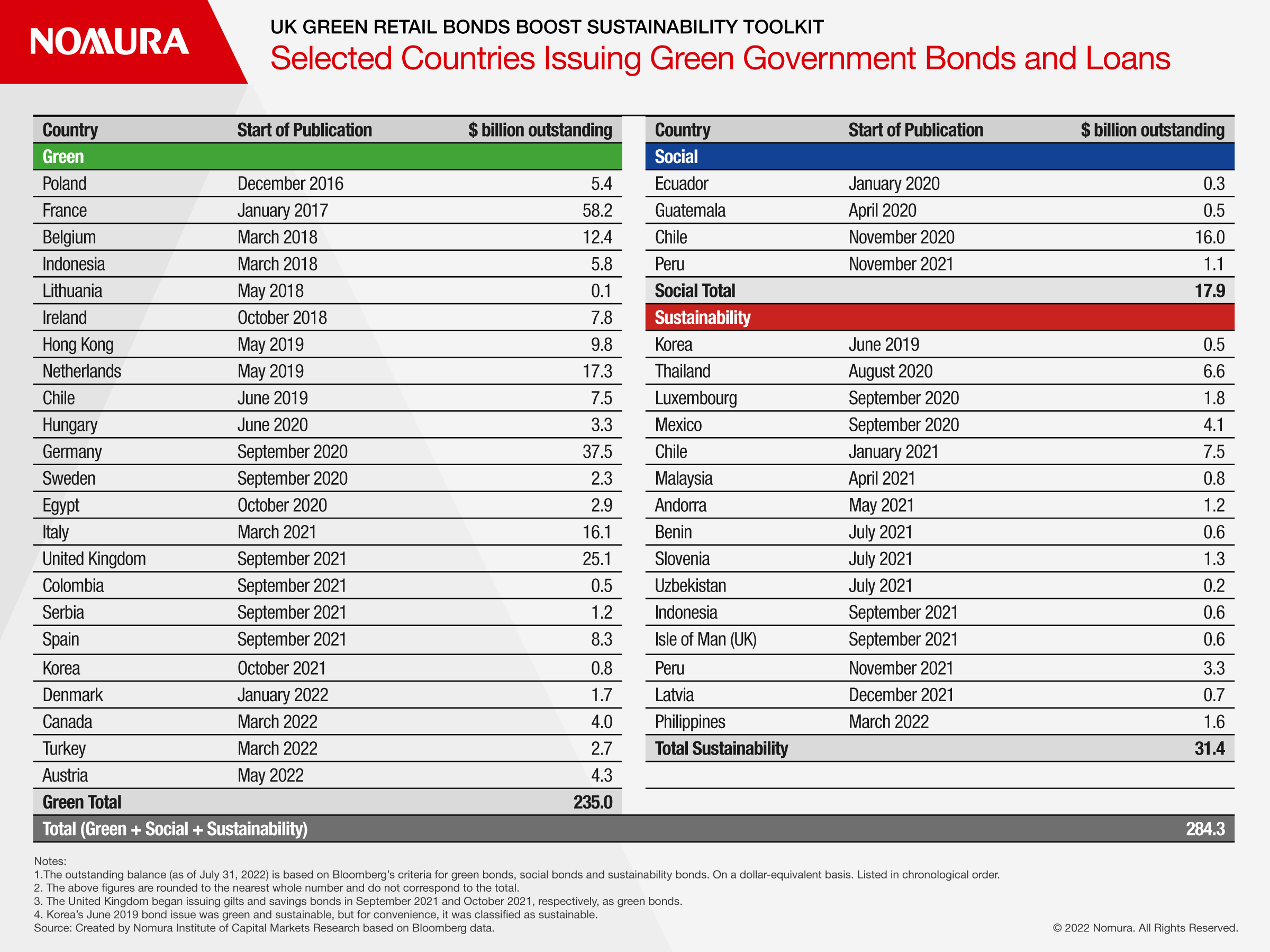

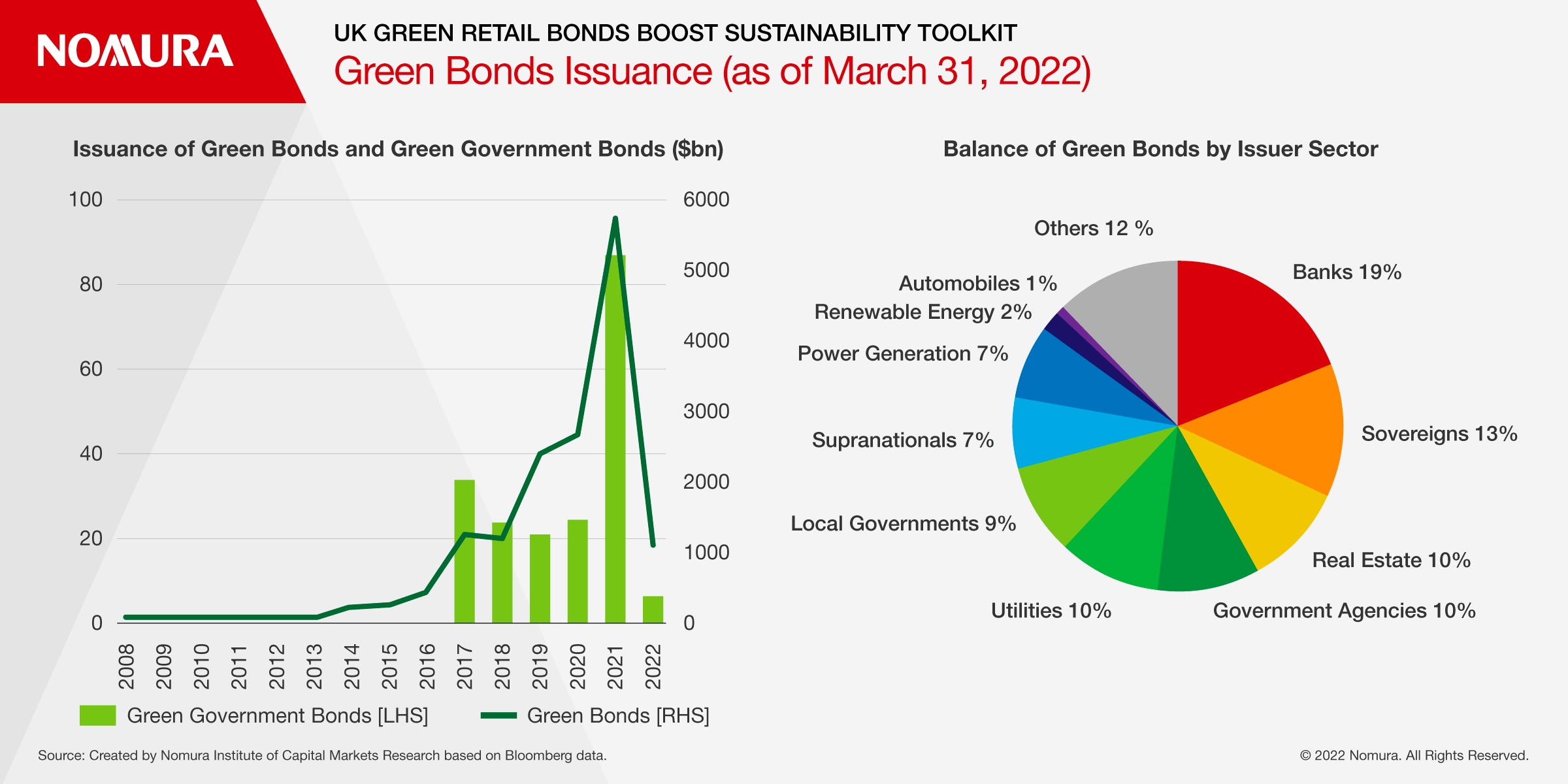

With the equivalent of over $20 billion outstanding, the UK is a significant issuer of green bonds and was the first G7 country to legislate a 2050 net zero emissions target.

By July 2022, more than 20 countries – or almost a fifth of the 131 countries committed to achieving net zero carbon emissions – had issued green bonds, amounting to the equivalent of $235 billion.

How do the Bonds Benefit the Environment?

The Green Savings Bonds – like the UK’s green bonds targeting institutional investors – were issued under the Green Finance Framework, published in June 2021. The Framework complies with the ICMA Green Bond Principles, according to a second-party opinion from Vigeo Eiris, part of Moody’s.

The Carbon Trust, an independent environmental consultancy set up by the UK government, provided a pre-issuance impact assessment of the UK government green financing programme, which includes the Green Savings Bonds. It said it was “confident that the programme will contribute to achieving net zero by 2050.” [1]

The Framework identifies six areas for eligible green expenditures:

- Clean transport

- Renewable energy

- Energy efficiency

- Pollution prevention and control

- Biological and natural resources

- Climate change adaptations

Proceeds of the Green Savings Bonds will be used for projects in these areas, such as building wind farms, accelerating the transition to electric vehicles and revamping homes and public transport, although the bonds (and their returns) are not linked to specific projects. HM Treasury (the UK’s Ministry of Finance) tracks the use of proceeds from the bonds on a dedicated green register, which is reviewed annually by an Inter-departmental Green Bond Board.

What do the Bonds Offer Investors

The Green Savings Bonds were issued by the National Savings and Investment (NS&I) Corporation, which provides cost-effective resources for the government as well as reliable savings and investment vehicles for the public. NS&I is one of the largest savings organisations in the UK, offering a range of savings and investments to 25 million customers. Buyers of the Green Savings Bonds enjoy 100% security on all capital invested, as NS&I is fully backed by the UK Treasury.

Bonds can be purchased from a minimum of £100 to a maximum of £100,000 through NS&I’s website. Unlike bonds aimed at institutional investors, the three-year bonds must be held to maturity; there is no secondary market or way to redeem them in the interim. The October 2021 issue offered an interest rate of 0.65% while the February 2022 issue offered 1.3%; both rates were less than comparable savings products available from other institutions at the time.

The bonds’ sustainability characteristics were prioritised in marketing. The UK’s now former Chancellor (finance minister) Rishi Sunak said the goal was to “give savers across the UK the chance to back the Government’s green projects and put their money to work in the fight against climate change”. Ian Ackerley, NS&I Chief Executive, said the bonds will “support six key areas to help make our environment greener, cleaner and more sustainable.” [2]

The Impact of Green Savings Bonds

While the funds raised from the Green Savings Bonds are likely to total just £300 million by the end of the financial year[3] – compared to £15 billion in green gilts to be sold by the HM Treasury to institutional investors – they are nevertheless a significant development, both for the UK government and the green bond market globally.

For the UK government, the Green Savings Bonds confirm the appeal of hold-to-maturity savings products for retail investors, provide a new financial investment vehicle for savers, and serve to publicise the country’s climate change measures to its citizens.

Globally, the success of the UK’s Green Savings Bonds has already inspired issuance elsewhere. In April, Hong Kong issued a green retail bond. The government more than tripled the maximum offer size to HK$20 billion ($2.56 billion) for the three-year bond. Interest is paid every six months based on the inflation rate over that half-year period, with a guaranteed minimum payment of 2.5%. [4]

In August, Singapore issued a S$2.4 billion ($1.7 billion) 50-year sovereign green bond priced at 3.04%. S$2.35 billion of the inaugural issuance was placed with institutional and accredited investors with the remaining S$50 million offered to individual investors. As governments around the world consider green retail bond issuance, it is important that they:

- Differentiate green retail bonds from other green financial products. In addition, with inflation increasing in most countries, interest rates are likely to need to rise to attract demand. Governments should also seek to improve purchase limits in order to optimise bond sales. More generally, governments must ensure the transparency of the bond issuance process, and seek to create an ongoing impact from green projects.

- Provide information that meets the requirements of retail investors. Information about the allocation of funds and impact reports have historically been tailored for institutional investors. Retail investors may need information that is easier to understand if green retail bonds are to be seen as credible.

- Use retail bonds to highlight climate change measures. As well as communicating details relating to green retail bonds via traditional investor relations strategies, governments should aim to increase public interest in and understanding of the country’s climate change measures when issuing green retail bonds. The use of social media, and even opportunities to visit and use green projects relating to bond issuance, could help to stimulate public interest.