Moving the U.S. waste industry to a more circular and recycling-led market represents a major investment opportunity according to waste sector investors and executives at Nomura Greentech’s Sustainable Leaders’ Summit. However, that effort faces headwinds due to ingrained consumer behaviours, landfill economics, and policy fragmentation which require better incentives to change.

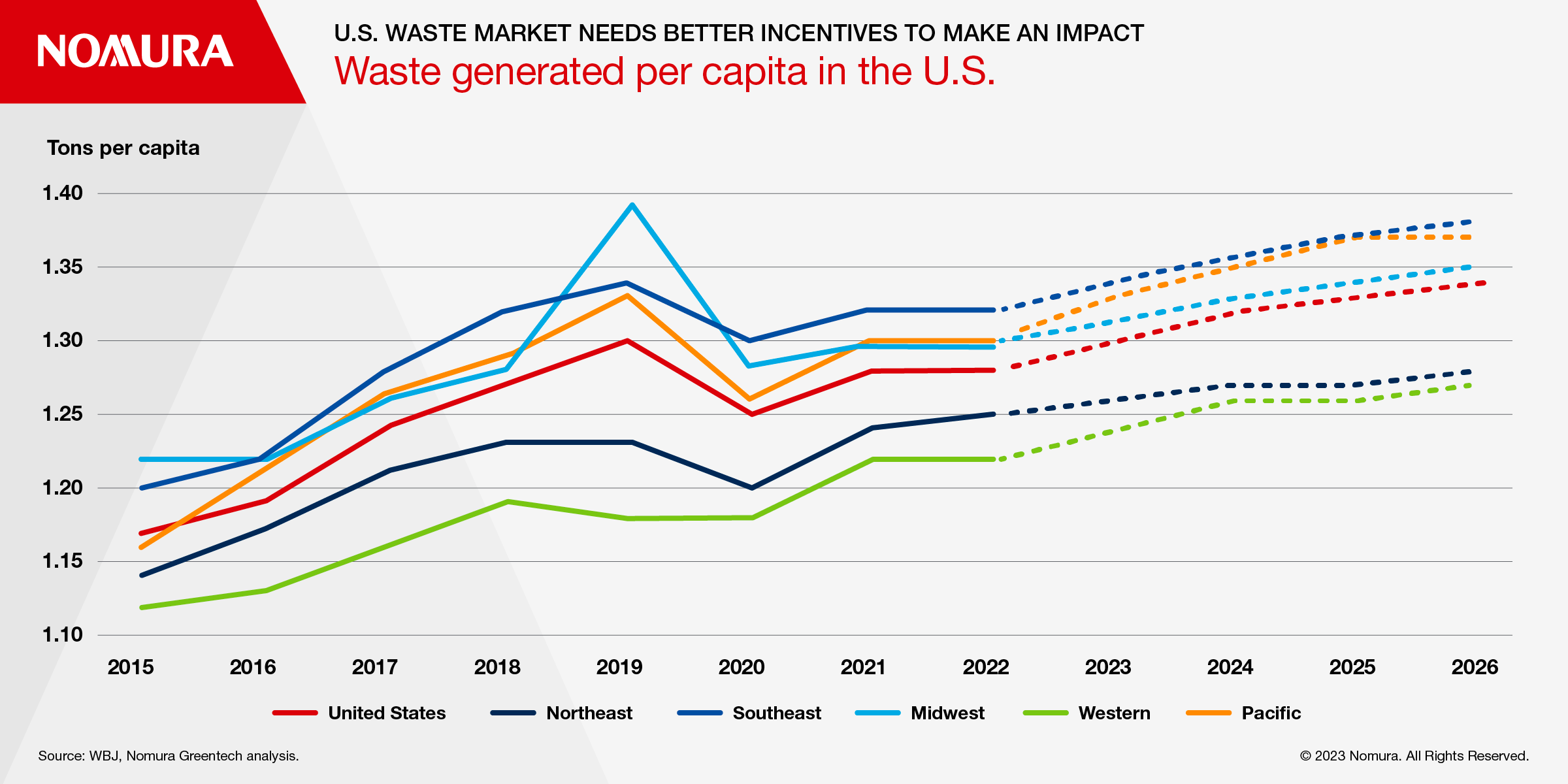

Waste is an enormous problem with the average American producing more than 1.25 tons per year and that figure is set to keep increasing, Waste Business Journal data shows.

The challenge is that it is so profitable to put low or negative value material into landfills, a leading investor said at the summit, which is held under the Chatham House Rule.

In the U.S., only 10 states have “Bottle Bills” which financially incentivise consumers to return their glass vessels to recycling stations, which means that 28 billion glass bottles and jars go to landfills every year and only 3 million tons are recycled due to varying policies across different states.

“In reality, it is a complete hodgepodge, incredibly local and unnecessarily complicated, making it hard for consumers to navigate,” the investor said.

Sensing a shift in direction for the industry, some waste majors are starting to be more strategic. WM and Republic Services – the two U.S. market leaders – among others, are expanding into renewable natural gas production. They are also spending hundreds of millions of dollars investing in their recycling technologies and facilities in response to customer demand for more suitable solutions despite the lower margins compared to landfilling. Companies are also looking at other initiatives. Republic Services is targeting a 40% increase in recovery of key materials by 2030 versus a 2017 baseline while others are using robotics to sort materials more efficiently.

Historically, European countries had a scarcity of landfills and high energy costs, which forced them to be more circular whereas the U.S. was the exact opposite with massive landfill capacity and cheap energy, the investor said.

The CEO of a plastics recycling firm cited the example of Germany with a population of 80 million, which has promoted Extended Producer Responsibility (EPR) - shifting waste management costs or physical collection from local governments to producers - since 1990. Germany moved from 3% recycling rates to 30% in the span of 10 years, supported by a $2.3 billion investment in consumer education and systems for waste collection.

He added that change in Europe is increasingly being driven by the pull of brand owners demanding that companies

incorporate recycled plastic content into their packaging, as well as the push of stricter regulation.

EU countries will have to measure, report and verify emissions from municipal waste incinerators from 2024, and waste incinerators may be incorporated into the EU emissions trading scheme from 2028 thereby penalising the burning of waste and encouraging firms to recycle as much as possible.

A broader EPR mandate was also proposed as a solution in the U.S. especially if it required large consumer packaged goods companies, like Amazon, to take responsibility for managing the post-consumer stage, in order to help meet national recycling and recovery targets.

One waste sector executive said that EPR combined with ‘minimum recycled content’ requirements - which mandate that packaging companies use at least some reprocessed material - was necessary to force real change in the industry.

The executives also discussed how, for batteries, recycling has become cheaper than new material extraction, driven by supply chain security concerns. The sector also demonstrates differences in recycling motivations – batteries are resource constrained versus plastics which are motivated by landfill diversion. Plastics recycling faces hurdles as reclaimed material costs currently exceed virgin plastic prices.

Other proposed solutions included the motivation of consumers to drive change either by eschewing plastic bottles or by pushing for greener products. One example of the latter is On Running which has a sustainable subscription footwear model that provides the subscriber with a new pair of trainers made from castor beans every six months and recycles the used pair. The footwear company also utilizes recycled content in order to produce the soles of its running shoes.

The investor explained that society may need to change its attitude towards waste infrastructure as more processing plants will have to be built to handle the increase in trash, which brings up the issue of ‘nimby-ism’ from local residents. He encountered the issue over the course of 4 years when looking for a site to build a facility in the U.S. Midwest to handle a hazardous waste stream - electric arc furnace dust.

Ultimately, the push to a more circular economy in waste and recycling will require coordinated efforts from consumers, corporations, investors and governments to enact positive change.