Central Banks | 3 min read June 2026

Economics | 3 min read | May 2024

Asia Economic Monthly: China taps Asian demand

Asia is importing more from but exporting less to China.

Economics | 3 min read | May 2024

Asia is importing more from but exporting less to China.

Asia’s trade relationship with China is undergoing a structural shift. Economies within the region are exporting less to China, due to a slowdown in China-centric processing trade and a moderation of domestic demand. At the same time, Asia is importing more from China. In February 2024, China’s share of Asia’s total imports stood at 21.3%, up from 15% a decade ago. This 6.3 percentage point rise contrasts with a 0.6 percentage point fall in China’s share of Asia’s exports during the same period.

The divergence has caused a sharp deterioration in Asia’s trade balance with China, resulting in a deficit of US$192.6 billion in 2023, down from a surplus of US$24.5 billion in 2013. Seven out of nine Asian economies ran trade deficits with China in 2023.

China’s demand for green metals and chips has benefited Indonesia and Taiwan, respectively. Taiwan continues to run the largest trade surplus with China. Indonesia runs a trade deficit with China, but there has been an improvement in the trend due to a rise in its exports of coal, iron and steel, and nickel to China.

Asia is importing more from China

There are four major reasons why Asia is importing more from China, according to Nomura’s analysis.

Medium-term implications

The trend of Asia exporting less to China while importing more from the country has important medium-term implications.

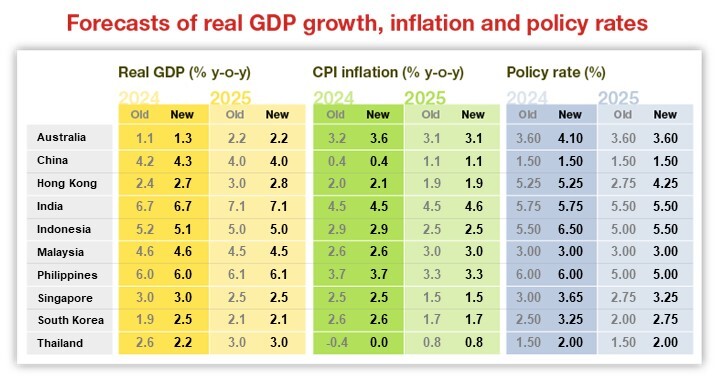

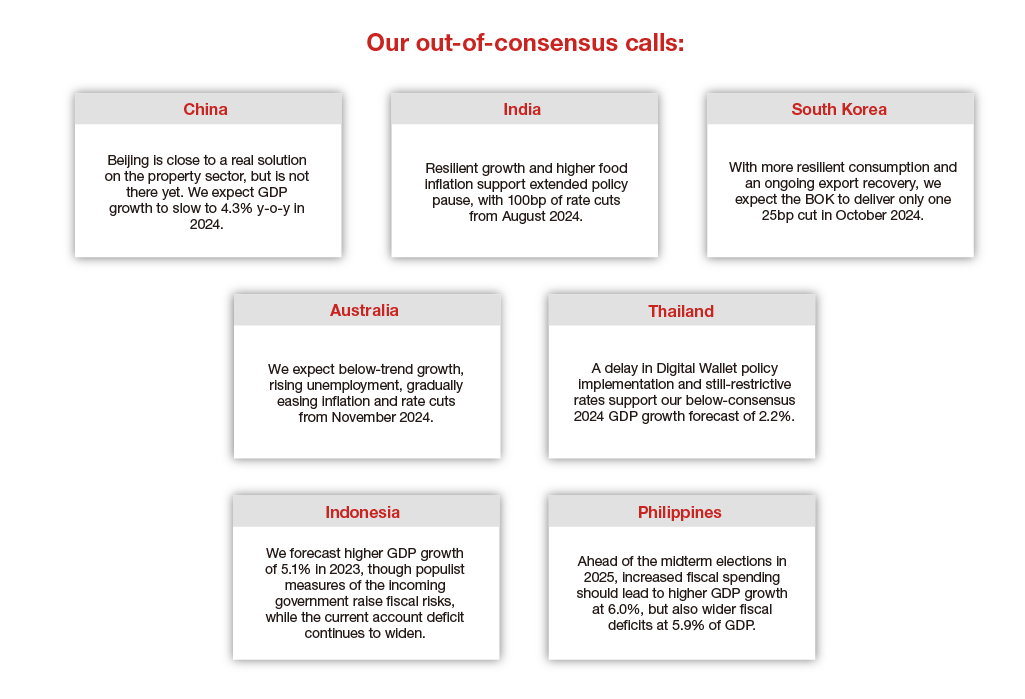

For more on our growth projections, read our full report.

Chief Economist, India and Asia ex-Japan

Economist, Asia ex-Japan

This content has been prepared by Nomura solely for information purposes, and is not an offer to buy or sell or provide (as the case may be) or a solicitation of an offer to buy or sell or enter into any agreement with respect to any security, product, service (including but not limited to investment advisory services) or investment. The opinions expressed in the content do not constitute investment advice and independent advice should be sought where appropriate.The content contains general information only and does not take into account the individual objectives, financial situation or needs of a person. All information, opinions and estimates expressed in the content are current as of the date of publication, are subject to change without notice, and may become outdated over time. To the extent that any materials or investment services on or referred to in the content are construed to be regulated activities under the local laws of any jurisdiction and are made available to persons resident in such jurisdiction, they shall only be made available through appropriately licenced Nomura entities in that jurisdiction or otherwise through Nomura entities that are exempt from applicable licensing and regulatory requirements in that jurisdiction. For more information please go to https://www.nomuraholdings.com/policy/terms.html.

Jump to all insights on Economics

Central Banks | 3 min read June 2026

Economics | 3 min read May 2024

Economics | 3 min read April 2024