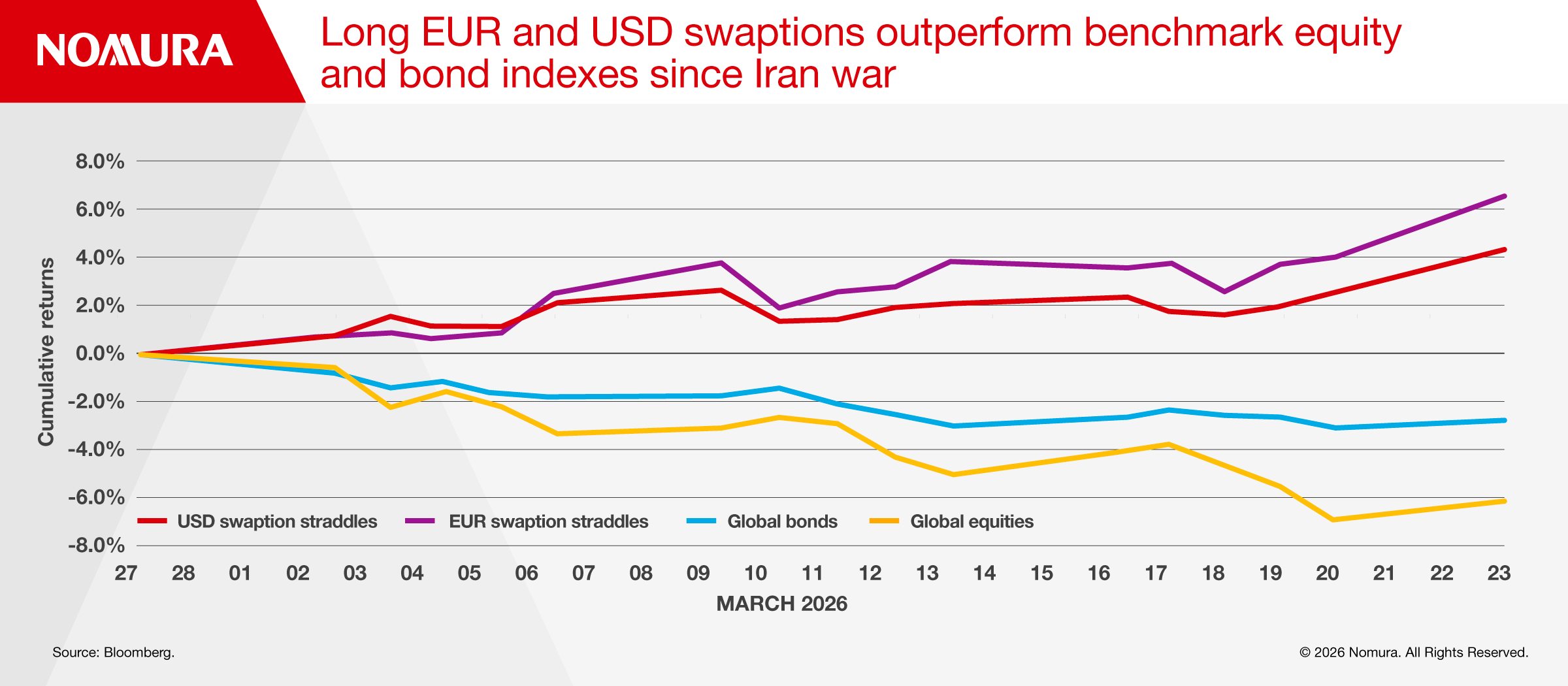

For decades, investors have embraced the asset allocation doctrine that bonds and equities belong together, believing one should work when the other failed, providing mutual diversification. But the Iran war undermines that assumption, as did the inflation shock of 2022, since both bonds and equities experienced drawdowns at the same time.

One strategy that did work in each of these cases was to own a portfolio of long swaption straddles, predominantly using longer expiries and tenors such as 10y10y.

As shown above, both the global equities index and global bonds index fell from February 27, just before the Iran bombing, until March 23. But long positions in EUR and USD swaption straddles made gains.

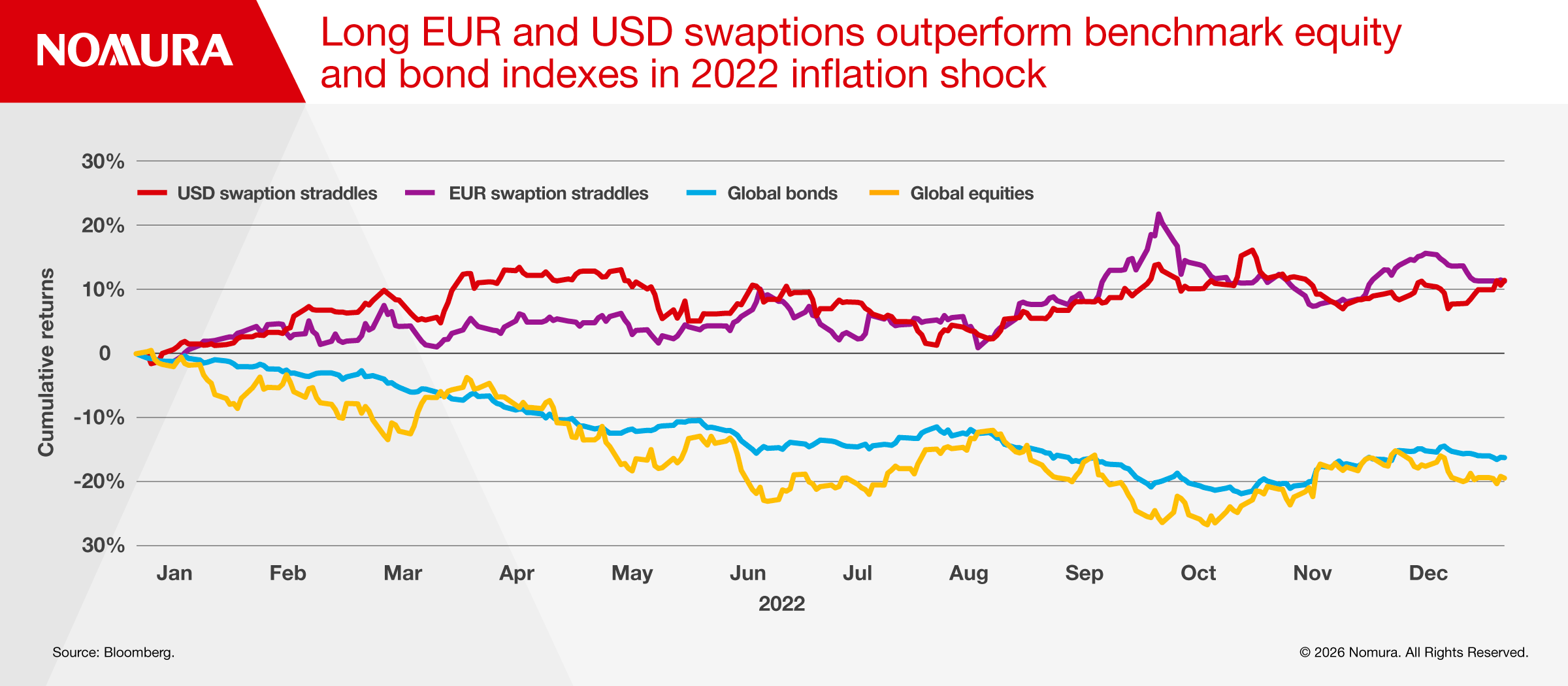

A similar pattern is evident in the inflation shock following Russia’s invasion of Ukraine in February 2022, which exacerbated price pressures from US government stimulus programs.

Tony Morris, Global Head of Quantitative Strategies at Nomura, says that long swaption straddles work when bonds fail for three main reasons:

- A two-way duration bet. Long swaption straddles can profit whether interest rates go up or down. In contrast, bonds only profit if interest rates fall, or stay at similar levels, losing money if they rise. “When a crisis involves inflation fears, as both the Iran war and the 2022 shocks have, interest rates are more likely to rise than fall or stay the same,” says Morris.

- Higher positive convexity. For a given risk exposure, swaptions embed much more positive convexity, “long gamma” in option terms, meaning they benefit from realised volatility in interest rates. While bonds have some positive convexity, it is small relative to total risk and dominated by duration.

- Long implied volatility. In times of crisis, the implied volatility of interest rates tends to rise, as investors bid up swaption prices to achieve protection. Swaption straddles directly benefit from this rise in implied volatility, as they are “long vega” in option terms. Bonds have no direct exposure to implied volatility.

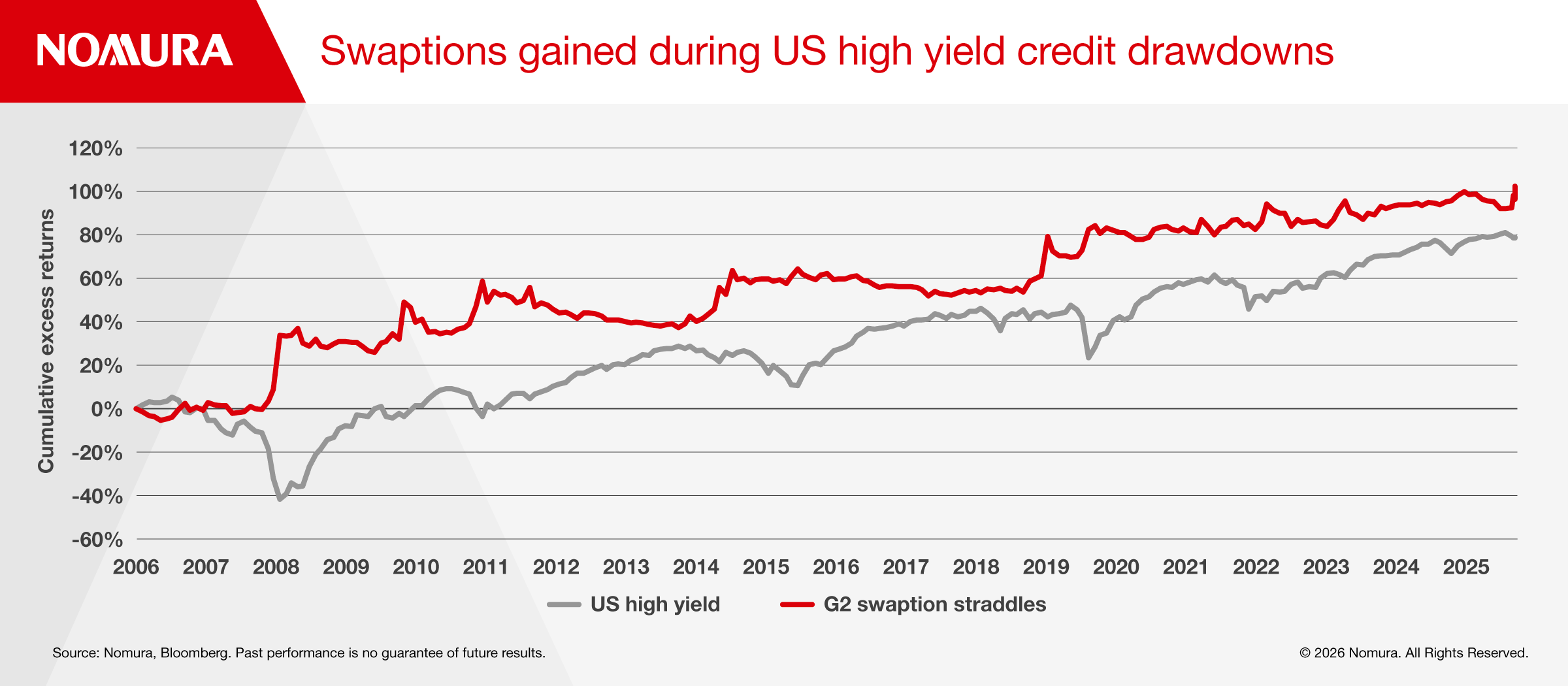

“Not only did long swaption straddles work in these two inflationary shocks, but they also delivered returns during the classic deflationary shocks, when equities and credit suffered drawdowns, but government bonds did well,” says Morris.

A good example of this versatility is the duration-adjusted excess returns (i.e. stripped of cash and interest rate duration) of US high yield corporate bonds. As shown below in gray, high yield credit had major drawdowns on many occasions, including the global financial crisis (2008-9), the Eurozone crisis (2011), the oilpatch crisis (2015-2016), and COVID pandemic (2020). In each of these cases, long positions in swaption straddles (shown in red) surged.

So, what is the connection between swaptions and credit, or corporate risk more generally? It’s certainly true that volatility in interest rates tends to increase at the same time as volatility in equities or credit spreads but there’s more to it than that.

As Robert Merton famously showed in his 1974 paper, a future cash flow with default risk is like a short put option on the asset value of the firm, where the strike price is the level of liabilities over time. This is the essence of the so-called “Merton model” of credit. However, most people learn this model, and option models more generally, assuming that interest rates are constant. Corporate valuation models such as discounted cash flow analysis also typically assume that interest rates are constant

But what if they are not constant, but stochastic – based on random probability? At shorter expiries, for example, below three months, where most of the equity derivatives market trades, it does not matter. At longer horizons, where most of the future cash flows driving credit and equity valuations exist, it matters a lot. Some academic studies estimate 80% of US equity risk derives from cash flows beyond 10 years.

Consequently, interest rate volatility starts to dominate corporate asset volatility as time horizons stretch from months into years.

“As time horizons get longer, what looks like FX, equity or credit risk is actually interest rate risk,” says Morris. “Most portfolios are materially short interest rate volatility, which is problematic during a market downturn, but long positions in swaptions can help.”

Nomura’s Quantitative Strategies team has written a detailed paper about the role of swaption straddles in investment portfolios and Nomura provides investable indices to facilitate access to the swaptions market.

While swaptions have long traded in a narrow circle of current dealers and ex-dealers now at macro or relative value hedge funds, and a few asset managers, the product is gaining wider appeal as an effective hedge when markets swing in unpredictable ways.

“We see investors adding strategic exposure to longer-expiry interest rate swaptions to hedge choppy markets," says Steven Loeys, Head of Macro QIS Structuring at Nomura. "They also see that longer-expiry straddles in swaptions have much less negative carry – cost of holding the position - than straddles in other asset classes, such as bond futures or equities, which are only liquid at shorter expiries.”

For more information about this topic please contact Anthony Morris or Steven Loeys.

Disclaimer

This content has been prepared by Nomura solely for information purposes, and is not an offer to buy or sell or provide (as the case may be) or a solicitation of an offer to buy or sell or enter into any agreement with respect to any security, product, service (including but not limited to investment advisory services) or investment. The opinions expressed in the content do not constitute investment advice and independent advice should be sought where appropriate.The content contains general information only and does not take into account the individual objectives, financial situation or needs of a person. All information, opinions and estimates expressed in the content are current as of the date of publication, are subject to change without notice, and may become outdated over time. To the extent that any materials or investment services on or referred to in the content are construed to be regulated activities under the local laws of any jurisdiction and are made available to persons resident in such jurisdiction, they shall only be made available through appropriately licenced Nomura entities in that jurisdiction or otherwise through Nomura entities that are exempt from applicable licensing and regulatory requirements in that jurisdiction.

To read the full disclaimer, please click here.

For more information please go to https://www.nomuraholdings.com/policy/terms.html