Updates to Japan’s Corporate Governance Code are moving forward under the Takaichi administration, and we expect they will have a major impact on the Japanese economy and corporate sector over the longer term.

Companies are under growing pressure to make efficient use of cash and deposits. We anticipate the corporate sector will increase its spending on investments, M&A, and shareholder returns.

More efficient uses for cash and deposits

In March 2023, the Tokyo Stock Exchange (TSE) issued a document asking companies to be more efficient in their use of capital. Three years on, the March 2026 Reuters Corporate Survey revealed that around 50% of the 216 respondents said the TSE’s requests were appropriate, and many added that they had led to increased awareness of governance and capital efficiency. However, 20% of companies said that they were leading to negative side effects, and 17% said they were not appropriate, with some companies mentioning an excessively short-term focus on share price and investors, as well as the emergence of activist investors.

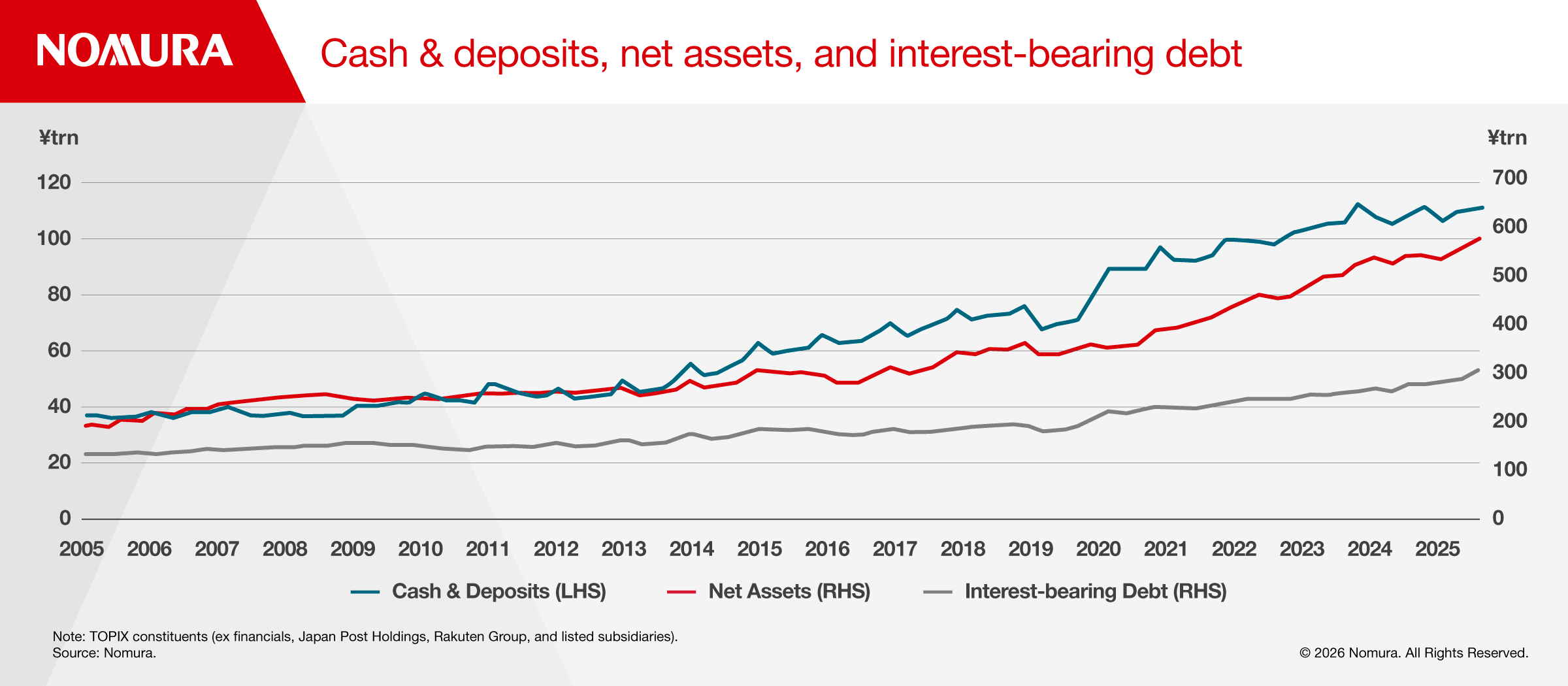

This ambivalence to the TSE’s requests is epitomized by listed Japanese companies’ cash and deposits, which were broadly flat at around ¥110 trillion as of December 2025 (Figure 1). As a percentage of total assets, they have fallen slightly, but they remain above 10% at Japanese companies, higher than in Europe (between 7% and 8%) and the US (around 6%).

While it may have been possible to justify holding cash and deposits under deflationary conditions, in an inflationary environment, excessive cash and deposits will lead to a deterioration in asset efficiency.

For the ratio of cash and deposits to total assets to reach the same level as in the US and Europe, companies would need to use ¥30 trillion to ¥40 trillion to fund capex, M&A, and shareholder returns. If that happens, the impact on the market would be considerable. The roughly 50% of listed Japanese companies that have been skeptical about the TSE’s requests would step up efforts to improve capital efficiency.

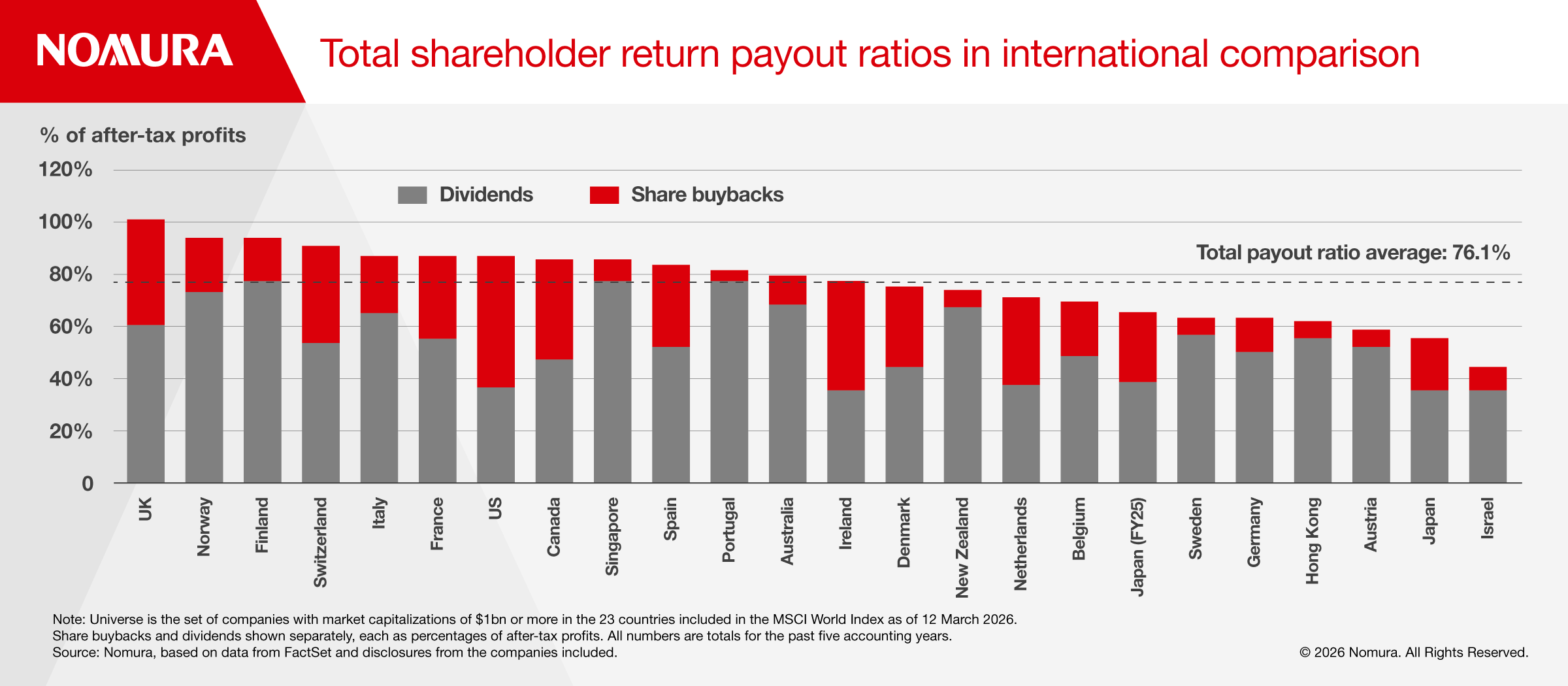

In FY2025/26, the share buyback ratio in Japan was 26.8%, above the international average of 21.8%. But the dividend payout ratio was 37.6%, well below the international average of 54.3%. The total payout ratio of 64.4% was also more than 10 percentage points below the international average of 76.1% (Figure 2). Total payout ratios at Japanese companies still have scope to catch up with global standards.

It is hardly surprising, then, that the focus of revisions to the Corporate Governance Code, due for release in mid-2026, will be on the effective use of cash and deposits. We expect that companies’ medium-term business plans will increasingly include views on optimal capital structure as well as cash allocation over the next few years.

Raising ROE

Return on equity (ROE) in Japan has been below 10% for a long time, which is lower than in the West. Some observers expect ROE to improve to around 11% to 12%, potentially putting it on par with Europe. However, even if the total payout ratio were to remain at its current level of around 70%, we estimate that ROE would only come in at around the mid-11% level by FY2029.

The disparity in ROE between Japan and the US is due to multiple factors, three of which are particularly significant: asset turnover, leverage, and large disparity in margins. Of these, leverage has been on a downward trajectory in Japan, the US, and Europe, suggesting that the buildup of capital as a result of profit growth has exerted downward pressure on ROE, which in turn explains the high total payout ratios shown in Figure 2.

One way for Japanese companies to improve their ROE would be to enhance asset turnover and increase leverage by overhauling their capital structures, which is why it makes sense for revisions to the Corporate Governance Code to call on companies to think about effective use of cash and deposits. However, we think global investors will continue to demand radical overhaul of business portfolios, including growth investment in high-margin areas and downsizing of unprofitable businesses.

Over the past few years, marked labor shortages in the Japanese economy have encouraged companies to restructure their businesses. We think many more companies will be able to improve profitability simply by halting unprofitable businesses amid labor shortages. Value-added per worker and recurring margins tend to improve when labor shortages worsen, suggesting that labor shortages have been prompting companies into reviewing inefficiencies and raising prices. We estimate that separating out low-margin businesses with pretax return on assets of less than 3% would boost overall ROE by around 2.6%.

This kind of earnings improvement process has already started, particularly in B2B sectors such as capital goods and parts, information services, and construction, and we expect it to continue through 2026.

To read the full report, click here.