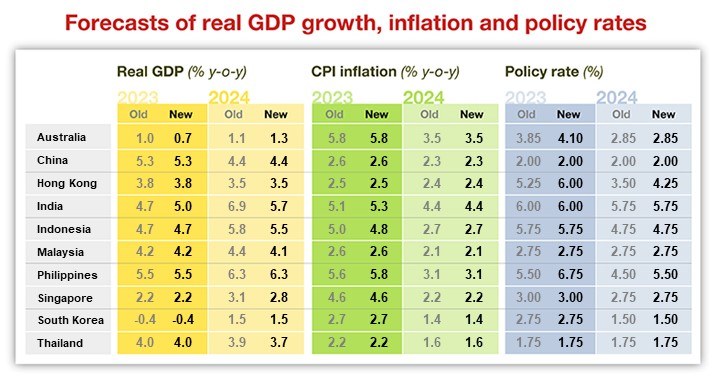

We expect Asia’s growth in the first half of 2023 to be dragged down by the inventory cycle, followed by an uptick in the second half. But behind the scenes, we see final demand slowing as exports outside China and investment demand moderate.

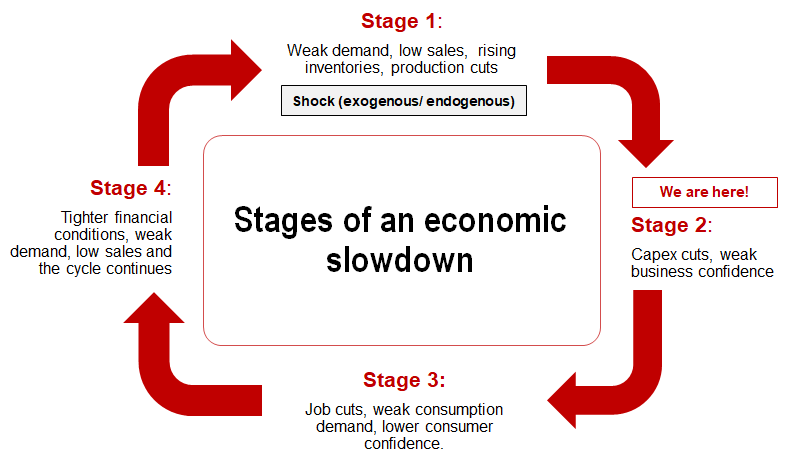

Anatomy of a growth slowdown

An economic slowdown typically occurs in four stages, as per our growth cycle framework. Asian economies are currently experiencing an export slowdown, placing pockets of the region in advanced stage 1 and early stage 2.

Asia’s current growth downturn is a result of exogenous shocks such as semiconductor shortages and subsequent inventory build-up, weak demand from China, high global inflation, and a surge in commodity prices.

This means that, as these fade – China recovery broadens, chip inventories become leaner, and inflation eases, the cycle can turn. However, the full impact of endogenous shocks such as tighter monetary policy on final demand is yet to be seen.

Fixed investment demand has just started to weaken and will moderate throughout 2023. Asia’s exports may see an uptick from improving chip and China demand in the second half of 2023, although part of this growth will be offset by slowing demand from the US and Europe, which are likely to face recessions later in the year. Private consumption demand in Asia should be more resilient but slowing job growth may cause lagged spillover effects.

Weak domestic demand and inventory destocking are both disinflationary, which increases our conviction that both headline and core inflation are set to decelerate sharply in H2 2023 and 2024 across most Asian economies. As a result, we see policy divergence as likely between the Fed and Asian central banks. Despite a higher projected US terminal Fed funds rate, we have only revised up our terminal rate forecast for Philippines’s central bank.

Finally, Asia might shine later than expected as a delayed US recession could be an overhang on Asia for longer. We still believe that Asia is well-positioned to attract more capital inflows due to easing terms of trade, a less negative exports and chip cycle, and medium-term growth drivers for emerging economies such as India and Indonesia.

Divergence among countries will be common

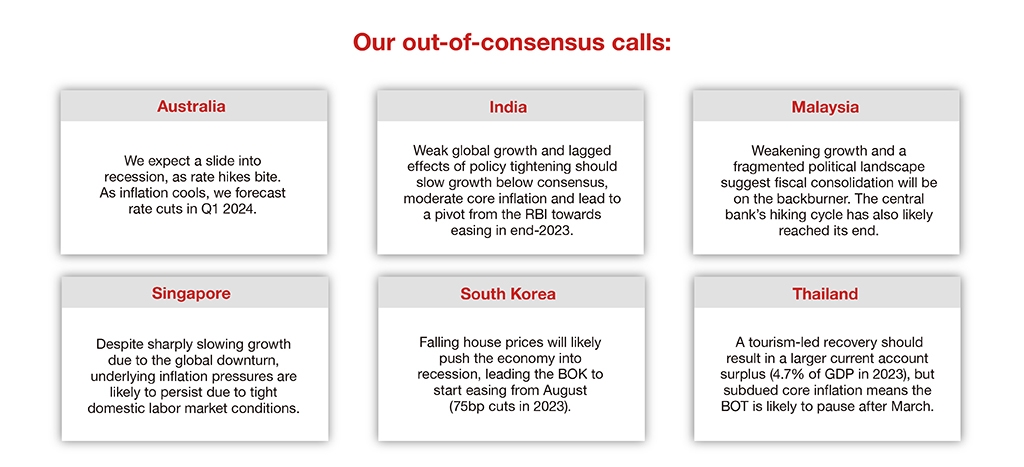

China’s economy has been hit the hardest due to shocks from its zero-Covid strategy and property downturn. Korea has been struggling with the semiconductor downcycle and Singapore is experiencing some economic weakness as a slowdown in exports and the industrial sector spill over into services and discretionary consumption. On the positive side, Thailand’s delayed tourism recovery has propped up its economy with growth firing across most domestic demand engines. Growth in the Philippines also appears resilient despite the steep rate hikes.

For more on our 2023 growth projections, read our full report.