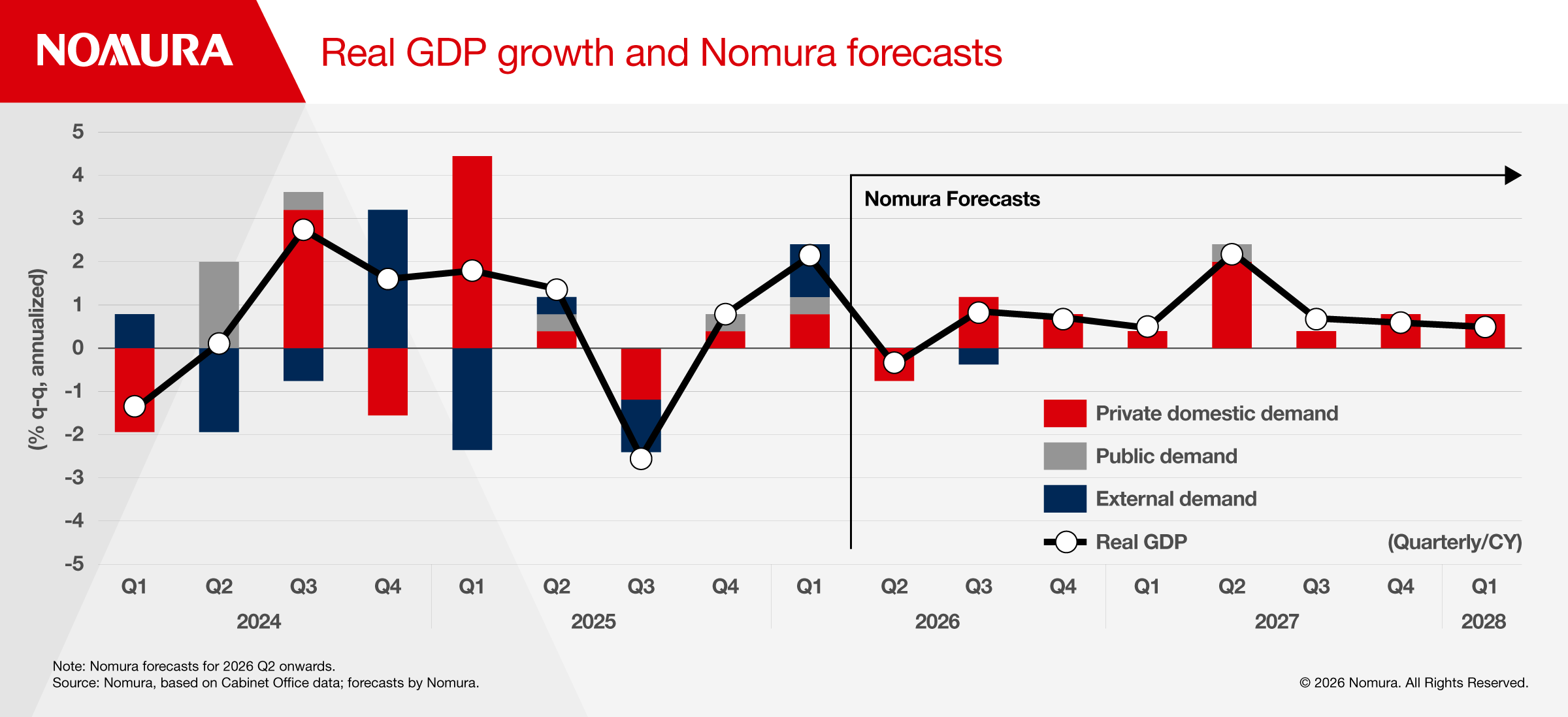

On May 19, Japan’s Cabinet Office announced the preliminary GDP estimates for the first quarter of 2026: Real GDP growth came in at +2.1% versus the previous quarter, above the consensus forecast. But this does not help us gauge the outlook for the Japanese economy because the Iran war has created so much uncertainty in the global economy.

We lay out our main scenario for the Japanese economy based on our current assumptions, plus five ways the Middle East conflict could affect Japan’s economy.

The main scenario: Japan’s moderate economic recovery continues at a slower pace

We assume that the de facto blockade of the Strait of Hormuz and tensions in the Middle East will ease. We expect the price of North Sea Brent crude to fall from $126.7 per barrel at the end of FY2025 to $84.3 per barrel by the end of FY2026 and to $76.9 per barrel by the end of FY2027, broadly in line with the futures curve.

We also assume that there will be a moderate decline in USD/JPY from ¥159.80 at the end of FY 2025 to ¥150 at the end of FY2026 and ¥145 at the end of FY2027.

Based on these assumptions, we now forecast real GDP growth of +0.5% year on year for FY2026 (down from +0.9%) and +1.0% for FY2027, versus +0.8% for FY2025. Even in our revised forecasts, we still expect the moderate economic recovery to continue.

That said, there will likely be some bumps along the way. In the current April to June quarter, we estimate that real GDP will fall quarter-on-quarter (0.5%) for the first time in three quarters (Figure 1).

We expect real GDP to return to positive territory in the July to September quarter with a rise of +0.9% q-o-q annualized. We assume the impact of the closure of the Strait of Hormuz will start to ease in the July to September quarter but production activity in Japan would take time to return to normal so the economy would likely remain sluggish.

Domestic production and exports should rise in the October to December quarter assuming that the impact of the Middle East conflict will ease further. However, as CPI rises at a lag, real disposable income — an indicator of households’ purchasing power — is more likely to decline heading into Oct–Dec, so consumer spending will most likely slow in that period.

Five ways the Japanese economy could be affected

Tensions in the Middle East pose a number of risks for the Japanese economy. We focus on five ways the situation in the Middle East could affect the Japanese economy:

- Price-related supply constraints

- Quantitative supply constraints

- Constraints on exports as a result of logistical disruptions

- Impact on exports from overseas economies

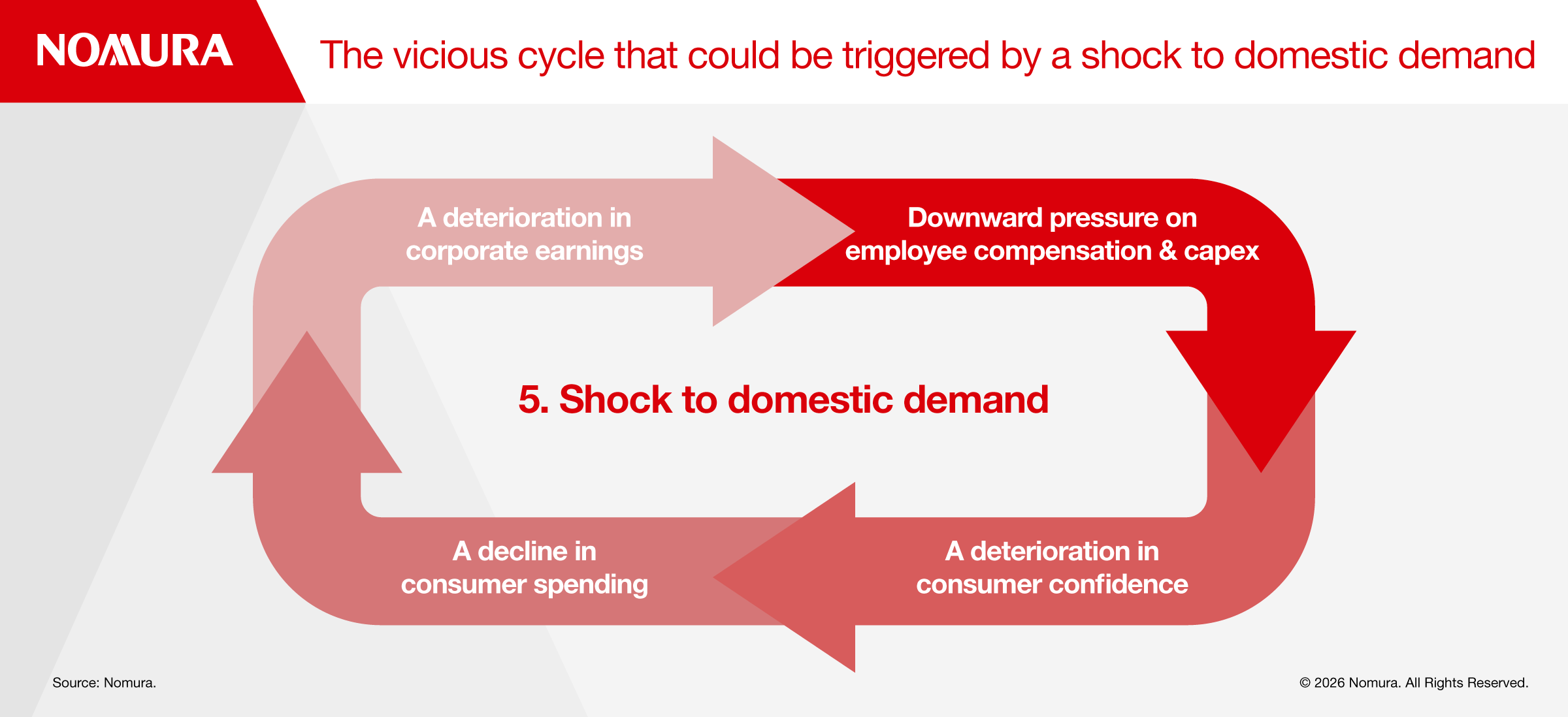

- Domestic demand shock

Of these, a domestic demand shock is the most serious but least likely. If it happened, it would be more difficult for the BOJ to hike interest rates.

Price-related supply constraints

For companies, the deterioration of trade — with higher crude oil prices leading to higher export and import prices — is likely to exert downward pressure on corporate earnings and production activity. For households, rising prices could dent real wages and crimp spending.

Quantitative supply constraints

Regardless of prices, the inability to procure energy and raw materials in sufficient quantities will result in lower capacity utilization at plants, which will then gradually spread downstream. This could make it difficult for households to procure some consumer goods.

Constraints on exports as a result of logistical disruptions

While there is demand for products and production is possible, logistics constraints will make it impossible to export goods. An example is the decline in automobile exports to the Middle East.

Impact on exports from overseas economies

Amid heightened tensions in the Middle East, Japan is not the only place where production activity is being hampered. As a result, Japan’s exports to a wide range of countries and regions other than the Middle East may be curtailed.

Domestic demand shock

A shock to domestic demand would have the greatest impact on Japan’s economy. If price-related or quantitative supply constraints result in lower capacity utilization in Japan and lower-than-expected earnings, companies could rein in or postpone capex. At the same time, if companies were to rein in hiring and wage hikes, households would become increasingly frugal. This would raise the prospect of weakened consumer spending, triggering a vicious cycle (Figure 2).

The Japanese economy is already seeing price-related and quantitative supply constraints as well as constraints on exports as a result of logistical disruptions. However, as long as the blockade of the Strait of Hormuz starts to ease, we think the Japanese economy will be able to avoid a drop in exports and a domestic demand shock.

To read the full report, click here.