US: Staring into the Void – A Recession is Now Likely

The Fed’s commitment to restoring price stability will likely push the economy into a downturn

With rapidly slowing growth momentum and a Fed committed to restoring price stability, we believe a mild recession starting in Q4 2022 is now more likely than not.

Financial conditions are likely to tighten further, consumers are experiencing a significant negative sentiment shock, energy and food supply disruptions have worsened and the outlook for foreign growth has deteriorated. All these factors will likely contribute to the expected downturn.

Relative to previous downturns, the significant strength of consumer balance sheets and excess savings should mitigate the speed of the initial contraction. However, policymakers’ hands are tied by persistently high inflation, limiting any initial support from monetary or fiscal stimulus.

Factors

driving the downturn

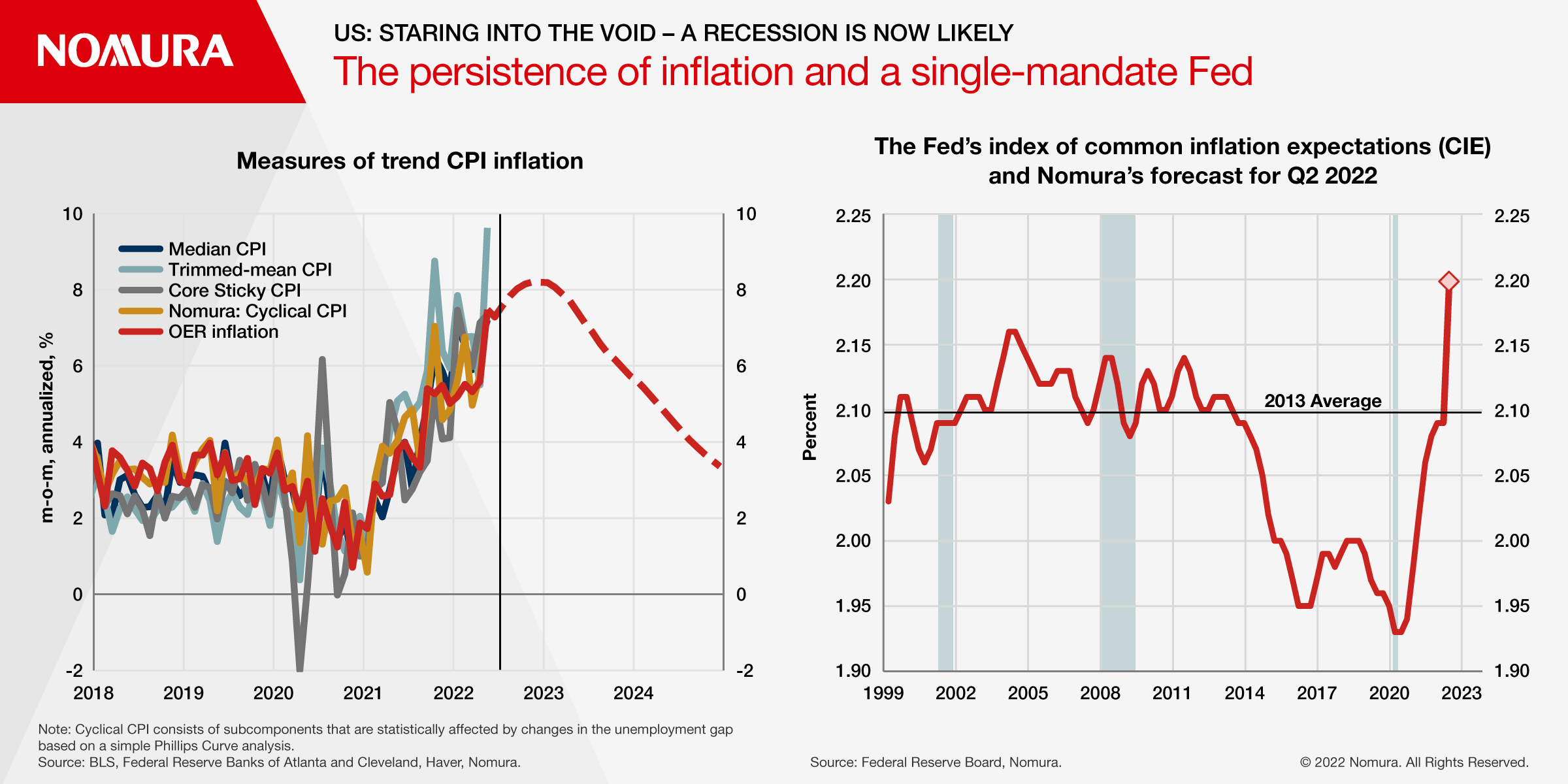

The persistence of inflation and a single-mandate Fed

From a very high level, the ongoing persistence of elevated inflation and growing evidence of unanchored inflation expectations are the two key drivers of our expected growth downturn. Despite the Fed’s significant hawkish pivot since November 2021, inflationary pressures have not eased meaningfully and may have arguably worsened. Inflation expectations are showing growing signs of being unanchored.

Against that backdrop, we believe the Fed’s efforts to realign demand with depressed supply to rein in price pressures will ultimately drive the economy into a mild recession. Fed officials have been unequivocally clear they will prioritize price stability, the frequently cited “bedrock” of the institution, above all else. With increasingly entrenched inflationary pressures and rapidly tightening financial conditions, those efforts are likely to have a more pronounced impact on demand relative to our previous expectations just a few months ago.

The persistence of inflation and a single-mandate Fed

Recent financial conditions developments and their implications for growth

Financial conditions have tightened considerably in 2022, but not yet to levels that would suggest a significant drag on growth. Broad measures of equity prices have declined between 20-30% and BBB option-adjusted corporate credit spreads have widened over 60bp. While NFIB’s latest data suggest small businesses are not yet experiencing a material deterioration in credit conditions, that could soon change.

That said, considering our expectations for Fed policy and inflation, we believe financial conditions are likely to tighten further. Equity valuations remain rich by historical standards with significant risk of lower corporate earnings, and the evaporation of the “Fed put” in an environment with historically elevated inflation suggests uncharted territory ahead. The acceleration in tightening over recent months, particularly for the equity market, could have a nonlinear impact on growth considering the broad weakness in risk assets, similar to the burst of the “dot com” bubble in the early 2000s. Consequently, we expect our financial conditions index to soon move more deeply into negative territory.

Interest-rate sensitive GDP components

Within the real economy, interest-rate sensitive GDP components are likely to accelerate the downturn. Already, housing demand has shown signs of pronounced weakness as both existing and new home sales move lower and starts and permits lose steam. The sensitivity of US GDP growth to higher interest rates could be larger in this cycle, considering interest rate-sensitive components comprise a historically elevated share of real GDP.

Rapid home price growth during the pandemic has pushed up the home price-to-rent ratio to levels not seen since the early 2000s. Despite the lag with which home prices will likely respond to the downturn, we see elevated risk of price corrections, which could prolong the downturn. Moreover, if workers lose bargaining power for remote work opportunities as the unemployment rate rises, COVID-related migration could reverse, which may exert downward pressure on home prices in areas that benefitted from the shift in work conditions.

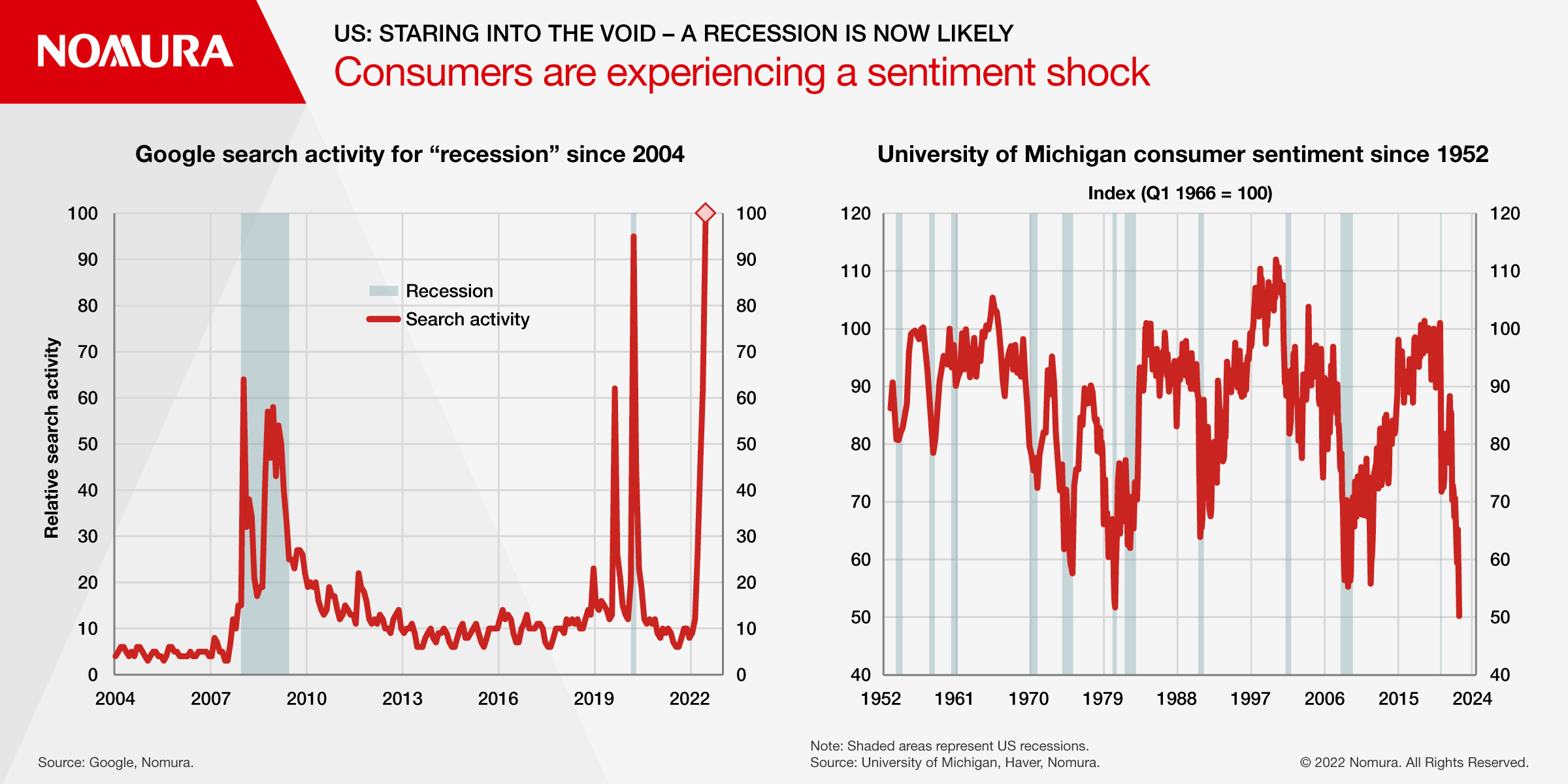

Consumers are experiencing a sentiment shock

For much of 2022, we have expected strong service consumption – due to re-opening, pent-up demand and excess savings – to support overall consumer spending despite headwinds for goods consumption. However, in recent months, meaningful signs of a negative consumer sentiment shock have emerged. Google search activity for “recession” has increased above levels that prevailed during the Global Financial Crisis (GFC) and the University of Michigan’s consumer sentiment index dropped to its lowest level on record in June

Consumer are experiencing a sentiment shock

Commodity price shocks risk becoming the new normal

In addition to tighter financial conditions, the exposure of interest-rate sensitive sectors and a consumer sentiment shock, the outlook for supply shocks – particularly for energy and food – has continued to deteriorate this year.

The ongoing Russia-Ukraine war and its impact on global commodity markets and supply chains has shown few signs of improvement, and may have started to become more entrenched. After commencing 2022 around $75/barrel and spiking to as high as $123/barrel at the onset of the war, WTI crude oil prices have remained persistently high, averaging close to $120/barrel during June. Retail gasoline prices in the US have risen sharply and persistently from around $3.30/gallon at end-2021 to over $5.00/gallon in June. Increased demand from the ongoing reopening of China after Omicron-linked lockdowns suggests further upside risk to energy prices.

Similar to higher energy prices, food price increases have been widespread and persistent, both for food-at-home (grocery stores) and food-away-from-home (restaurant) prices. Disruptions emanating from the war and the lingering impact of COVID-induced supply chain snarls have both contributed to what may be a prolonged period of elevated food price inflation.

Against that backdrop, the Fed has been compelled to more carefully pay attention to non-core inflation components considering their importance for consumer sentiment and inflation expectations. Rising inflation in these areas may lead to inflation expectations un-anchoring further, thereby risking high inflation to become further entrenched.

Despite

weak sentiment, consumer fundamentals are solid

Heading into an expected recession, consumer fundamentals remain on historically solid footing. The household debt-service ratio remains well below its pre-pandemic level, and despite the recent deterioration in stock prices, the wealth-to-income ratio for households remains elevated. Excess savings have supported consumption in recent months, with the personal saving rate dropping notably below its pre-pandemic average.

The combination of significant balance sheet strength and excess savings suggests the downshift into recession will likely be more gradual for consumers relative to previous cycles. Compared to the significant deleveraging that occurred after the Global Financial Crisis (GFC), we do not see clear signs of a consumer “accelerant” for this recession.

Policy

support will be on the sidelines

One of the most significant differences between our expectation for this recession and prior episodes involves the response from policymakers. In the current high-inflation environment, both monetary and fiscal policy are likely to be much more restrained in their response relative to previous recessions.

The Fed’s

hands are likely to be tied through 2022 by elevated inflation

Fed officials have been clear they will prioritize restoring price stability above all else. Unfortunately, we believe monthly core inflation is likely to remain quite elevated and above levels with which the Fed would be comfortable, at least through 2022, and likely into early 2023.

Over the past decade and a half, the proximity of the Fed’s policy rate to the effective lower bound (ELB) has helped establish a standard “playbook” for responding to recessions, exemplified during the COVID crisis: cut rates swiftly and sharply to the ELB and prepare for large scale asset purchases (LSAPs, or QE), in order to provide additional accommodation.

That playbook is likely to be of little use to policymakers in the current environment, due to persistently elevated inflation. While we expect rate cuts to start in H2 2023, they will likely come much later than they otherwise would have absent strong inflationary pressures. Moreover, the pace of rate cuts is likely to be slower than in previous recessions. We believe the Fed will continue to reduce the size of its balance sheet into 2023 considering its historically elevated size and their plans to tighten financial conditions beyond raising short-term rates. Both actions run against what policymakers would likely prefer to do in a standard recession.

Fiscal policy support is likely to be absent, or outright restrictive

Similar to monetary policy, we believe fiscal policy will largely remain on the sidelines for the expected recession, aside from the regular impact of automatic stabilizers like unemployment insurance. Policymakers in Washington across the spectrum have increasingly taken the view that significant, and unprecedented, fiscal support during the pandemic helped exacerbate inflationary pressures. That experience, combined with widespread voter dissatisfaction due to inflation, will make many members of Congress reluctant to provide any kind of discretionary fiscal stimulus.

One of the most striking indications of just how quickly the conversation in Washington has changed has been recent commentary from Biden administration officials on the potential for deficit reduction to help combat inflation. Treasury Secretary Yellen in particular has suggested deficit reduction could help address elevated inflation pressures.

Conclusion

We expect a modest recession to start in Q4 2022

Combining the factors above, we expect a modest recession to start in Q4 2022. Relative to previous downturns, we expect a shallower and longer path, for three reasons. First, as noted above, robust consumer balance sheets and excess savings should limit how quickly growth decelerates. Second, the lack of policy support – monetary and fiscal – at the onset of the recession will likely prolong its length. Third, despite some concerns over corporate debt, there is no obvious financial accelerator to amplify the recession shocks like the GFC.

This content has been prepared by Nomura solely for information purposes, and is not an offer to buy or sell or provide (as the case may be) or a solicitation of an offer to buy or sell or enter into any agreement with respect to any security, product, service (including but not limited to investment advisory services) or investment. The opinions expressed in the content do not constitute investment advice and independent advice should be sought where appropriate.The content contains general information only and does not take into account the individual objectives, financial situation or needs of a person. All information, opinions and estimates expressed in the content are current as of the date of publication, are subject to change without notice, and may become outdated over time. To the extent that any materials or investment services on or referred to in the content are construed to be regulated activities under the local laws of any jurisdiction and are made available to persons resident in such jurisdiction, they shall only be made available through appropriately licenced Nomura entities in that jurisdiction or otherwise through Nomura entities that are exempt from applicable licensing and regulatory requirements in that jurisdiction. For more information please go to https://www.nomuraholdings.com/policy/terms.html.