The closure of the Strait of Hormuz is now in its third month. Pipeline price pressures due to supply chain disruptions are visible, but physical supply disruptions across Asia have been less than feared. We believe this resilience is due to a mix of factors: depletion of strategic petroleum reserves, buffers from floating storage and in-transit oil, activation of alternate energy sources (coal) and countries sourcing energy from alternate routes at higher prices.

Hopes of a US-Iran deal are rising again, but the longer the Strait of Hormuz remains closed, the faster the existing buffers could still be depleted; so even as we have been surprised with Asia’s resilience, we remain vigilant.

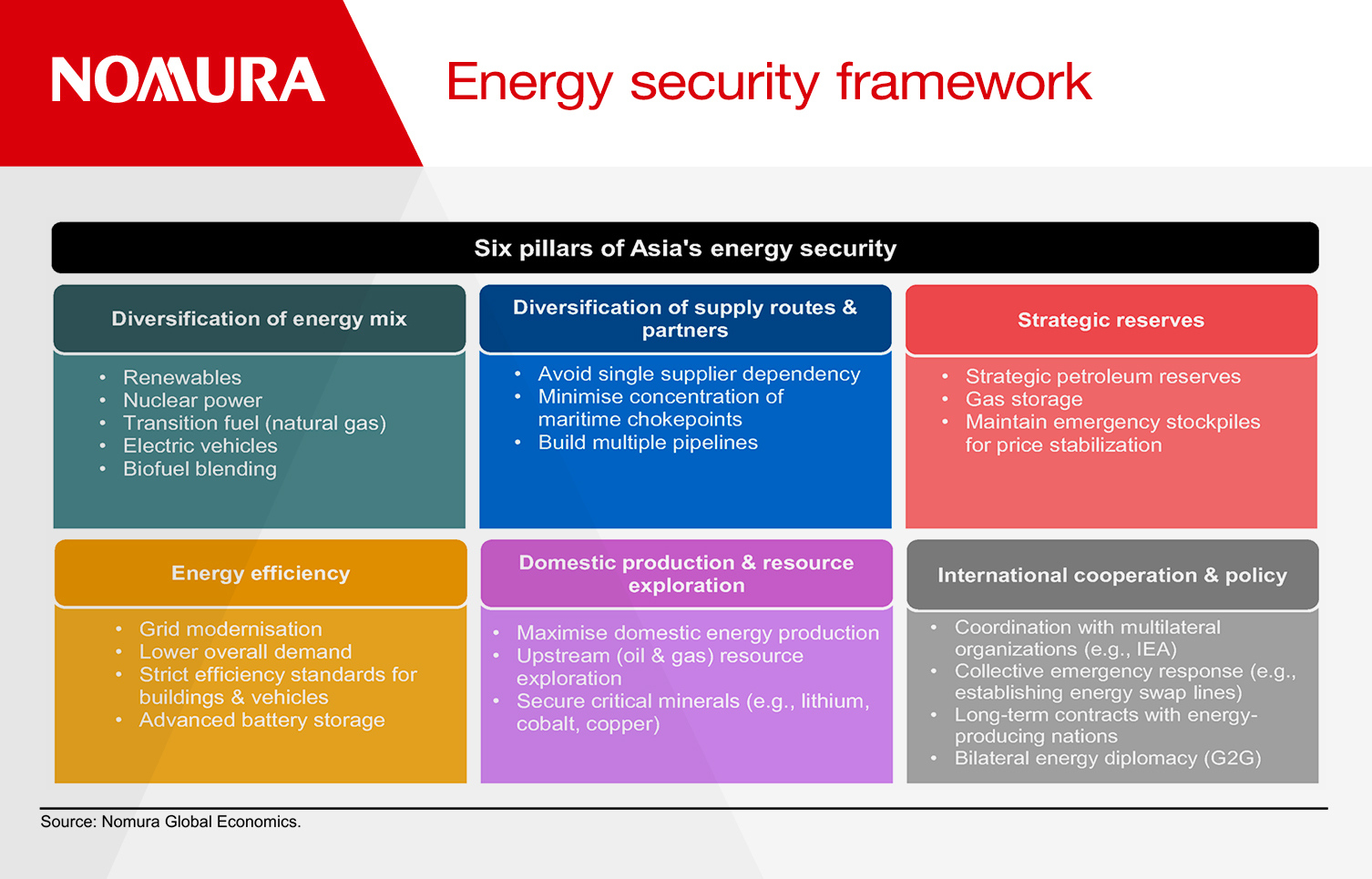

Six pillars of Asia’s energy security

Beyond the impact on near-term supply, the Middle East conflict has galvanized Asia’s focus on medium-term energy security. In our view, there are six primary pillars of energy security. We use five of these pillars to create Nomura’s Asia Energy Security Index (NAESI), a measure of how prepared Asia is on energy security.

Diversification of the energy mix

Boosting resilience means reducing the reliance on a single source of energy and imported fossil fuels, increasing the share of renewable and nuclear energy in the energy mix and diversifying transport energy sources.

We find wide variations across Asia. Most Asian economies depend heavily on fossil fuels and imported energy, though China, India and Vietnam can switch to domestic coal. New Zealand and the Philippines have high renewable shares but are dependent on imported petroleum products. EV penetration in Singapore is high, but it is a large net oil and gas importer. Japan, India and Malaysia lag in EV penetration, while South Korea’s nuclear capacity leads the pack. Each economy faces distinct energy chokepoints.

Diversification of supply sources

Countries can reduce concentration risk by sourcing energy from multiple partners, securing various maritime routes and building multiple pipelines. It is crucial for Asian economies to diversify their supply sources, as most of them now source 60-99% from Asia and the Middle East combined. New Zealand and Australia are particularly exposed to supply disruptions in Asia, as they source over 90% of their refined fuel from the region.

Strategic reserves and storage

To cushion against unanticipated supply shocks, countries need to maintain sufficient physical stockpiles of crude oil and expand LNG storage capacity. Oil reserves are much higher in Northeast Asian economies and significantly lower in South/Southeast Asia. Lower gas storage is a security risk for many Asian economies and likely reflects technical barriers and higher capital costs.

Improve energy efficiency

This can be done by reducing the energy intensity of the economy through grid modernization, implementing stricter efficiency standards and using energy storage systems such as advanced batteries. China has made the most effort in these aspects, while Japan, South Korea and Singapore also rank highly on advanced smart grid deployment and efficiency standards. India and the rest of ASEAN, on the other hand, still face significant gaps on grid modernization.

Boosting domestic production and resource exploration

According to the United States Geological Survey, Asia Pacific holds 12% of the world's oil and gas resources, comprising an estimated 10.5 billion barrels of undiscovered oil and 271.5 trillion cubic feet (Tcf) of gas. Major holders of proven and probable oil and gas reserves in the region include Malaysia, China and Australia. Countries also need to secure critical minerals, such as lithium, cobalt and copper, which are essential for a green energy transition.

International cooperation

Countries can enhance energy security through multiple strategic channels: bilateral long-term supply agreements, government-to-government energy diplomacy, coordination with multilateral agencies and engagement with regional energy frameworks.

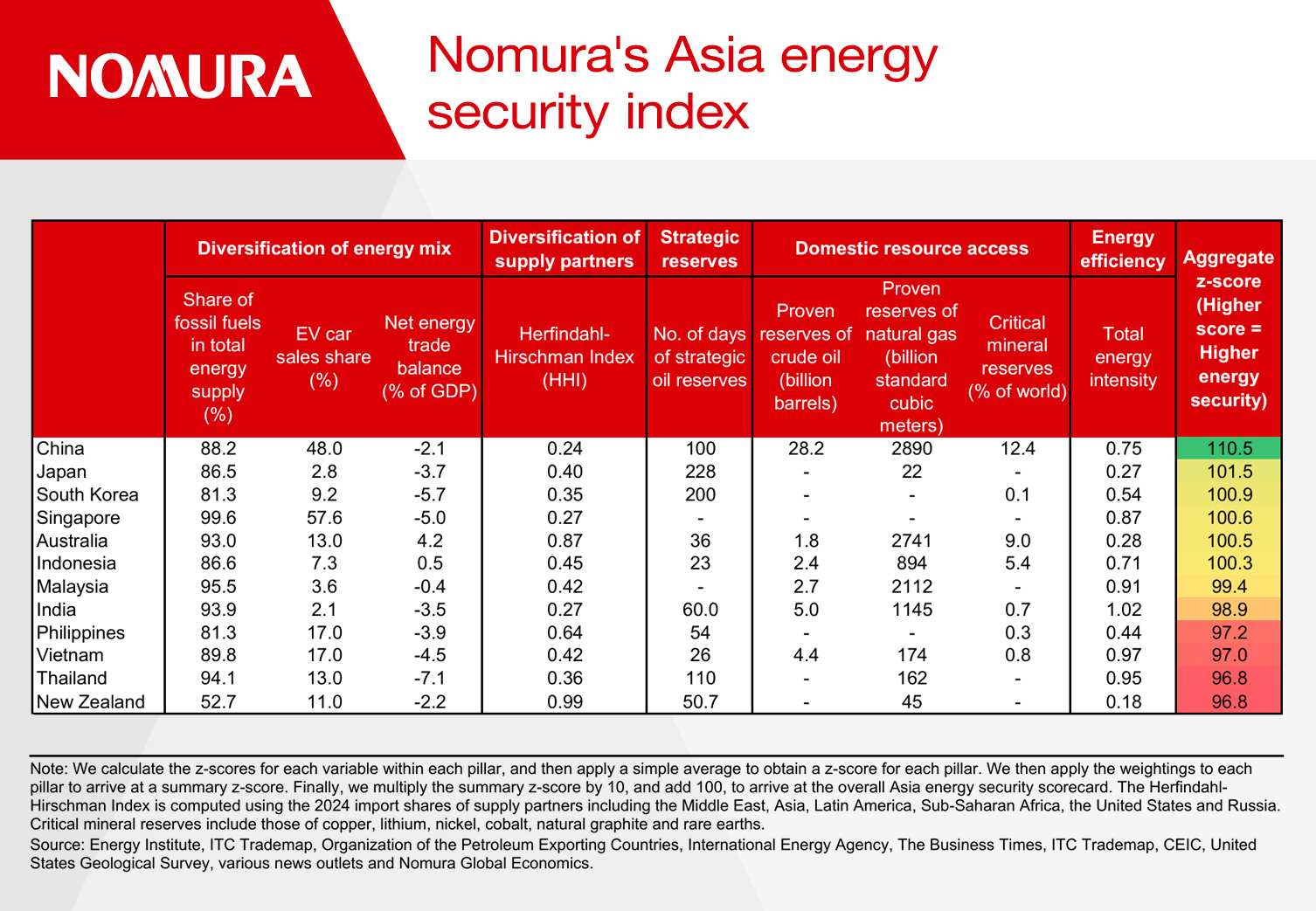

Nomura’s Asia Energy Security Index

To quantitatively estimate where Asian economies stand on their energy security, we aggregate five of the six pillars (excluding international cooperation) into a combined scorecard. Our results show that energy security varies widely across the region.

China has the highest energy security score on our index, reflecting its concerted effort over multiple years to diversify its energy mix, maintain leadership in renewables and EVs and secure a wide range of energy suppliers. Moreover, China is resource-rich, with the highest proven reserves of crude oil, natural gas and critical minerals within the region.

At the other end of the spectrum, New Zealand and Thailand rank among the lowest on our index. New Zealand has a high concentration of energy supply partners and a lack of proven crude oil and critical mineral reserves, while Thailand is heavily reliant on imported oil and gas, and has low energy efficiency.

Most other Asian economies rank in the middle, with the aggregate variation between them rather small. However, their individual energy chokepoints differ.

How Asia is planning to boost its energy security

Asian policymakers are determined to improve their medium-term energy security. Our analysis of the ongoing developments suggests some key themes across countries.

Diversification: Diversification is a common goal among policymakers, in terms of energy mix and sources of energy supply. China’s 15th Five-Year Plan sets a target of 25% non-fossil energy in primary consumption by 2030, while South Korea has unveiled an accelerated roadmap aiming for renewables to generate 20% of its electricity by the same year.

Asia’s nuclear ambitions are on the rise. South Korea is bringing back its offline reactor units, India has announced a ten-fold expansion of its nuclear power capacity by 2047, and Malaysia is now studying nuclear energy as a long-term option.

Countries are actively trying to pivot away from Middle Eastern energy dependence by diversifying their supplier base, contracting new oil and gas supplies from the US, Australia, Latin America and West Africa.

Strategic reserves, storage and domestic exploration: Across the region, countries are expanding their energy storage infrastructure. China's emphasis on self-sufficiency in core oil and gas demand signals further expansion of its strategic oil reserves. India is also actively considering boosting its strategic petroleum reserves, with its largest LNG importer having announced plans to build seven new storage facilities.

Boosting domestic output remains equally critical. India has launched "Samudra Manthan," a national deepwater exploration mission designed to discover new resources and strengthen the country's hydrocarbon reserves.

Regional cooperation: Signs of growing regional cooperation are emerging. The energy shock has significantly accelerated the ASEAN Power Grid initiative, enabling member states to share renewable resources and reduce dependence on imported fossil fuels. During the Australian Prime Minister's recent visit to ASEAN, Malaysia committed to prioritizing excess fuel supplies to Australia, while Australia reaffirmed continued LNG exports to Malaysia under existing agreements – a clear example of reciprocal energy security arrangements.

Investment and export opportunities

Investment spending is on the rise across countries, targeting oil and gas exploration, renewable energy, nuclear reactor projects, energy storage and smart grid infrastructure, driven by traditional energy security concerns and the rise in power demand from AI data centers.

We also see significant export opportunities emerging from the global focus on energy security. Demand for green technologies – including electric vehicles, solar panels and battery systems – is rising, with Asia well-positioned to capitalize on this trend.

China commands a 40% market share in global green tech exports, while Thailand, Malaysia, Vietnam and India are emerging as significant players in solar panel exports. South Korea and Japan hold dominant positions in the export market for advanced lithium-ion batteries, with the former also positioning its Small Modular Reactors strategy around its manufacturing strengths.

Global efforts to diversify energy supply sources should boost LNG exports from Malaysia and Australia, while China, Indonesia and Australia also stand to benefit from surging demand for nickel and rare earth minerals.

Beyond the ongoing Middle East conflict, Asia’s focus on medium-term energy security presents significant opportunities ahead, in our view.

To read our full report, click here.