Japan’s Economy Wakes Up as Alarm Clocks Trigger Growth Boost

We previously explored the major events that led to a decades-long deflationary spiral in Japan. Here, we lay out how Japan’s economy can wake from its slumber by focusing on four main themes, (1) human resources strategy; (2) software investment; (3) entrenching a price-hiking culture; and (4) governance reforms.

Potential improvement in profit margins at Japanese corporations caused by the end to deflation

Revising prices like European companies have done, could mean roughly 40% improvement in margins

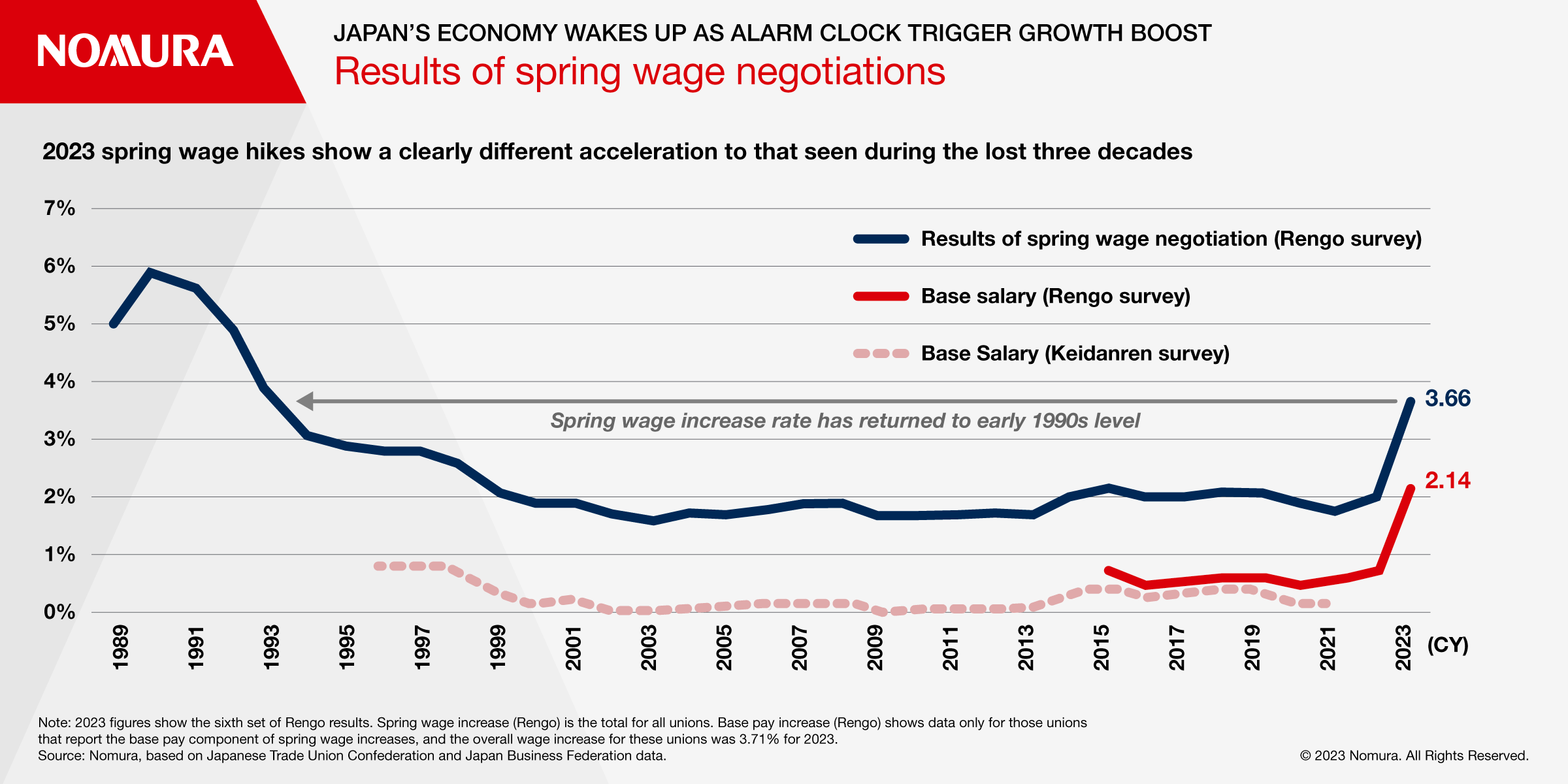

2023 spring wage negotiations are a symbolic structural change in the Japanese economy

With equity markets taking centre stage, investors are watching closely to see whether the Japanese economy, and Japanese corporations in particular, will at long last be roused.

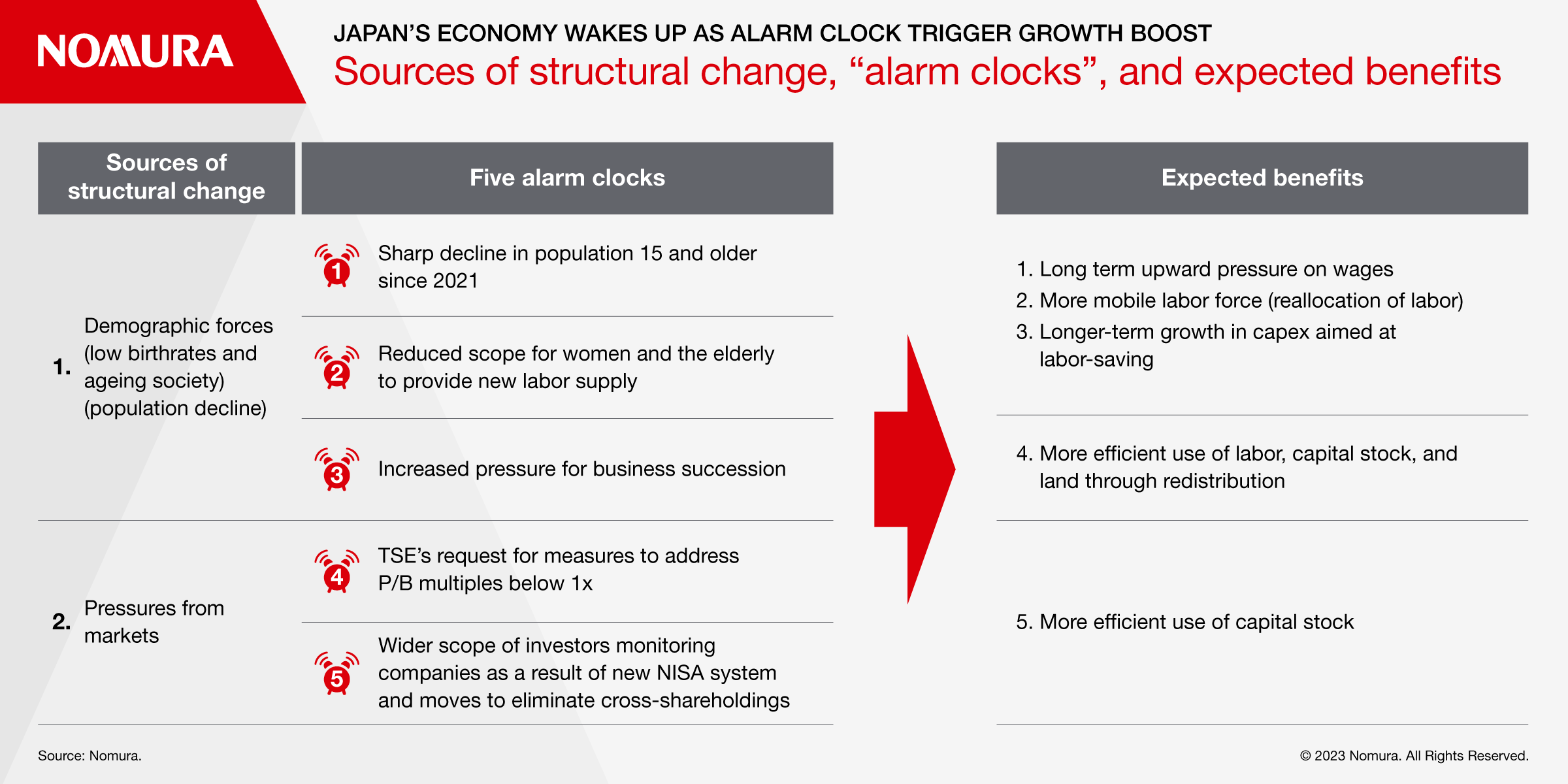

We hear five “alarm clocks” now ringing for Japan’s economy, resulting from two sources of structural change: demographics and market pressures.

If the blaring of these alarm clocks successfully wakes up Japan, we think Japan could overcome its labor shortage, thereby bringing about a wider range of growth opportunities making better use of companies’ capital stock, technologies, and skills.

Figure 1: Sources of structural change, “alarm clocks”, and expected benefits

CHANGES IN HUMAN RESOURCE STRATEGIES

The ‘shunto’ spring wage hikes reached their highest level in nearly 30 years as a result of factors including post pandemic tighter supply-demand, the rise in energy and food prices caused by the Ukraine conflict, and the sharp depreciation in JPY versus USD stemming mainly from rate hikes by the US Federal Reserve, making them the most symbolic qualitative change in the Japanese economy that we have observed.

However, as none of these is likely to result in sustained upward pressure on wages, we cannot rule out the possibility that the 2024 spring wage negotiations will end in a major slowdown in wage growth.

Having said that, Japan’s precarious demographics may lend a hand. Japan’s overall population peaked around 2008 and has been heading downward since. With the working-age population aged 15 and older declining rapidly and lower prospects for women and the elderly joining the labor force, so long as this decline in Japan’s population is a continuing phenomenon, we expect continued upward pressure on wages.

SIGNS OF HEIGHTENING ACTIVITY IN THE CAREER CHANGE MARKET

Even with the traditional lifetime employment model collapsing over the course of the lost three decades, the career change market had remained subdued as it was seen as a place for people to reactively search for new jobs out of necessity, and many workers changing jobs even saw declines in their earnings. Since around 2020, the number of currently employed people looking to switch jobs has been clearly increasing. This could put pressure on Japanese companies’ rigid hiring practices.

In terms of labor supply, we think these pressures could promote reallocation of labor through greater labor force mobility (improved labor market liquidity). Moreover, if labor market liquidity were to improve, this could help speed up corporate business reforms too.

Figure 2: Results of spring wage negotiations

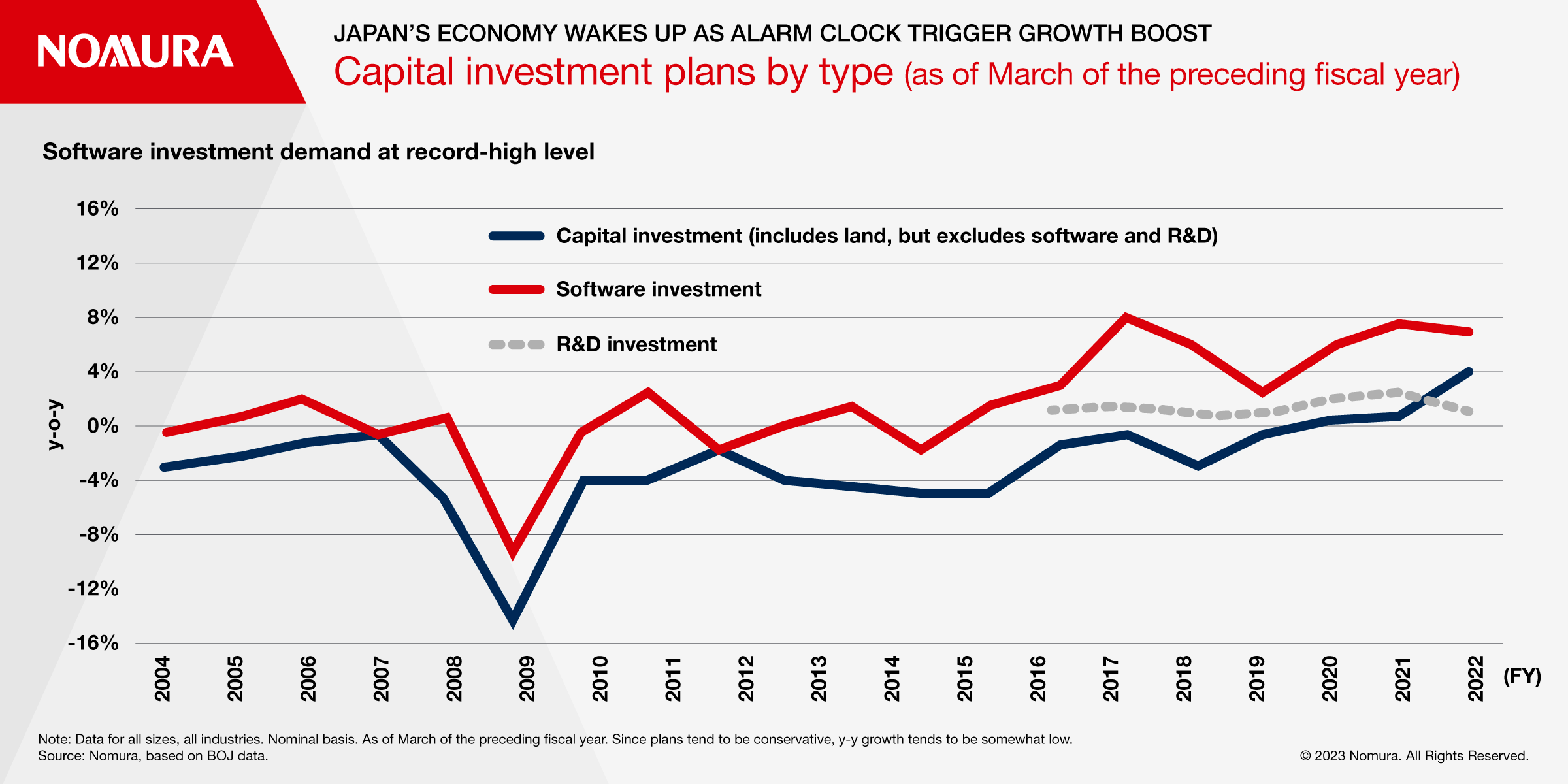

SOFTWARE INVESTMENT ENTERING A NEW PHASE

Capital investment slowed during Japan’s three “lost decades”.

However, the worsening labor shortage is pressing companies to improve productivity. Japanese companies embarked on capex spending from the 2010s to implement DX and cope with personnel shortages, and we are now seeing some resultant breakthroughs.

STRUCTURAL STRENGTH OF IT INVESTMENT DEMAND LIKELY TO BOLSTER EARNINGS

System integrators are helping medium-sized and major companies improve productivity and increase sales, while SaaS companies are monetizing moves by SMEs to reduce operating expenses.

A survey of FY23 capex plans conducted in March 2023, based on plans for the coming fiscal year, revealed that software investment should continue to grow at a record pace, while capital investment (including land, excluding software and R&D) should also increase.

Figure 3: Capital investment plans by type (as of March of the preceding fiscal year)

We think this indicates that corporate capex demand is strong. We think the reopening of the economy following the COVID-19 crisis will result in the emergence of pushed-back capex demand, especially from the non-manufacturing sector.

Investment in IT systems in front-facing fields such as e-commerce and non-contact solutions in 2019–2020 and are also now looking to overhaul their systems after a three-year period. We also note demand for major upgrades to core systems in fields such as accounting, HR, call centers, and CRM.

BEDDING IN OF PRICE HIKE CULTURE AND GROWTH IN CORPORATE PROFITS

Japanese firms are clearly moving to pass higher costs on to prices. We see potential for a virtuous cycle by which rising wages drive growth in demand for high-priced products and services. The entrenchment of a culture of price hikes could help Japanese firms escape from the low margins that have been a weak point. Companies that have hiked prices and raised profit guidance have shown better share price performance since spring.

After the collapse of the bubble, the Japanese economy fell into a deflationary equilibrium. Companies hit by low growth attempted to generate profits by lowering prices and selling large quantities at low margins. Economies of scale from this approach enabled them to lower prices further.

However, this deflationary equilibrium is now starting to make less sense. A new inflationary equilibrium is starting to emerge because of labor shortages.

As labor shortages have become more severe, companies have found themselves unable to hire enough staff to maintain or increase market share by lowering prices. Ultimately, they have been forced to hike prices in order to meet the cost of having to pay higher wages in order to attract staff.

Figure 4: Japanese economy in negative spiral during period of deflationFigure 5: Potential “new normal” under major labor shortage

ACCELERATING SHAREHOLDER RETURNS (COMMONALITIES WITH THE US IN THE 1980S)

In March 2023, the Tokyo Stock Exchange (TSE) issued a list of requests to listed companies, urging them to manage their operations with due consideration to their cost of capital and their share prices, while asking them to conduct analyses of return on capital and then draw up plans to improve their corporate value. With expectations for corporate governance improvement heightening, we think the concepts of shareholder value and corporate value have been increasingly taking hold in the Japanese equity market against a backdrop of changing shareholder structures and increasing shareholder activism.

Due to pressure from the market, we think the lay of the land in Japan’s equity markets has come to resemble that of the US stock market in the 1980s, when shareholder returns expanded rapidly. This suggests that there is potential for Japanese companies to ramp up investor returns.

Total dividends paid by all listed companies in Japan for FY22 amounted to ¥18.2trn, and share buybacks executed totaled ¥9.7bn, record highs in both cases. The total shareholder return payout ratio came to 55.4%, significantly higher than the ratios observed in previous peaks in FY07 (46.5%), and FY18 (47.3%).

Looking at total shareholder return payout ratios for the 23 developed market countries included in the MSCI World Index, the average for the past five years stood at 73.5%. Calculated on the same basis, the ratio for Japan is fully 17 percentage points lower, at 56.5%.

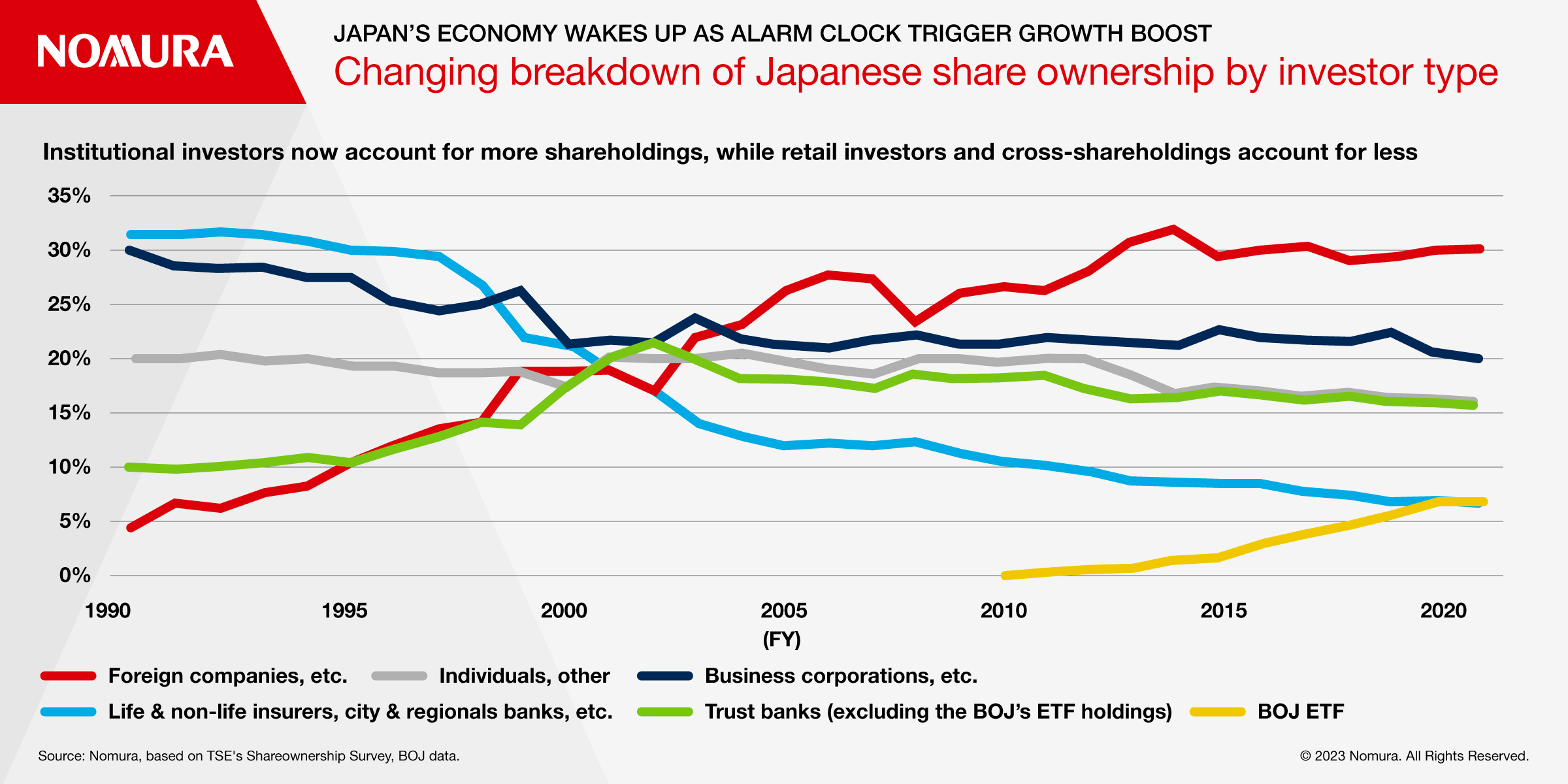

PROGRESS IN THE DISSOLUTION OF CROSS-SHAREHOLDINGS

Much progress has been made in dissolving corporate cross-shareholdings. The fraction of shares held by entities such as life insurers, non-life insurers, city banks, and regional banks stood at 10.5% in FY10, but by FY21 had fallen to 6.4%. Meanwhile, cross-shareholdings among non-financial corporations fell noticeably in both FY20 and FY21, bringing cross shareholdings as a fraction of share ownership in the stock market down to its lowest level ever.

The makeup of share ownership in the market has changed in ways that put more pressure on corporate management teams to be accountable to shareholders, in a similar vein to changes that the US stock market went through in the 1980s, when retail investors ended up holding a smaller proportion of shares while institutional investors held a larger proportion.

Figure 6: How the breakdown of share ownership by investor type in Japan’s stock market has changed over time

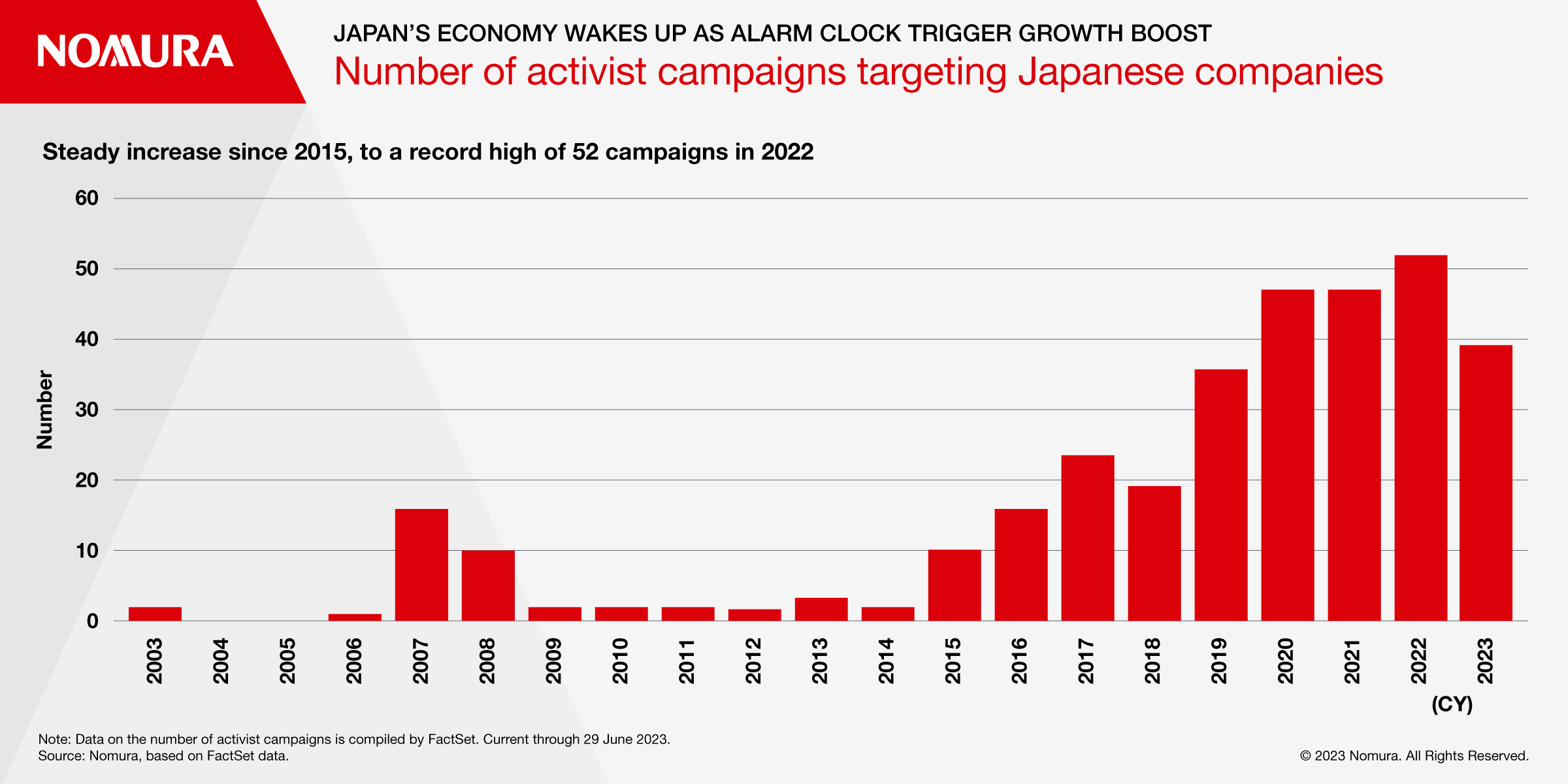

THE RISE OF THE ACTIVISTS

Activism is on the rise in Japan now, showing further similarities to the takeover environment that the US market saw in the 1980s. FactSet data shows that activist campaigns have increased steadily since 2015, rising to a record high of 52 campaigns in 2022. NHK, Japan’s public television network, ran a special feature in April, in which it tackled why activist investors have been targeting Japanese firms. It noted that while activists have historically been seen as seeking only to maximize short-term profits, today’s activists are more willing to point out problem areas in corporate governance, and have also lauded Japanese companies for continually evolving while capably navigating the changes seen in Japan’s regulatory regime and its society.

Figure 7: Number of activist campaigns targeting Japanese companies

WHAT WOULD HAPPEN IF JAPAN FINALLY BROKE OUT OF DEFLATION?

Price hikes in Japan are beginning to look as though they are here to stay, and this is a truly significant development for Japanese equities. Investors have for a long time held Japanese stocks in fairly low esteem, largely because of their low return on equity (ROE), and more specifically their low profit margins. If companies can rid themselves of the assumption that their domestic prices will remain unchanged, this will add a new axis to long-term profit maximization strategies, namely price revisions.

If Japanese companies succeed in dynamically revising prices like European companies have done, while adjusting employment practices, we see the potential for a 40% improvement in margins and ROE, which could push the Nikkei 225 up to 45,000. The rapid rise in share prices since spring may be evidence that the market is beginning to price in this scenario.

This content has been prepared by Nomura solely for information purposes, and is not an offer to buy or sell or provide (as the case may be) or a solicitation of an offer to buy or sell or enter into any agreement with respect to any security, product, service (including but not limited to investment advisory services) or investment. The opinions expressed in the content do not constitute investment advice and independent advice should be sought where appropriate.The content contains general information only and does not take into account the individual objectives, financial situation or needs of a person. All information, opinions and estimates expressed in the content are current as of the date of publication, are subject to change without notice, and may become outdated over time. To the extent that any materials or investment services on or referred to in the content are construed to be regulated activities under the local laws of any jurisdiction and are made available to persons resident in such jurisdiction, they shall only be made available through appropriately licenced Nomura entities in that jurisdiction or otherwise through Nomura entities that are exempt from applicable licensing and regulatory requirements in that jurisdiction. For more information please go to https://www.nomuraholdings.com/policy/terms.html.