US: Recession Imminent – Will the Economy Recover by 2024?

We continue to expect an imminent recession and look for an only muted rebound in real GDP growth during 2024

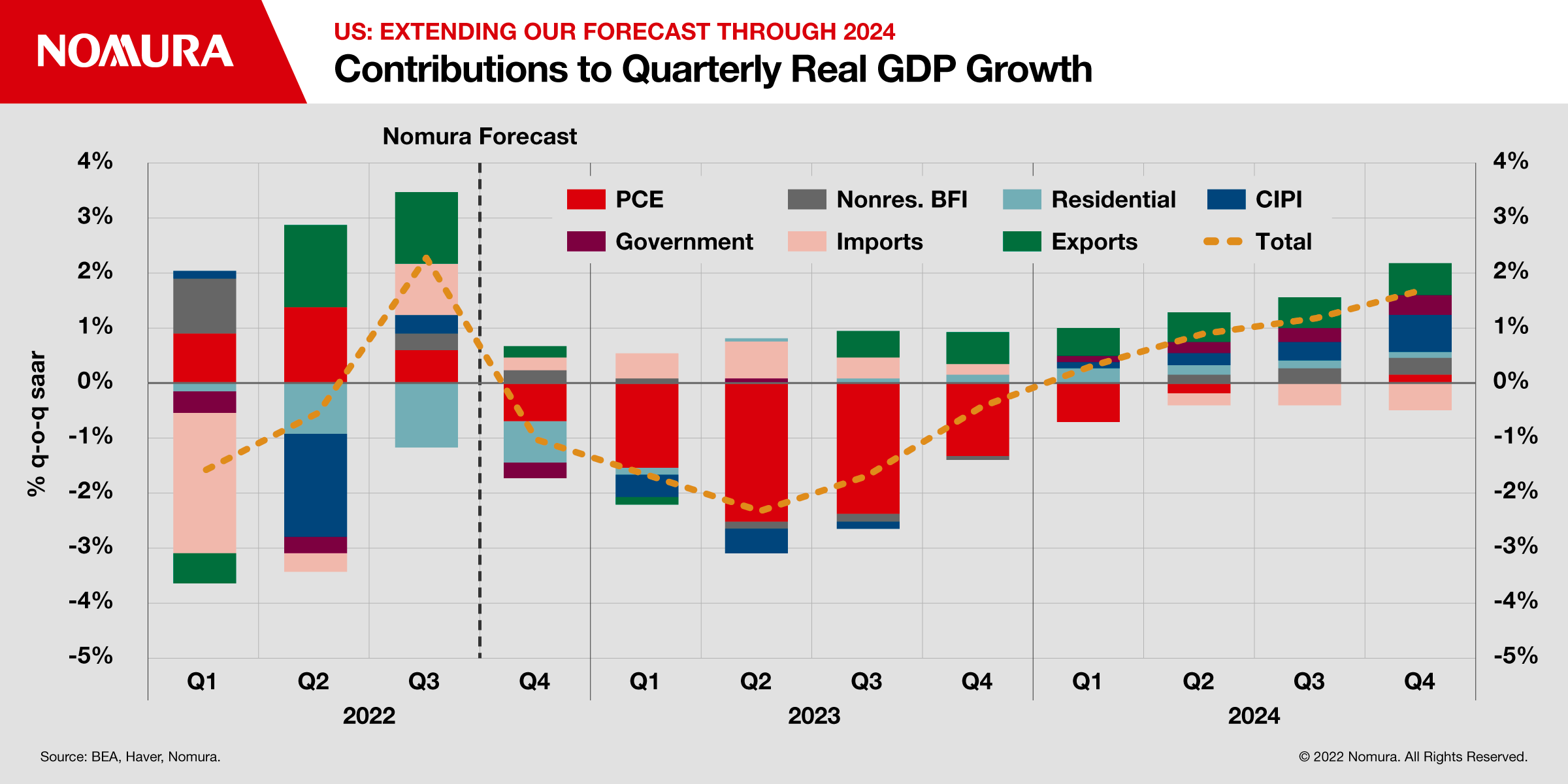

We maintain our call for a US recession to begin in Q4 2022.

After five consecutive quarters of negative real GDP growth, 2024 will likely see an only muted recovery.

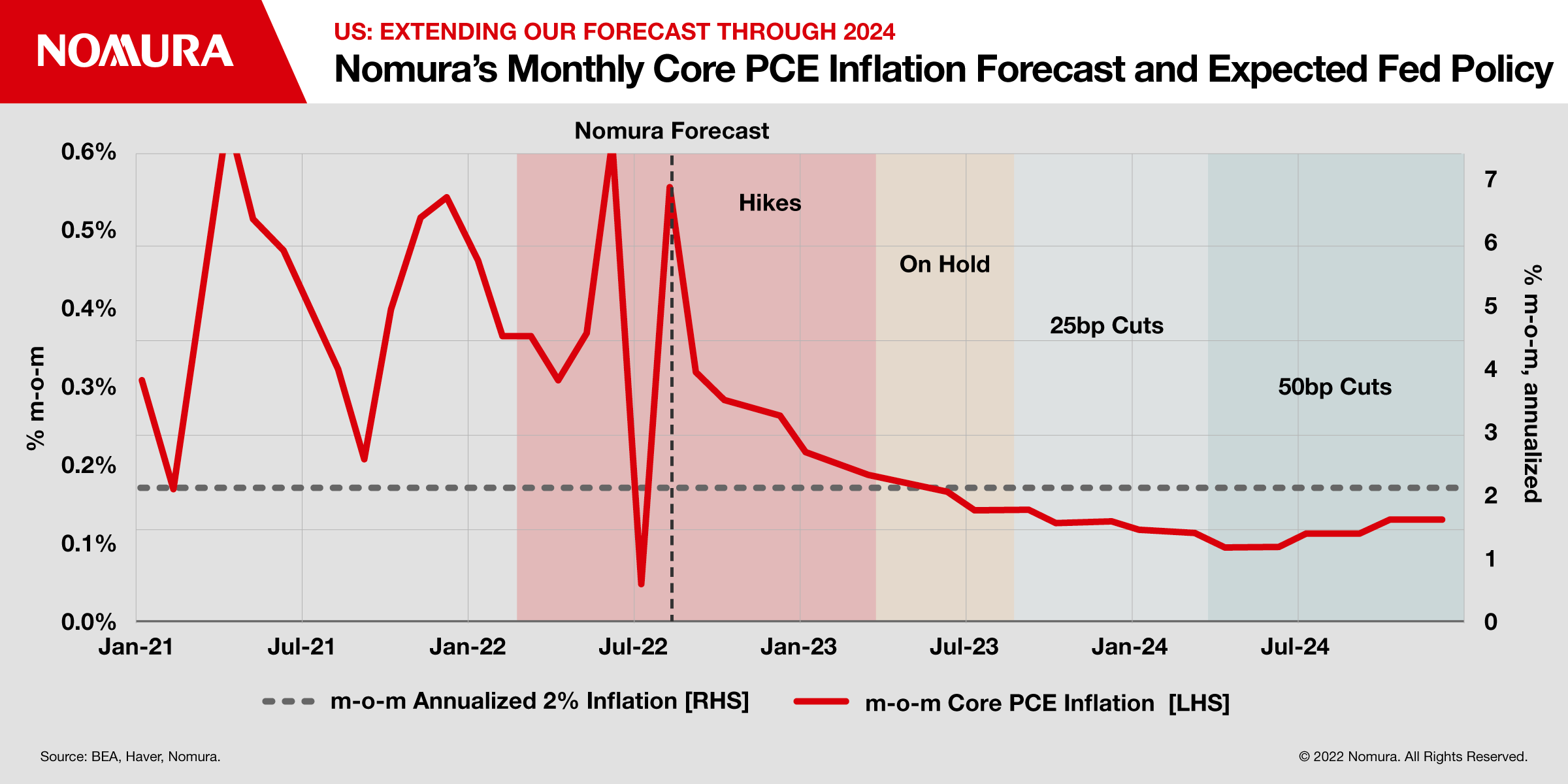

We expect hikes of 75bp in November and December, 50bp in February and 25bp in March to a terminal rate of 5.25-5.50% before cuts in September 2023.

Near-term Fed policy will likely continue to be driven by monthly core inflation readings, as the Fed’s concerns have shifted to underlying inflation.

We

continue to expect a recession, with a muted 2024 recovery

A prolonged recession remains our base case, but with a few adjustments

We continue to expect a recession – under the NBER definition of a

broad-based decline in activity – to begin in Q4 2022, with risk of a

slightly later start in 2023. The broad contours of our forecast through 2023

remain unchanged, including an expected five consecutive quarters of negative

real GDP growth.

In 2023, we expect a slightly

larger downturn in real GDP, down 1.8pp peak to trough relative to our previous

forecast of 1.5pp, as inflation appears increasingly entrenched and supply

constraints, labor shortages in particular, eased at a slower pace, warranting

more demand destruction to control inflation. Consequently, we expect the

unemployment rate to peak at a slightly higher level, 6.4% instead of just

below 6%.

Incoming data across a range of industries support our recession call

Relative to our previous major forecast update in June 2022, when we first called for a recession, incoming data continue to point to a moderate slowdown in activity

Real consumer spending remains lackluster and, while consumer sentiment has moved off recent lows, it remains depressed by historical standards. The weakness already apparent in consumer activity – despite still-strong albeit slowing labor market conditions – suggests consumer spending will weaken further along with the labor market in coming months.

The housing market continues to experience one of the most rapid declines in activity since the Global Financial Crisis (GFC), as sales and building activity pull back. Downside risks to home price growth over coming quarters remain acute, especially considering what will likely be a shift from worker to firm bargaining power in the labor market, and a potential unwind of work-from-home dynamics that boosted prices during the pandemic.

The industrial and business sector faces considerable headwinds that have shown no signs of abating, including a strong dollar, saturation of domestic consumer goods markets, high uncertainty and a bleak outlook for the global economy.

Finally, the outlook for external growth has continued to deteriorate as Europe enters recession and growth in China remains constrained by ongoing “zero-COVID” efforts.

A recession will likely be required to break inflation’s grip

While the timing remains uncertain, conviction in our view that a recession will ultimately be required to break the significant entrenchment of domestically generated US inflation has increased. Stepping back from industry-specific factors, we believe a rise in the unemployment rate will ultimately be required to weaken labor markets, slow wage growth and bring trend inflation lower.

Rapid home price growth during the pandemic has pushed up the home price-to-rent ratio to levels not seen since the early 2000s. Despite the lag with which home prices will likely respond to the downturn, we see elevated risk of price corrections, which could prolong the downturn. Moreover, if workers lose bargaining power for remote work opportunities as the unemployment rate rises, COVID-related migration could reverse, which may exert downward pressure on home prices in areas that benefitted from the shift in work conditions.

The recovery in 2024 is likely to be muted

We expect the Fed’s reaction to the oncoming recession to be quite delayed relative to historical standards. Instead of cutting rates aggressively at the onset of the downturn, FOMC participants will be raising rates and holding them at a restrictive level with rate cuts starting only in September 2023 and at a cautious initial pace.

Moreover, our assumptions on fiscal policy have not changed: despite high uncertainty, divided government in 2023-24 appears likely following the November 2022 midterm elections. Similar to monetary policy, fiscal policy will likely turn from a significant tailwind during the pandemic to a notable headwind, with potential volatility around debt limit and government spending deadlines.

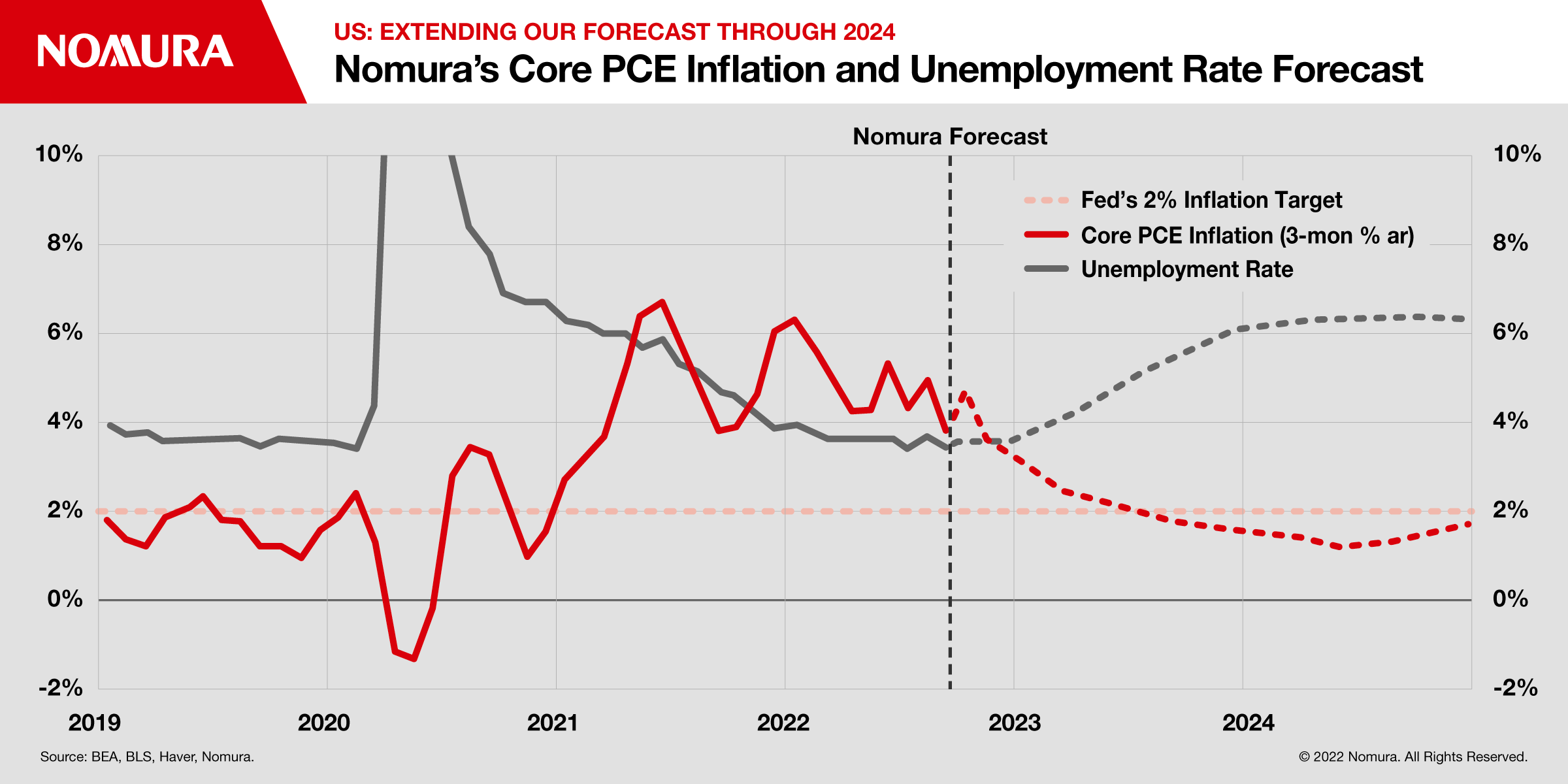

Inflation will likely moderate substantially

We expect

y-o-y core PCE inflation to remain elevated above 4% through end-2022 but

substantial moderation to about 2% in December 2023 appears likely. Continued

easing of supply chain constraints and our forecasted recession will

likely exert disinflationary pressures. Despite our expectation that the

recession ends in Q4 2023, inflation remains a lagging indicator of the

broader economic trend, and we expect disinflationary shocks to persist into

2024.

Expected

negative payback of higher energy prices and an anticipated normalization of

food price inflation will likely push down headline inflation. We expect

headline PCE inflation to underperform core PCE inflation on a y-o-y basis,

starting in Q2 2023 and through end-2024.

Within core

PCE inflation, we expect inflation of rent-related components to continue to

accelerate on a y-o-y basis until Q2 2023 as official rent data tend to reflect

the lagged impact of tightening of rental housing markets. We think regular

rent inflation will start to moderate in mid-2023 and continue to decelerate in

2024, coming back to its normal pre-pandemic level of 3.5% by end-2024, down

from our expected peak of 8.8% y-o-y.

On the goods

side, we expect annual price changes of certain goods, such as used vehicles

and home appliances, to turn negative by end-2022, followed by substantial

declines in 2023, reflecting recession-induced downward pressures. In addition,

other goods prices, which have shown resilience so far this year, including new

vehicles, furniture, paper products and apparel products, will likely start to

decline on an annual basis by Q2 or Q3 2023, as demand-supply imbalances

continue to ease.

Contributions to Quarterly Real GDP Growth

The Fed and fiscal policy

Monthly inflation measures remain critical for the Fed’s policy decisions

We believe Fed participants will feel comfortable dialing back the pace of rate increases in early 2023 and eventually pausing, before beginning rate cuts in September 2023. From the perspective of monetary policy, many FOMC participants have begun to more clearly link the policy rate path to the trajectory of monthly, instead of annual, core PCE or trend inflation

Beyond early 2023, we think the downtrend of monthly core PCE inflation will likely continue. With the unemployment rate rising rapidly at that point, likely above 5% by September 2023, we believe the underperformance of inflation will allow the Fed to refocus on its dual mandate, resulting in rate cuts as inflation risks continue to diminish.

Under our inflation outlook, we think the Fed will likely keep cutting rates during 2024 as the risks of inflation re-accelerating remain low, reaching an end-2024 policy rate of 1.00-1.25%.

Nomura's Monthly Core PCE Inflation Forecast and Expected Fed PolicyNomura's Core PCE Inflation and Unemployment Rate Forecast

Low expectations for fiscal policy, but with slightly more upside risk

The outlook for fiscal policy has become modestly more uncertain, but our expectations for fiscal stimulus remain low. While we expect divided government in 2023 – as Republicans appear likely to retake the House of Representatives in November, and may also take the Senate – the outlook for Democrats has improved since mid-June.

Consequently, while we believe fiscal policy will remain a headwind to growth in 2023-24, if Democrats surprisingly retain control of both the House and Senate during the midterm elections, we cannot rule out some amount of fiscal stimulus in late 2023 and 2024, as the economy remains mired in recession. That said, the probability of such an event likely remains low, and we would not expect any significant fiscal support in H1 2023, as it may result in a more aggressive response from the Fed to ensure inflation returns to target.

This content has been prepared by Nomura solely for information purposes, and is not an offer to buy or sell or provide (as the case may be) or a solicitation of an offer to buy or sell or enter into any agreement with respect to any security, product, service (including but not limited to investment advisory services) or investment. The opinions expressed in the content do not constitute investment advice and independent advice should be sought where appropriate.The content contains general information only and does not take into account the individual objectives, financial situation or needs of a person. All information, opinions and estimates expressed in the content are current as of the date of publication, are subject to change without notice, and may become outdated over time. To the extent that any materials or investment services on or referred to in the content are construed to be regulated activities under the local laws of any jurisdiction and are made available to persons resident in such jurisdiction, they shall only be made available through appropriately licenced Nomura entities in that jurisdiction or otherwise through Nomura entities that are exempt from applicable licensing and regulatory requirements in that jurisdiction. For more information please go to https://www.nomuraholdings.com/policy/terms.html.