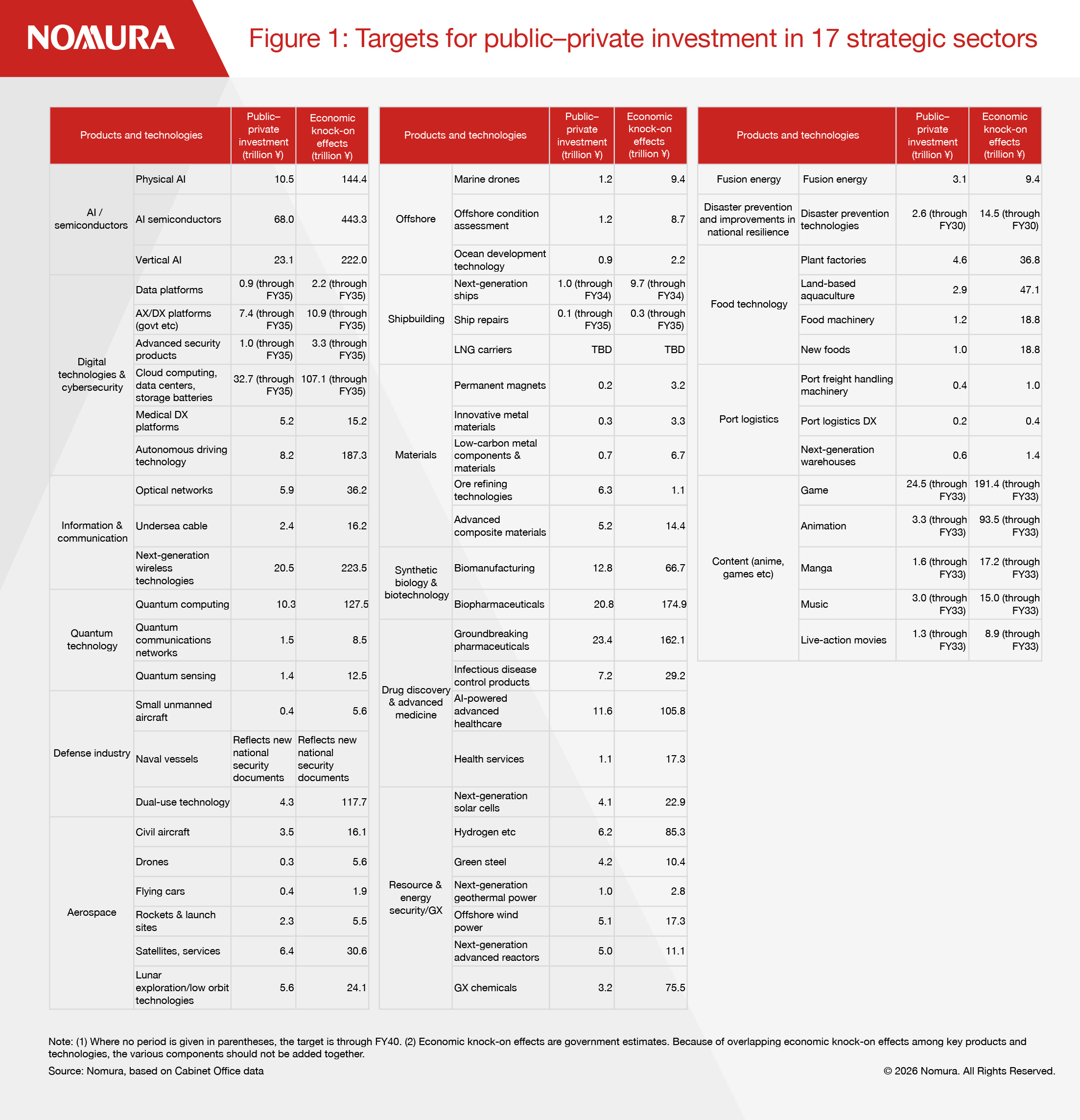

The first growth strategy of the Takaichi administration was unveiled on June 24. It calls for over ¥370 trillion ($2.3 trillion) in public–private investment through FY2040 (Figure 1). The target areas of these investments are in crisis management and growth, covering key products and technologies across 17 strategic sectors, including defense, digital technologies & cybersecurity, quantum technology, resource & energy security, and shipbuilding.

The figure is particularly high for investment in AI and semiconductors — including physical AI, AI semiconductors, and vertical AI — at ¥101.6 trillion. The Takaichi administration is expressing a clear commitment to prioritizing support for this area.

However, there are still many unknowns, including the breakdown of public-sector and private-sector investments and how the new scheme will fit with existing industry support policies.

Three economic scenarios

The growth strategy includes longer-term fiscal projections. It presents three scenarios based on the extent to which additional fiscal spending could stimulate private-sector investment in addition to demand.

In scenario 1, high growth is realized. Scenario 2 reflects a lower level of growth. And scenario 3 is a continuation of the status quo. These scenarios assume additional fiscal spending of ¥10 trillion in real terms from FY2027 onwards, increasing in line with growth in prices and wages.

In scenario 1, which assumes the strongest impact from the growth strategy, nominal capex at Japanese companies rises from ¥125 trillion in FY2025 to around ¥230 trillion by FY2040, and nominal GDP rises from ¥669 trillion to around ¥1,100 trillion. In addition to increased demand through growth investments, this scenario assumes there will be an increase in economic supply capacity as R&D investments and resource allocation become more efficient.

In contrast, scenario 3 assumes the lowest growth. It is a continuation of the status quo where the only boost to demand is from additional fiscal spending, and private-sector investment is in line with past trends. Capex comes to only around ¥170 trillion and nominal GDP to only around ¥900 trillion by FY2040.

The public–private investment roadmap identifies bottlenecks in each sector and sets out measures to be taken. But even if these are implemented, it is unclear whether this would result in the high-growth scenario. For scenario 1 to be realized, the government will need to provide more convincing explanations for how this will be achieved to persuade companies, markets, and other relevant parties.

Establishing the “strong and prosperous Japan” investment framework

On June 24, Prime Minister Sanae Takaichi also announced that she intends to set up an investment framework for “a strong and prosperous Japan” in the initial general account budget for FY2027.

The investment framework is described as having three major characteristics:

- no upper limit on budget requests from government ministries and agencies

- funding allocated based on plans spanning multiple years

- ensuring adequate scale while being mindful of fiscal sustainability

Considering the first of these, the Takaichi administration has been moving toward a more selective approach to budget allocation, emphasizing the 17 strategic sectors while reviewing subsidies and special tax measures. We expect the disparity between priority and non-priority areas in the budget to become even more pronounced.

For the second, the government’s introduction of multi-year support measures should create a more predictable environment for private-sector companies when making investment decisions.

Regarding the third, Takaichi has highlighted fiscal sustainability as part of her fiscal stance. However, the longer-term projections indicate that, in order to achieve the target of steadily reducing the debt-to-GDP ratio, the growth strategy will need to deliver an impact close to the maximum of the assumed range. Scenario 1 is the only scenario where the debt-to-GDP ratio continues to decline during the period covered by the longer-term projections (through FY2040).

Is longer-term fiscal sustainability possible?

Under LDP rules, the Takaichi administration could remain in power until 2036. To ensure longer-term fiscal sustainability beyond the maximum term of office, the administration will need to demonstrate that such a high level of growth is credible.

To read the full report, click here.