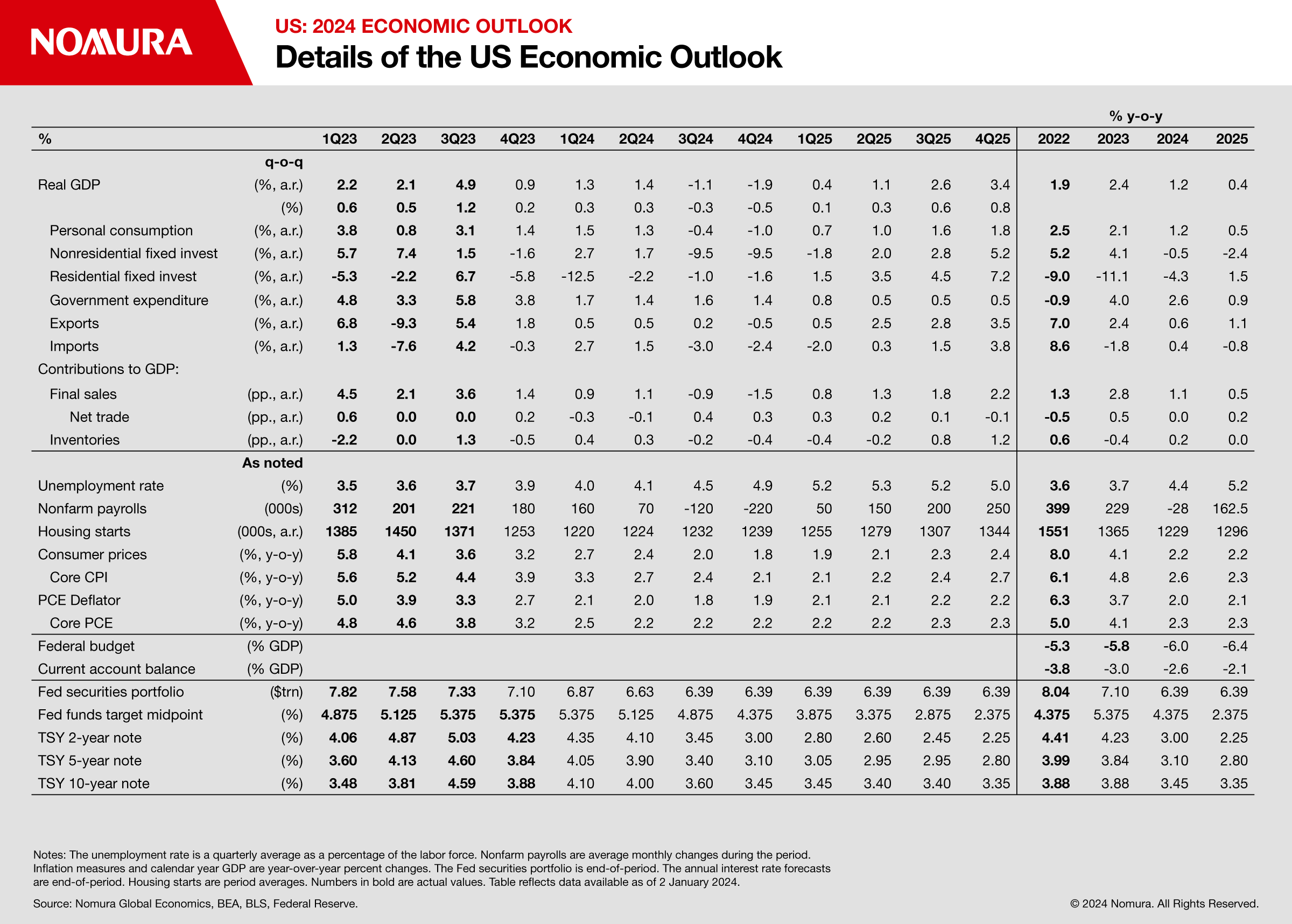

US 2024 Outlook – Slowdown, Recession and Last-Mile Inflation Risks Ahead?

US growth momentum is slowing following the surprising resilience in 2023. We expect real GDP growth to average close to zero for 2024, with a below-trend average of 1.3% in H1 ahead of a mild recession in H2.

Tight financial conditions will weigh on the cyclical sectors and lead to strains on private sector balance sheets. Disinflation is likely to continue through 2024, but progress could be uneven. Wage growth, in particular, is likely to remain elevated, raising the risk of an eventual inflation reacceleration or ‘last mile’ inflation persistence.

Disinflation, sluggish growth, and FOMC’s recent dovish shift towards balanced risks, will likely lead to a pre-emptive rate cut of 25bp in June 2024, but an aggressive rate cutting cycle seems unlikely until a recession starts in H2 2024.

We expect the Fed to begin a 25bp per meeting cutting cycle and halt balance sheet reduction once a recession is underway in September.

Slowdown, recession and last mile inflation risk

Growth momentum is slowing

After surprising

strength in 2023, growth momentum appears to be cooling. Financial

conditions have eased recently, but remain restrictive, which

will likely exert downward pressures on the economy with a

lag. Households and businesses have been well-insulated from rising

interest costs so far, but higher borrowing costs will increasingly weigh on

cyclical spending.

We expect business

financial stress to intensify throughout the year, with default rates

continuing to rise. Slowing growth and inflation will also likely lead to a

deceleration in revenues, with a strong dollar adding additional headwinds to

multinational corporations and export-driven businesses.

In addition to looming

headwinds, some one-off positive shocks for capex are likely to fade.

Industrial policy from CHIPS and the Inflation Reduction Act (IRA)

led to a surge of investment in the tech sector in 2023. We do not expect

a sharp reversal, but the fastest pace of increase has likely passed.

The labor market is beginning to cool

Labor markets have slowed significantly, even without a sharp growth downturn or widespread layoffs. The monthly run-rate for nonfarm payrolls has decelerated to below 200k — in line with its pre-pandemic average — and the unemployment rate has drifted higher to 3.7%.

So far, this slowdown appears to be a normalization after frenzied hiring and labor hoarding in 2021-22. Measures of hiring and labor demand have moderated, and the pace of layoffs has increased modestly.

Taken together, slower hiring and a faster run-rate for layoffs suggest a further increase in the unemployment rate. We expect the unemployment rate to move above 4% in H1 2024, with a sharper increase only occurring later after the onset of recession

Consumers are resilient, but growth is moderating

Solid labor income growth will likely support consumer spending. Tighter financial conditions are a strain for households, but this is more likely to lead to a slowdown than an outright downturn in the near term.

Household balance sheets have been well insulated from higher rates and tighter financial conditions. Around 70% of household debt is mortgage borrowing, which is overwhelmingly fixed-rate debt still paying low rates. Despite home price appreciation and rising homeownership rates, mortgage debt payments are still below 2019 levels as a percentage of disposable personal income.

Despite this solid foundation, headwinds are building for household finances. Most household liabilities are insensitive to rising rates, but credit card interest costs are increasing, and delinquency rates have picked up. The resumption of student loan payments (following years of forbearance) is also a drag on household cashflows.

Consumer surveys demonstrate that higher borrowing costs and tighter lending conditions are weighing on demand for vehicles and other large durable goods. The University of Michigan consumer sentiment survey showed a sharp rise in the share of households that claim it is a bad time to make large purchases due to high interest rates. Rejection rates for consumer credit applications have also increased, and a rising share of households indicated that they have been discouraged from even applying for credit.

Disinflation is underway

We believe disinflation will likely continue in 2024 and forecast core PCE inflation to decelerate to 2.2% in Q4 2024 from 3.2% as of November 2023. Disinflationary forces appear to be concentrated in vehicle prices and rent, while we expect inflation of supercore components to moderate more gradually.

Higher interest rates started to drive down vehicle prices, which make core goods prices one of the primary sources of disinflation. Leading indicators point towards continuing deceleration in rent inflation through 2024. Expected moderation in vehicle prices and rent inflation will likely have a larger disinflationary impact on core CPI than core PCE inflation.

The remaining part of core inflation is non-rent core service prices, so-called supercore inflation. CBO and CMS forecasts for cost increases for Medicare services point to stable inflation for healthcare service prices. However, about one-third of supercore components such as food service prices seems to be sensitive to wages. Based on our analysis, wage growth tends to be sticky and thus those wage-sensitive prices will likely moderate more gradually than rent and core goods prices. We expect supercore PCE inflation to fall to 3.1% y-o-y in Q4 2024, from 3.5% in November 2023.

Last mile risks

Realized inflation is

falling, but there will be lingering risks of a reacceleration. We think wage

growth and

hence supercore inflation provide an important guide for assessing these

risks. Many policymakers (including Chair Powell) have argued that any

evidence that tightness in the labor market is no longer easing could put

further progress on inflation at risk, which underlines the importance of labor

markets and wage growth for the inflation outlook (Fig. 13).

One lesson from the

1970s inflation was not to declare victory prematurely without broad

corroboration that both inflation and wage growth have slowed (Fig. 14). In the 1970s, a series

of shocks (including the two oil crises and depreciation of the US dollar

associated with the end of the Bretton Woods exchange rate regime)

exerted inflationary forces. The Fed tightened policy to prevent a

positive output gap, but did not remain restrictive enough to address building

demand pressures in wage growth and persistent services inflation. Prices

reaccelerated and expectations became unanchored, leading to a prolonged period

of high and volatile inflation.

Fed is done hiking, but aggressive rate cuts are unlikely as long as growth remains resilient

Disinflation and sluggish growth are likely to discourage the Fed from hiking rates further, and we expect a tentative start to rate cuts in June 2024. However, we believe the Fed would not be comfortable easing aggressively until inflation and wages decelerate more decisively.

In our view, it will be difficult for the Fed to ease quickly as long as growth is solid and realized inflation remains above target. We see two key uncertainties that should discourage aggressive rate cuts until a recession is underway.

First, as the prior sections suggest, inflation risks will likely remain skewed to the upside even when realized core PCE is printing close to the Fed’s target. It is always difficult to distinguish between temporary, volatile drivers of inflation and structural trends. Our inflation forecast for 2024 suggests disinflation will be driven mostly by noisy goods prices and backward-looking rents, raising the risk that ‘underlying’ inflation is still elevated.

Second, rate cuts would raise the risk that policy becomes accommodative. Rates are well above the Fed’s model-based estimates of ‘neutral,’ but these models are unreliable in real time. Small differences in assumptions lead to significant differences in estimates across models.

In the past, rate cuts outside recessions have been limited, and were often preceded by financial stress. Since rate decisions were made public in 1994, there have only been three instances of non-recessionary rate cuts, in 1995, 1998, and 2019 — following the Mexican peso crisis, LTCM, and QT-related money market stress. In each case, there was only 75bp of cumulative easing. Without salient financial stability risks, the pace and magnitude of pre-emptive rate cuts will likely be limited.

Why a recession is likely

Tighter financial

conditions have not led to acute stress yet, but in our view, the risk of a

downturn remains elevated.

The Fed’s aggressive

rate hikes and slowing inflation are raising real interest rates. In addition,

the economy is slowing, weighing on revenue growth of US businesses.

Refinancing maturing corporate debt in 2024 and subsequent years will also increase

the debt burden on businesses gradually. The banking sector is still facing

pressures as interest margins for small banks have continued to be squeezed.

Against this backdrop, credit conditions for the business sector continue to

tighten, which corroborates recent increases in the speculative corporate bond

default rate.

Based on our

calculation, the interest coverage ratio, a measure of the ability of businesses

to pay interest, started to deteriorate this year. Historically, changes in the

interest coverage ratio tend to affect certain types of business investment

with a one-year lag. Overall, we will likely see a more substantial impact from

credit tightening on business investment in coming quarters, causing a

capex-driven recession in H2 2024.

The Fed can cut quickly and end QT when a recession is underway

Once a recession is

underway, the Fed’s employment and inflation mandate are both likely to suggest

policy can ease.

Even in a mild

recession, unemployment is likely to rise significantly. We expect the headline

unemployment rate to rise towards 5% by the end of 2024, and increase to a peak

in the mid-5% range by 2025. Wage growth tends to be sticky early on in

recessions, but it predictably declines after a sufficient lag.

We expect a recession in

H2 2024 would likely push down supercore PCE inflation to its pre-COVID level

in 2025. Additional disinflationary forces stemming from a recession should

make the Fed confident that the risk of inflation rebounding has diminished,

enabling it to launch a large scale rate cutting cycle in September 2024, along

with an end to quantitative tightening.

Fiscal policy on hold

With divided government

and a national election looming in November, we do not expect any significant

fiscal easing in response to a recession. 2024 is an election year and the

administration cares about slowing growth. However, House Republicans likely

have less incentive to support policy that boosts the economy. Inflation risks

and concerns of elevated deficits might dampen support for stimulus, even among

Democrats.

Risk scenarios to our economic outlook

Soft landing is a risk

The drag from tight

financial conditions makes a recession seem more likely than not, however a soft landing remains

a risk.

Cyclical spending has

already fallen significantly since the start of the tightening cycle, and it is

possible that demand stabilizes even if financial conditions remain

restrictive. In addition, strong balance sheets of households might provide

more support to the broader economy than we currently assume.

Potential changes to the Fed’s reaction function

Since late 2021, the Fed

has been prioritizing the inflation leg of its dual mandate. Officials have

repeatedly said that returning inflation to 2% was their priority, and that

they would do whatever was necessary to achieve this objective.

Since October, there

have been signs of wavering. Chair Powell admitted that the FOMC started to discuss

rate cuts in 2024 at the December meeting, and he did not push back against

aggressive market prices of five to six 25bp rate cuts at his post-FOMC press

conference.

Overall, Our forecast

for Fed policy in 2024 assumes the emphasis on inflation will persist, but the

risk of a more aggressive dovish pivot has increased. Importantly, due to

policy lags, disinflation and sluggish growth will likely persist for at least

a few months regardless of the Fed’s policy approach even if easing financial

conditions exert renewed inflationary pressures with a lag. In our view, this

would risk an inflation reacceleration in the medium term, but there is no

near-term circuit breaker that would prevent the Fed from easing policy or lead

to a rapid hawkish reversal.

Severe recession and financial stress

Our expectation is that

a 2024 recession would be mild, with just two quarters of negative growth and

the unemployment rate peaking around 5.3%. In our view, this is a reasonable

base case given the fundamental strength of household balance sheets and the

lack of overinvestment during the expansion. That said, recent history shows

that recessions often trigger financial stress, leading to a negative feedback

loop and a more severe downturn.

We do not see a clear

catalyst for financial stress, but growth downturns can reveal hidden

vulnerabilities or ‘break’ otherwise healthy markets. The past three recessions

have coincided with equity sell-offs of 30% or more, and even past mild

recessions typically lead to some credit stress.

This content has been prepared by Nomura solely for information purposes, and is not an offer to buy or sell or provide (as the case may be) or a solicitation of an offer to buy or sell or enter into any agreement with respect to any security, product, service (including but not limited to investment advisory services) or investment. The opinions expressed in the content do not constitute investment advice and independent advice should be sought where appropriate.The content contains general information only and does not take into account the individual objectives, financial situation or needs of a person. All information, opinions and estimates expressed in the content are current as of the date of publication, are subject to change without notice, and may become outdated over time. To the extent that any materials or investment services on or referred to in the content are construed to be regulated activities under the local laws of any jurisdiction and are made available to persons resident in such jurisdiction, they shall only be made available through appropriately licenced Nomura entities in that jurisdiction or otherwise through Nomura entities that are exempt from applicable licensing and regulatory requirements in that jurisdiction. For more information please go to https://www.nomuraholdings.com/policy/terms.html.